- In late June 2026, Quanta Services, Inc. (NYSE:PWR) was moved out of several Russell midcap and value benchmarks and added to larger-cap, growth and defensive Russell indexes, while its subsidiary entered a joint venture with Hyosung HICO to manufacture high-voltage circuit breakers in Pennsylvania.

- This combination of index reclassification and U.S.-based power equipment expansion highlights how Quanta is being repositioned in markets as a larger, growth-oriented infrastructure player.

- We’ll now examine how Quanta’s shift into top-tier Russell growth and defensive indexes may influence its broader investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Quanta Services Investment Narrative Recap

To own Quanta Services, you need to believe in a long, infrastructure-heavy power buildout and the company’s ability to execute profitably on complex grid projects. The biggest near term catalyst remains how effectively Quanta converts its record project pipeline into earnings, while key risks center on execution across acquisitions and large-scale transmission jobs. The latest Russell index moves and Hyosung HICO breaker JV do not materially change those near term drivers, but they slightly sharpen the focus on growth and power equipment exposure.

Among recent developments, the Hyosung HICO high voltage circuit breaker joint venture stands out as most relevant. It directly connects to Quanta’s core transmission and substation work, potentially helping with equipment availability and bid competitiveness on large U.S. grid projects. For investors focused on project timing risks and backlog quality, this manufacturing foothold in Pennsylvania sits squarely in the path of the same grid and data center power catalysts that are shaping expectations for Quanta’s earnings trajectory.

Yet against this growth story, investors should not overlook how tighter labor markets and complex, politically sensitive transmission projects could still...

Read the full narrative on Quanta Services (it's free!)

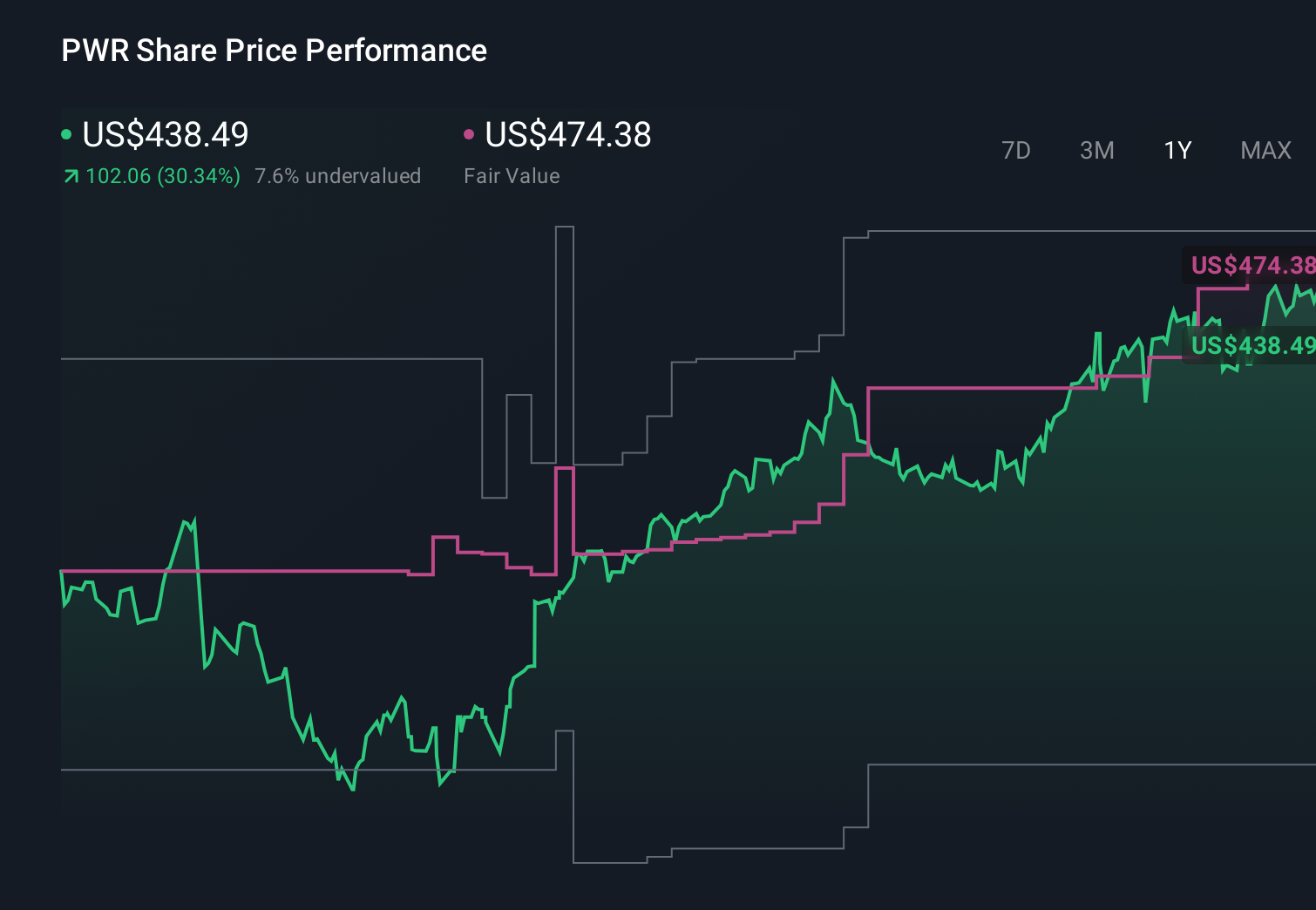

Quanta Services’ narrative projects $46.7 billion revenue and $2.4 billion earnings by 2029.

Uncover how Quanta Services' forecasts yield a $761.35 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling Quanta to reach about US$49.2 billion in revenue and US$3.3 billion in earnings by 2029, but this new index shift and equipment JV could either reinforce that grid supercycle view or highlight how exposed those bullish assumptions are to the risk that automation and new technologies eventually reshape the construction model you are betting on.

Explore 6 other fair value estimates on Quanta Services - why the stock might be worth as much as 7% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Quanta Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Quanta Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quanta Services' overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 42 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com