With the Fed signaling a possible pause in rate hikes, inflation still elevated but easing, and growth data softening, income focused investors are again weighing the appeal of dividend paying blue chips. The current mix of moderating inflation, uncertain policy direction, and sensitive bond yields can change how reliably certain stocks support a portfolio’s cash flow and risk profile. This article looks at three dividend paying blue chip stocks from our screener that appear well aligned with today’s cross currents, and explains why some investors are watching them closely as potential sources of stability and income.

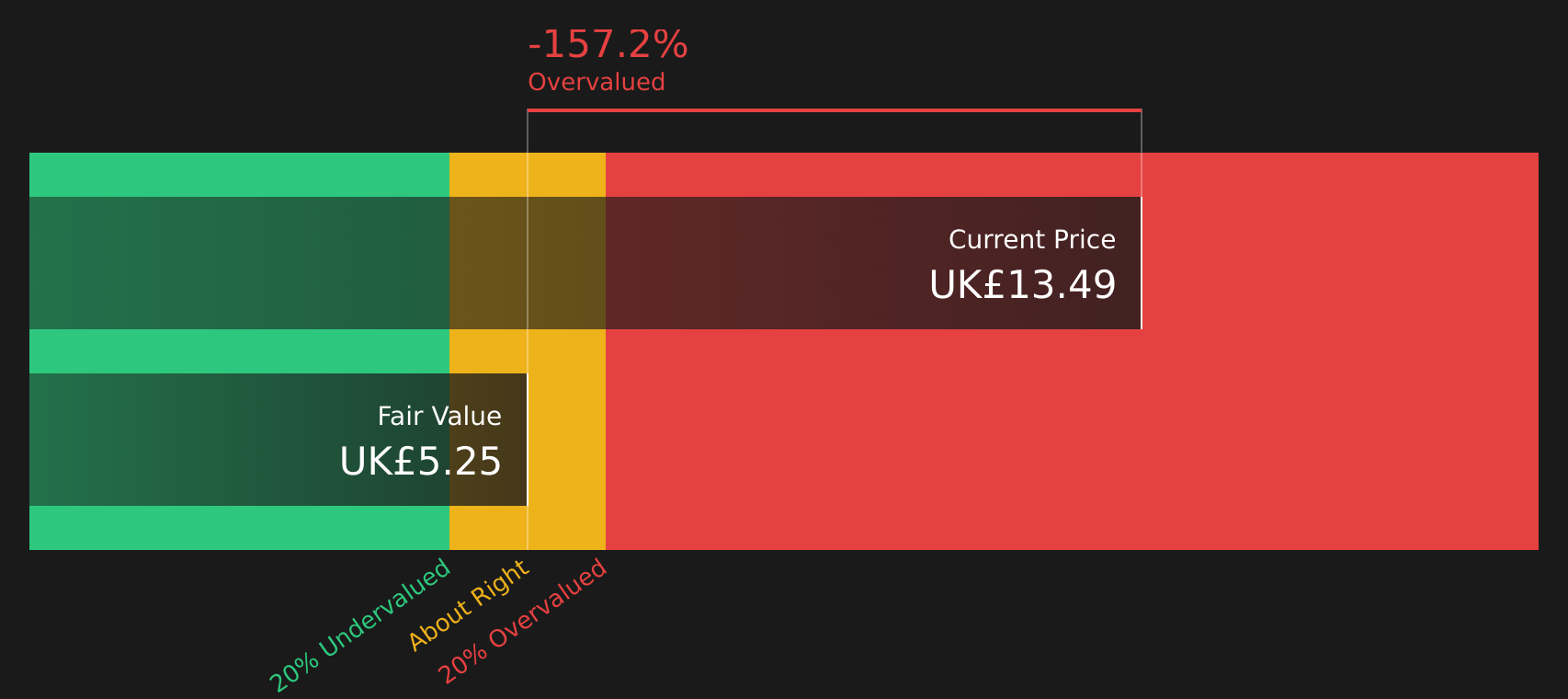

United Utilities Group (LSE:UU.)

Overview: United Utilities Group is a UK based utility that supplies water and wastewater services, while also operating in energy generation, financing, and property management, from its base in Warrington. The company runs an extensive network of around 122,000 kilometers of pipes to serve households and businesses.

Operations: United Utilities Group generates £2.6b in revenue primarily from its regulated UK water and wastewater business, all from within the United Kingdom.

Market Cap: £10.0b

Income focused investors watching United Utilities Group are weighing a mix of utility cash flows, a 3.98% dividend yield and meaningful investment plans against a balance sheet that relies heavily on debt and fresh equity. The company is channeling new capital, including an £800m share sale, into leak detection technology, pollution control and network upgrades that are intended to support long term service quality and dividend capacity, especially as the Fed’s softer tone on rates supports demand for steady income stocks. At the same time, negative credit outlooks, rising operating costs and a dividend that is not fully covered by free cash flow underline why careful analysis of risks, regulatory decisions and execution on the AMP8 investment programme matters for anyone considering this stock.

United Utilities Group’s heavy investment phase and 3.98% yield can look appealing, but the real story sits in how those plans line up with its cash generation and balance sheet, which the United Utilities Group financial health report examines in more detail.

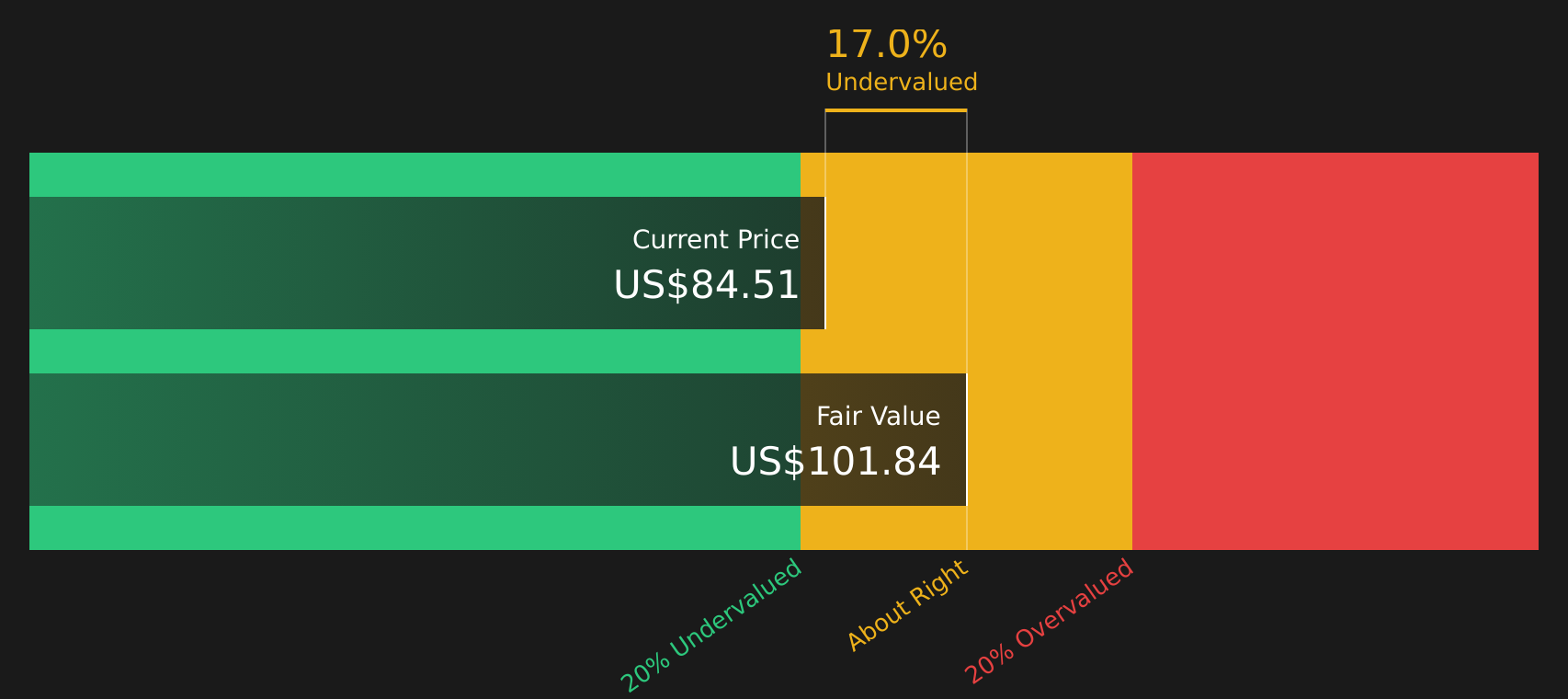

MGE Energy (MGEE)

Overview: MGE Energy is a Madison based public utility holding company that generates and distributes electricity and natural gas in the United States, serving around 170,000 electric customers through a mix of coal, gas and growing renewable sources, plus battery storage. It also invests in and operates transmission facilities that move power across its regional grid.

Operations: MGE Energy generates around US$537 million of revenue from electric operations, US$253 million from gas, and about US$46 million from non regulated energy activities, with a US$68 million consolidation adjustment across the group.

Market Cap: US$3.4b

MGE Energy may appeal to income seekers who want a regulated utility with a history of dividend growth and earnings that analysts describe as high quality, at a time when a possible Fed pause and softer growth are drawing investors toward steady cash payers. Analysts currently project earnings and revenue growth in the mid single digits, alongside capital investment in renewables and recent analyst upgrades. These factors point to a company that some investors view as more of a defensive compounder than a high flier. However, the P/E premium to its own cash flow value, high debt, and dividends that are not well covered by free cash flow indicate that the current price may leave limited room for disappointment if funding costs or demand conditions change.

MGE Energy’s steady regulated earnings and premium P/E suggest that investors might be overlooking a key tension between stability and price. The 2 key rewards and 2 important warning signs could clarify whether that premium is quietly justified or masking something else.

American States Water (AWR)

Overview: American States Water is a San Dimas based utility that supplies water and electricity to around 265,100 water customers and 24,900 electric customers in California, and also runs a contracted services arm that provides water and wastewater services on US military bases.

Operations: American States Water generates about US$475.2m from Water, US$60.9m from Electric and US$143.2m from Contracted Services, with all of its US$679.3m revenue coming from the United States.

Market Cap: US$3.3b

American States Water is often viewed as a potential fit for investors looking for a defensive, dividend paying blue chip that still has growth angles. It combines a long history of dividend increases, expectations for mid to high single digit earnings growth, and rising revenue across its regulated and contracted businesses. At the same time, its California concentration, higher debt, use of equity issuance and exposure to regulatory decisions on cost of capital and decoupling mean that today’s premium valuation may leave less room for missteps. The interest rate backdrop and the bond sensitive nature of utility stocks make it especially important to understand how American States Water’s planned infrastructure spending, military contracts and regulatory environment interact with its earnings quality and dividend resilience.

American States Water’s premium valuation and California concentration have some investors split, yet its mix of regulated earnings and military contracts could be more resilient than it looks. See how the 3 key rewards and 2 important warning signs might reframe that balance between comfort and hidden pressure points

The three dividend paying blue chips in this article are just a starting point, with the full Dividend Paying Blue Chip Stocks screener surfacing 37 more companies that pair established balance sheets with dividend histories and narratives that may be just as compelling as the ones already covered through the Dividend-Paying Blue Chip Stocks screener. Use Simply Wall St to identify, filter and analyze the specific catalysts, risk profiles and income narratives that matter most to you so you can focus on the dividend ideas that best match your conviction and time horizon.

Take Control of Your Investment Journey

If MGE Energy or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh breakout stories and under the radar compounders do not stay quiet for long. Once momentum is moving, ideal entry windows can narrow quickly, so it may be worth reviewing potential opportunities promptly.

- Spot companies quietly building momentum across niche commodities and infrastructure by scanning the curated 30 best rare earth metal stocks before they move onto everyone else’s radar.

- Track income-focused companies with balance sheet strength by running the focused 3 dividend fortresses while yields may still appear compelling to some income investors.

- Explore potential market leaders in automation by filtering the hand picked 30 robotics and automation stocks and see which businesses are building long term earnings engines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com