- In late June 2026, Sonos, Inc. was added to the Russell 2000 Value-Defensive, Defensive, and Growth-Defensive indices, while TC Acoustic and Lazada launched a Super Brand Day campaign in Singapore and Škoda Auto announced Sonos as the audio partner for its new Peaq electric vehicle.

- Together, these index inclusions and high-profile collaborations highlight Sonos’s expanding brand reach across both capital markets and consumer touchpoints, from home audio to in-car listening.

- We’ll now examine how Sonos’s additions to multiple Russell 2000 defensive indices could influence its investment narrative and perceived resilience.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Sonos Investment Narrative Recap

To own Sonos, you need to believe its premium audio ecosystem and expanding use cases can offset cyclical home-audio weakness, tariff headwinds, and a lull in major hardware launches. The Russell 2000 defensive index additions may modestly support Sonos’s “resilience” narrative in the near term, but they do not directly address the core risks around tariffs, competition, or dependence on a relatively narrow hardware portfolio.

The Škoda Peaq partnership is the most relevant development here, as it pushes Sonos beyond the living room and into automotive audio, a newer category for the company. If Sonos can turn more of these collaborations into recurring product lines, that could help diversify revenue away from cyclical home audio and partially offset tariff and pricing pressures, though it is still early for this opportunity.

Yet, against this broader opportunity, investors should still be aware of how rising tariffs on Vietnam and Malaysia production could...

Read the full narrative on Sonos (it's free!)

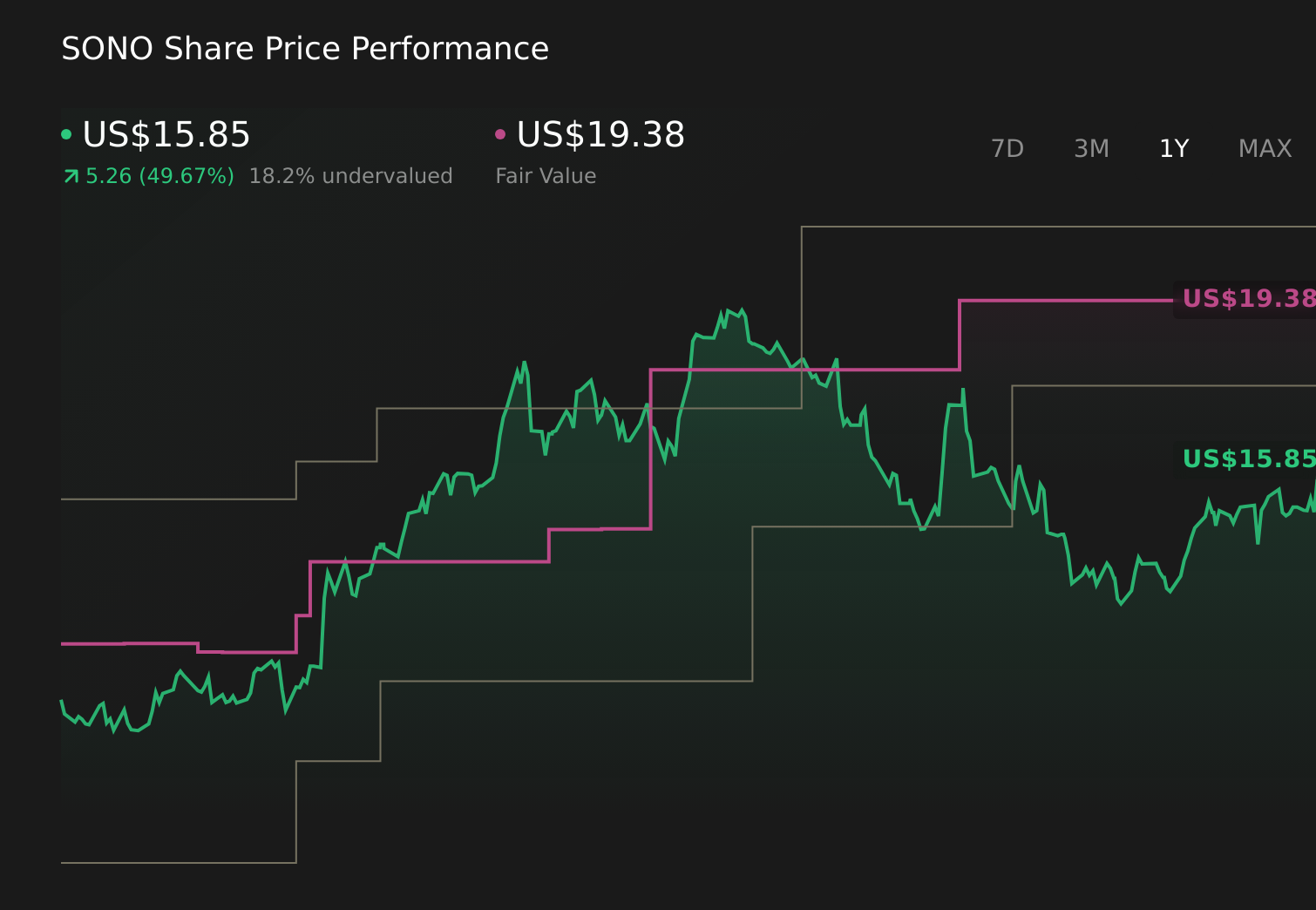

Sonos’ narrative projects $1.6 billion revenue and $120.2 million earnings by 2028. This implies an increase in earnings from today’s level to reach that $120.2 million forecast.

Uncover how Sonos' forecasts yield a $19.38 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were already assuming revenue could reach about US$1.8 billion and earnings about US$166 million, suggesting a much stronger outcome than consensus. In contrast to concerns about tariffs and commoditized hardware, these bullish views lean on faster platform and AI driven adoption, and the latest announcements could either support or challenge those expectations over time.

Explore 5 other fair value estimates on Sonos - why the stock might be worth as much as 54% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sonos research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Sonos research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sonos' overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com