- On 27 June 2026, Polaris Inc. (NYSE: PII) was removed from several Russell value benchmarks and simultaneously added to multiple Russell growth indexes, marking a broad reclassification within the Russell 2000, 2500, 3000, and 3000E families.

- This rotation from value to growth index baskets may reshape how institutional investors view Polaris, influencing which portfolios hold the shares and how the company is compared with powersports and leisure peers.

- Next, we’ll examine how Polaris’s shift into Russell growth benchmarks interacts with its existing investment narrative around quality gains and tariff uncertainty.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Polaris Investment Narrative Recap

To own Polaris today, you need to believe its premium powersports brands and product innovation can ultimately outweigh tariff pressures, recent losses, and a soft retail backdrop. The shift from Russell value to growth benchmarks may change who holds the stock, but it does not materially alter the near term story, which still hinges on tariff mitigation progress as the main catalyst and sustained margin pressure from higher costs and weak volumes as the key risk.

The June 19 appointment of Dustin J. Semach, currently President and CEO of Sealed Air, to Polaris’s board and its Audit and Compensation Committees is timely against this backdrop. For investors focused on quality improvement and execution around tariffs and costs, adding a director with broad experience in finance, transformation, and global operations ties directly into the central question of whether Polaris can translate its growth reclassification into more durable earnings power.

Yet beneath the index shift, investors should pay close attention to how ongoing tariff exposure could still pressure margins and cash generation, especially if...

Read the full narrative on Polaris (it's free!)

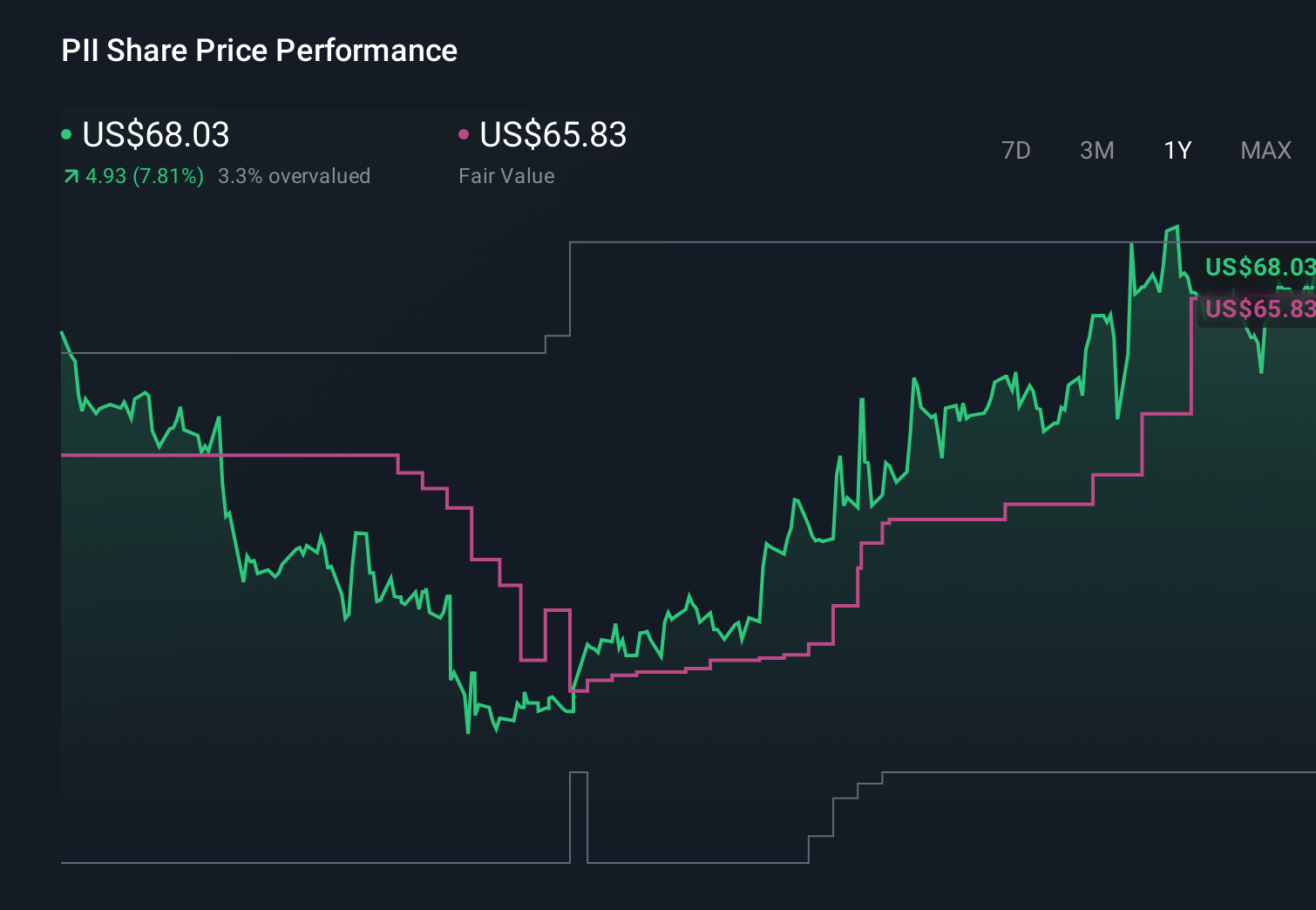

Polaris' narrative projects $7.8 billion revenue and $425.0 million earnings by 2029. This requires 2.1% yearly revenue growth and an $871.1 million earnings increase from -$446.1 million today.

Uncover how Polaris' forecasts yield a $68.00 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts, who were assuming earnings could reach about US$411 million by 2029, also highlight that continued investment in electrification could pressure margins, so you should weigh these upbeat forecasts against the real possibility that the index move and future regulatory or cost shifts may reshape both the upside and the risks.

Explore 3 other fair value estimates on Polaris - why the stock might be worth as much as 18% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 42 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com