- In late June 2026, The Goldman Sachs Group, Inc. launched a wide range of callable fixed-rate medium-term notes across maturities from 2028 to 2046, while also being reclassified out of several Russell growth benchmarks and into the Russell 1000 Value-Defensive and Russell 1000 Defensive indices.

- This shift from growth to value and defensive indices, alongside active issuance in its own bond curve, highlights how Goldman’s profile is being reframed for both equity and fixed-income investors.

- We’ll now examine how Goldman’s move into value and defensive indices could inform its existing investment narrative around earnings quality and capital deployment.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

Goldman Sachs Group Investment Narrative Recap

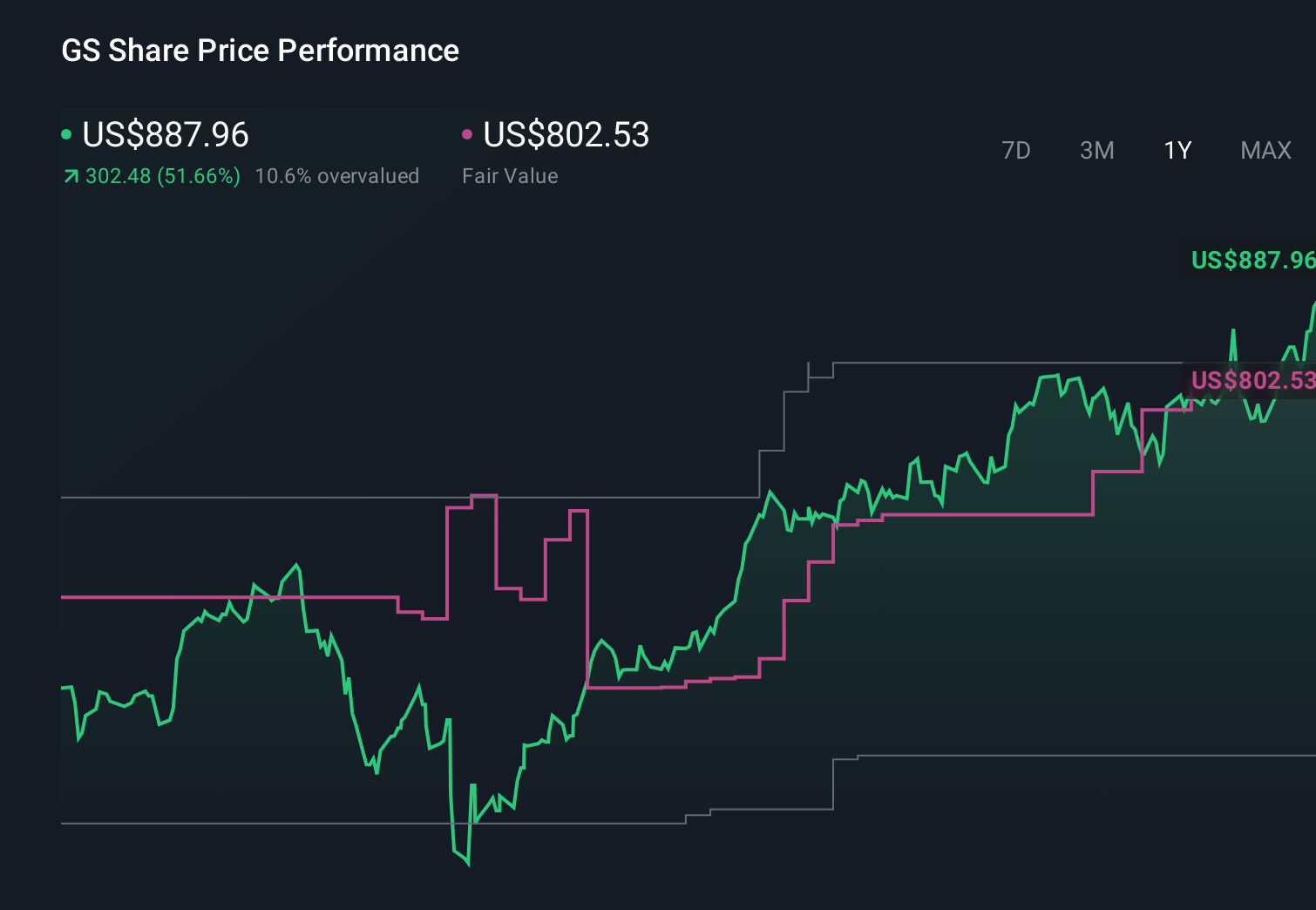

To own Goldman Sachs today, you need to believe in its ability to turn a diversified, global franchise into steady fee and financing income while managing regulatory and geopolitical shocks. The shift into Russell value and defensive indices, alongside active issuance of callable medium term notes, reinforces a perception of Goldman as a more mature, capital intensive compounder. This reclassification does not materially change the near term balance between the key catalyst of deal and fee momentum and the ongoing risk from evolving capital rules.

The late June 2026 wave of callable fixed rate medium term note offerings, stretching out to 2046, is the clearest tie to this evolving story. It sits alongside recent buybacks and dividends as part of a broader capital stack picture, but for equity holders the more relevant connection is how sustained access to term funding underpins Goldman's ability to keep leaning into asset and wealth management growth, while still absorbing any higher capital buffers that regulators may require.

Yet despite this more defensive label, one risk investors should still be aware of is how future regulatory shifts could interact with Goldman's growing use of long dated funding and potentially...

Read the full narrative on Goldman Sachs Group (it's free!)

Goldman Sachs Group's narrative projects $67.7 billion revenue and $20.0 billion earnings by 2029. This requires 3.2% yearly revenue growth and a $2.9 billion earnings increase from $17.1 billion today.

Uncover how Goldman Sachs Group's forecasts yield a $934.19 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts sound far more cautious than consensus, arguing that rising digitization and fintech disruptors could steadily erode margins across Goldman's core franchises just as it is reclassified as a value defensive name. These analysts were only counting on revenue to grow around 1.6% annually to about US$64.5 billion by 2029 and earnings to reach roughly US$18.6 billion, so the latest funding and index changes might prompt them to revisit whether their already conservative assumptions still hold or need to be revised in either direction.

Explore 5 other fair value estimates on Goldman Sachs Group - why the stock might be worth 9% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Goldman Sachs Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Goldman Sachs Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Goldman Sachs Group's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com