- In late June 2026, Ormat Technologies, Inc. (NYSE: ORA) was added to several Russell growth and small‑cap indices, including the Russell 2000 Growth, 2500 Growth, 3000 Growth, 3000E Growth, Small Cap Comp Growth, and the Russell 2000 Growth‑Defensive Index.

- This broad index inclusion increases Ormat’s visibility across growth‑oriented benchmarks, potentially making the geothermal and energy storage company more prominent in institutional portfolios.

- We’ll now examine how Ormat’s broad addition to multiple Russell growth indices may influence its existing investment narrative and future expectations.

Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Ormat Technologies Investment Narrative Recap

To own Ormat, you need to believe in long duration demand for geothermal and energy storage projects supported by policy incentives and long term contracts. The broad Russell growth index additions improve visibility but do not materially change the near term focus on executing capex heavy expansion while managing rising leverage and operational risks in the electricity segment.

The upcoming Q2 2026 earnings release on August 5 is the most relevant near term checkpoint for this index news, as it will show how Ormat is converting its larger project pipeline and recent storage and geothermal asset additions into revenue and earnings, and whether margins and capex are tracking in line with its reaffirmed 2026 guidance.

Yet behind the index inclusion and growth story, investors should be aware of the concentration risk in battery sourcing and the evolving FEOC rules that could ...

Read the full narrative on Ormat Technologies (it's free!)

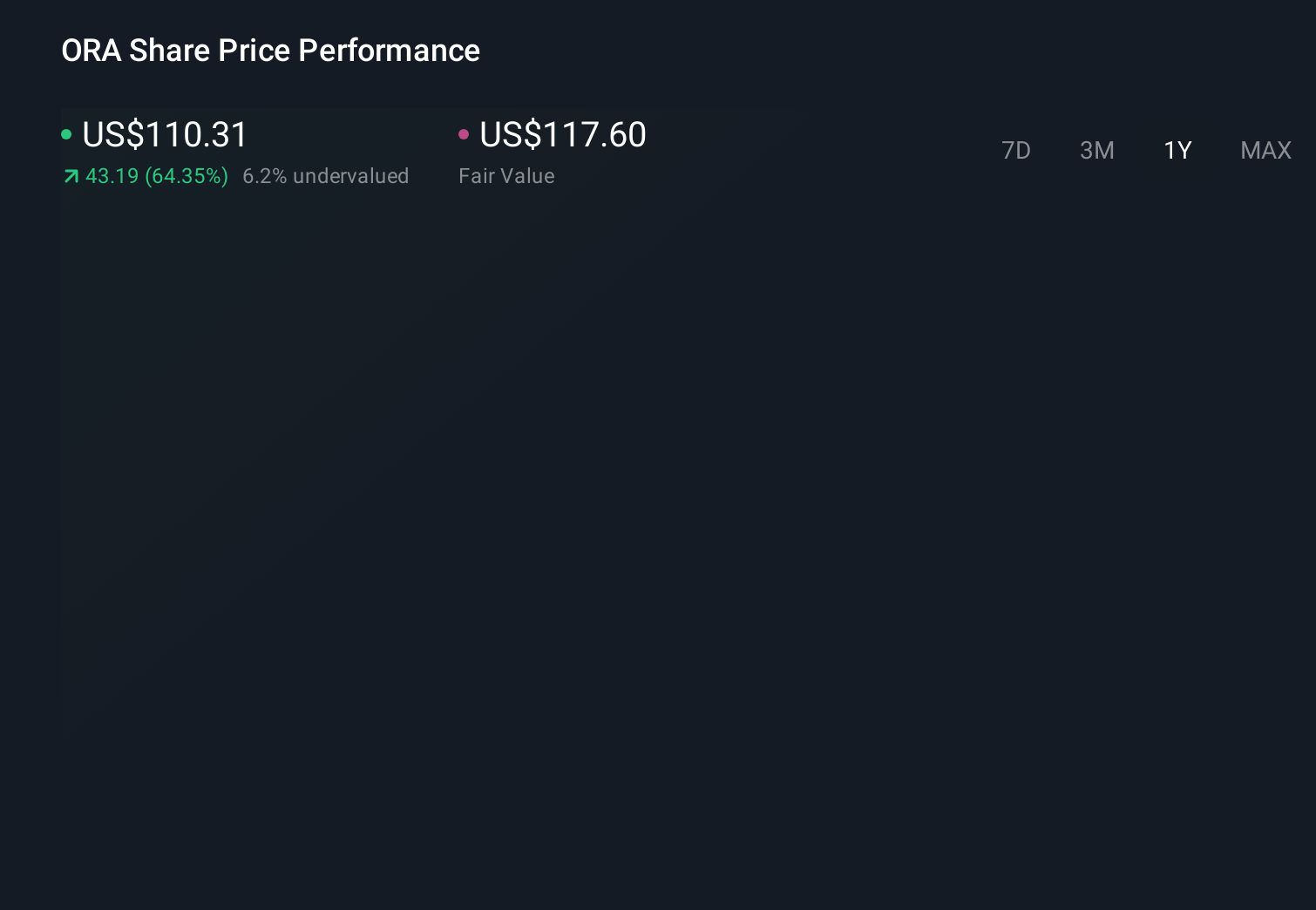

Ormat Technologies' narrative projects $1.3 billion revenue and $194.6 million earnings by 2029.

Uncover how Ormat Technologies' forecasts yield a $135.45 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Ormat span roughly US$118 to US$192 per share, showing how far apart individual views can be. When you set those against the heavy capex needs and leverage sensitivity outlined earlier, it underlines why checking multiple opinions before forming your own view on Ormat’s prospects can be so important.

Explore 3 other fair value estimates on Ormat Technologies - why the stock might be worth just $118.26!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ormat Technologies research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Find 41 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com