Deutsche Bank’s June 30 research placed AMETEK (AME) on the radar for short term investors, citing expected 2027 earnings strength tied to a recovering short cycle market and contributions from its Indicor segment.

See our latest analysis for AMETEK.

AMETEK’s share price has had a firm run over the past year, with a 12.18% year to date share price return and a 28.18% 1 year total shareholder return. More recent 1 day and 7 day share price moves have softened, hinting that near term enthusiasm has cooled even as the longer term performance trend remains supportive of the earnings story highlighted in Deutsche Bank’s research.

If AMETEK’s setup has you thinking about where else strong earnings narratives may emerge next, it could be worth scanning 35 power grid technology and infrastructure stocks as another way to spot companies tied to essential infrastructure themes.

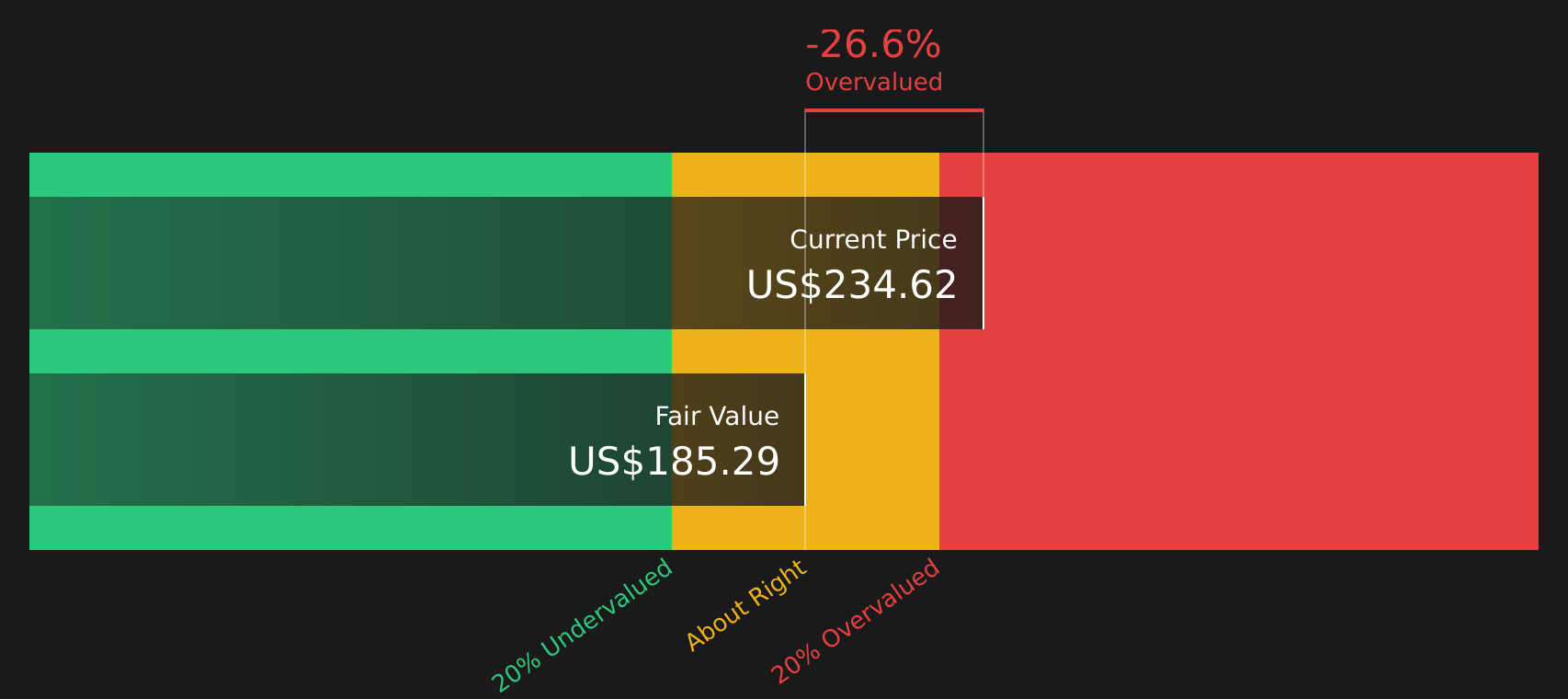

With AMETEK trading at $234.62, sitting at a discount to the average analyst price target but also carrying a weak value score, the key question is whether the stock is mispriced or if the market already reflects those 2027 earnings expectations.

Most Popular Narrative: 9.4% Undervalued

AMETEK’s most followed narrative points to a fair value of $259.05, which sits above the last close at $234.62 and puts the recent share price strength in context.

Adoption of digital reality, automation, and advanced metrology solutions is accelerating across key end markets such as aerospace, defense, and architecture. This trend was recently reinforced by the FARO Technologies acquisition, which expands AMETEK's addressable market and supports both revenue and margin growth through higher value, software-enabled recurring revenue streams. Growing global focus on sustainability and energy efficiency, alongside regulatory requirements across sectors (e.g., energy, grid modernization, environmental labs), is driving long-term demand for high-precision analytical and monitoring instrumentation. These dynamics favor AMETEK's portfolio and support steady revenue and market share gains.

Want to see what is baked into that fair value gap? The narrative leans heavily on compounded revenue growth, rising margins and a richer earnings multiple. Curious which assumptions really move the $259.05 figure and how long earnings would need to track those projections?

Result: Fair Value of $259.05 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the AMETEK narrative could be tested if weakness in semiconductor and research markets persists, or if acquisition driven growth underdelivers against expectations.

Find out about the key risks to this AMETEK narrative.

Another View: AMETEK Through A Cash Flow Lens

The narrative-driven fair value for AMETEK at $259.05 points to a 9.4% gap versus the $234.62 share price, yet the Simply Wall St DCF model paints a tighter picture. On that cash flow basis, AMETEK’s fair value is $180.43, which implies the stock screens as overvalued rather than undervalued.

The contrast is clear. Analysts leaning on earnings and multiples see potential upside from here. In comparison, the DCF view suggests investors are already paying up for a long runway of cash flows. Which set of assumptions feels closer to how you think AMETEK’s future will actually unfold?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AMETEK for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around AMETEK have you on the fence, it can be worthwhile to act early and review the numbers yourself by examining the 3 key rewards.

Looking for more investment ideas beyond AMETEK?

If AMETEK has sharpened your focus on quality opportunities, do not stop here. Broaden your watchlist now so you do not miss the next idea.

- Target potential value opportunities by checking out 43 high quality undervalued stocks that combine solid fundamentals with prices the market may be overlooking.

- Secure your income focus by reviewing 7 dividend fortresses that offer higher yields with an emphasis on consistency.

- Prioritize resilience by scanning 75 resilient stocks with low risk scores designed to spotlight companies with steadier risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com