- In June 2026, Huntington Ingalls Industries (HII) was added to the Russell 1000 Value-Defensive and Russell 1000 Defensive Indexes, secured a US$417.7 million five-year Navy elevator maintenance contract, opened the new Carrier Refueling Overhaul Workcenter at Newport News, and began fabricating the future USS John F. Lehman (DDG 137).

- Together, these developments underscore HII’s expanding role across both new-build and long-term sustainment work for the U.S. Navy, while also aligning the stock more closely with institutional investors focused on defensive, value-oriented exposures.

- We’ll now examine how the new US$417.7 million Navy sustainment contract influences HII’s existing investment narrative and long-term outlook.

Find 41 companies with promising cash flow potential yet trading below their fair value.

Huntington Ingalls Industries Investment Narrative Recap

To own Huntington Ingalls Industries, you need to believe in a durable U.S. Navy shipbuilding and sustainment pipeline, supported by large, multi‑year programs and recurring lifecycle work. The new US$417.7 million elevator maintenance contract moderately reinforces the near term catalyst of steadier earnings from services, but it does not remove key risks such as reliance on future block submarine awards and potential pressure on U.S. defense budgets.

The elevator sustainment award is especially relevant because it expands HII’s Mission Technologies work across global maintenance, training, and rapid response services, complementing the shipyards’ capital intensive builds. As a multi‑year IDIQ contract, it sits squarely within the existing catalyst of growing recurring maintenance and modernization revenue, which can help offset volatility if major new‑build program awards slip or are scrutinized more heavily in future budget cycles.

Yet while contracts like this help, investors should also be aware of the risk that future U.S. defense budgets could eventually shift away from large manned vessels and...

Read the full narrative on Huntington Ingalls Industries (it's free!)

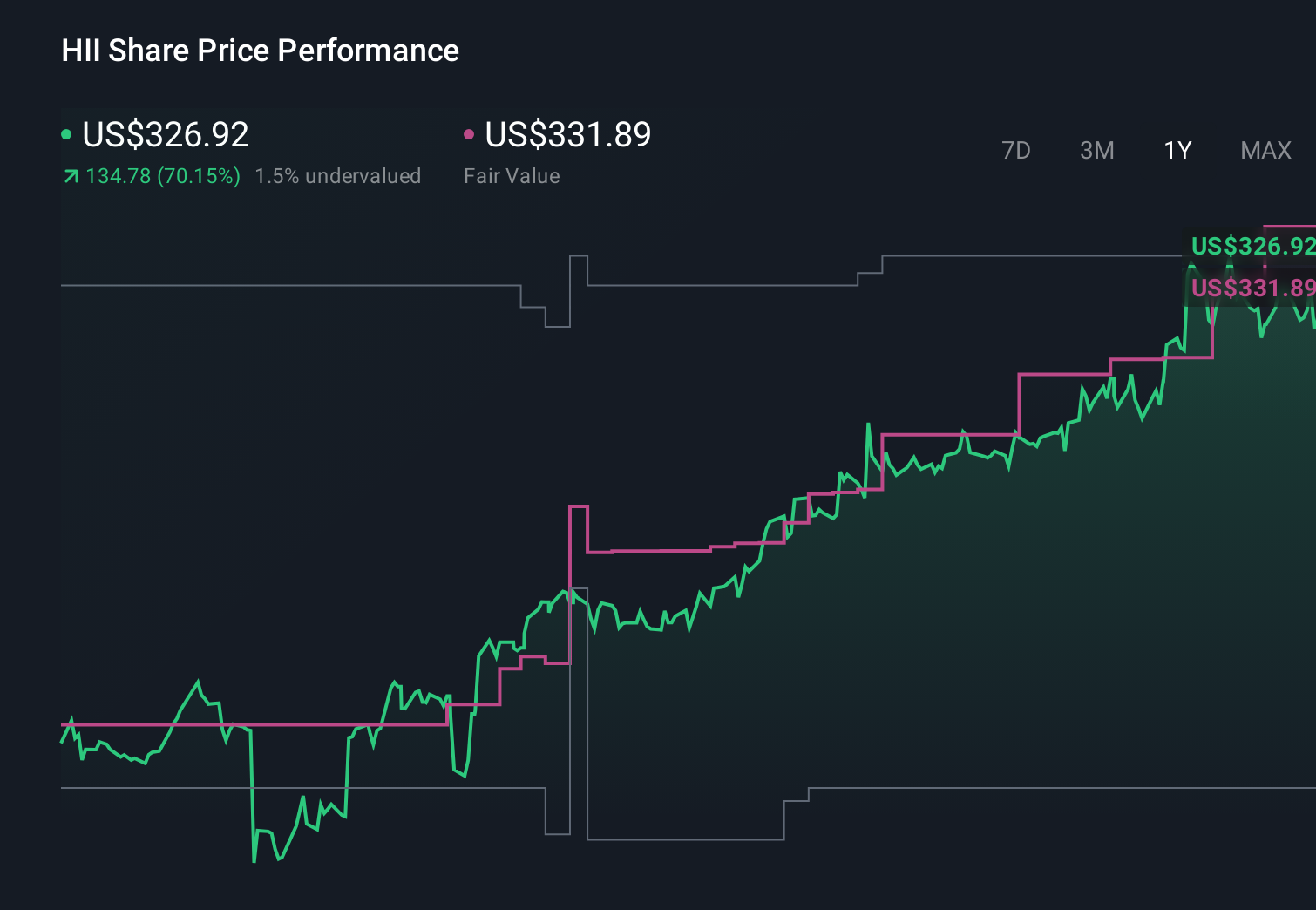

Huntington Ingalls Industries' narrative projects $14.8 billion revenue and $920.3 million earnings by 2029. This requires 4.9% yearly revenue growth and about a $315 million earnings increase from $605.0 million today.

Uncover how Huntington Ingalls Industries' forecasts yield a $387.91 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Some analysts see a much tougher road ahead, even before this contract win, with bearish forecasts of only about 4.3 percent annual revenue growth and earnings of roughly US$831 million by 2029, so it is worth comparing how their more cautious view of budget and autonomy risks might shift if HII keeps adding high margin sustainment work.

Explore 4 other fair value estimates on Huntington Ingalls Industries - why the stock might be worth as much as 58% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Ingalls Industries research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Huntington Ingalls Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Ingalls Industries' overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com