Index additions put Custom Truck One Source in focus

Custom Truck One Source (CTOS) has attracted fresh attention after being added to several Russell growth indices, including the Russell 2000 Growth, 2500 Growth, 3000 Growth, 3000E Growth, and Small Cap Comp Growth benchmarks.

See our latest analysis for Custom Truck One Source.

Custom Truck One Source has already seen strong share price momentum, with a 30 day share price return of 24.7%, a 90 day return of 81.9% and a year to date gain of 106.0%. The 1 year total shareholder return of 141.9% points to building positive sentiment that the index additions may be reinforcing.

If you are looking beyond Custom Truck One Source for other infrastructure linked ideas, it could be a good moment to scan opportunities in power grid technology and infrastructure through the 35 power grid technology and infrastructure stocks.

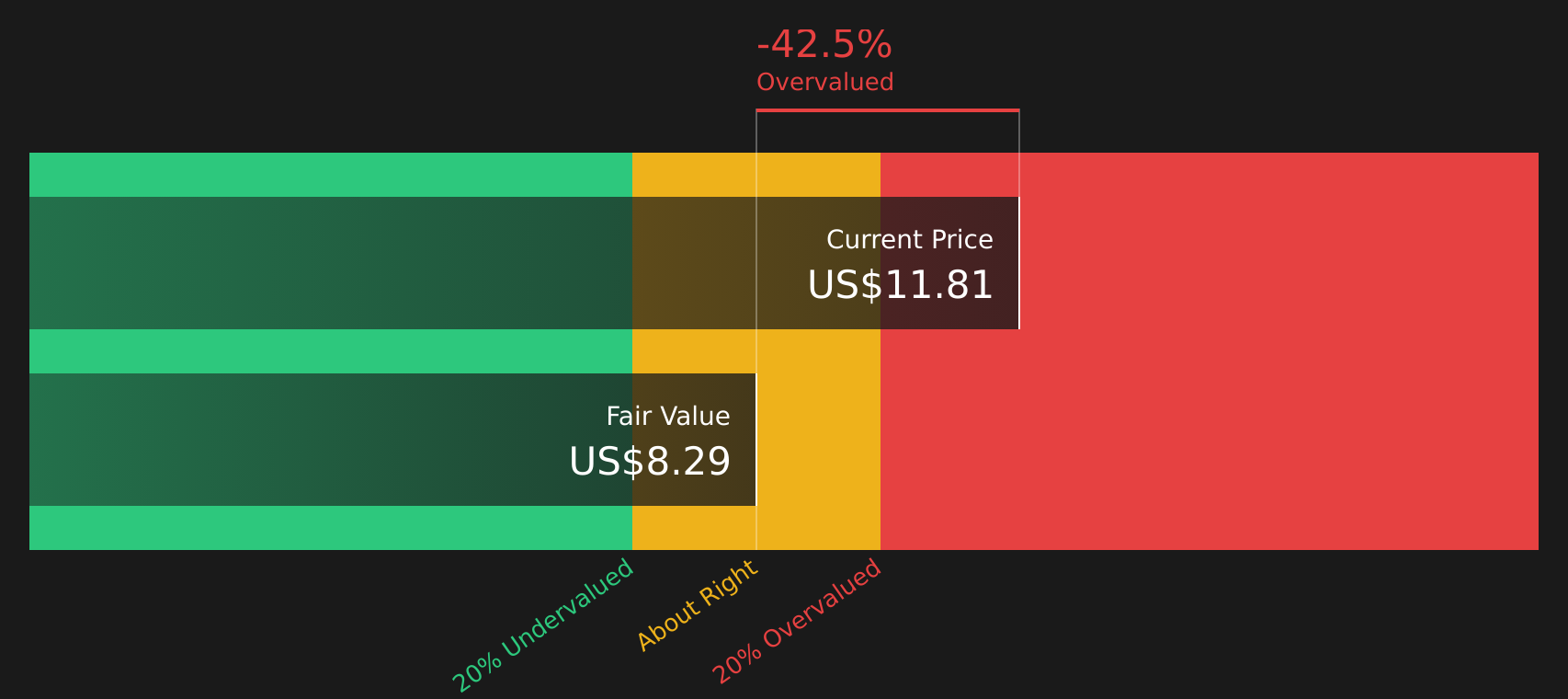

With Custom Truck One Source now trading around $11.95 after a strong run and sitting close to analyst targets, you have to ask: is there still mispricing here, or is the market already banking on future growth?

Most Popular Narrative: 56% Overvalued

At a last close of $11.95 against a narrative fair value of $7.67, Custom Truck One Source is framed as richly priced, which puts a lot of weight on its future execution.

Strategic and ongoing investments expanding the rental fleet and maintaining high utilization rates (above 75%) are increasing recurring revenue and providing margin stability, supporting consistent adjusted EBITDA growth and improved free cash flow generation.

Want to see the full playbook behind that fair value? The narrative leans on steady revenue expansion, margin repair, and a punchy future earnings multiple. Curious how those pieces fit together into a single number?

Result: Fair Value of $7.67 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still plenty that could go wrong for Custom Truck One Source if high net leverage collides with weaker TES backlogs or continued margin pressure.

Find out about the key risks to this Custom Truck One Source narrative.

Another View on Custom Truck One Source valuation

While the narrative fair value of $7.67 suggests Custom Truck One Source is overvalued at $11.95, the SWS DCF model points to a future cash flow value of $8.29, also below the current price. When two separate methods both sit under the market price, it raises a simple question: what is the crowd paying up for?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment on Custom Truck One Source split between rich pricing and clear rewards, this is a moment to review the facts and act on your own judgment. To see what investors are optimistic about in the data, take a closer look at the 2 key rewards.

Looking for more investment ideas beyond Custom Truck One Source?

If Custom Truck One Source has sharpened your focus on opportunities, do not stop here. Use the Simply Wall St screener to refresh your wider watchlist.

- Spot opportunities trading below their estimated worth by reviewing the 42 high quality undervalued stocks before the crowd fully catches on.

- Strengthen your portfolio’s foundations by zeroing in on companies in the solid balance sheet and fundamentals stocks screener (48 results) that prioritise financial resilience.

- Boost your income focus by scanning the 9 dividend fortresses so you are not leaving potential yield ideas on the table.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com