- In June 2026, Sunrun Inc., Renew Home and Tesla Energy Operations, Inc. announced an alliance to aggregate millions of home batteries and smart devices into more than 16 gigawatts of flexible energy capacity for utilities and data center operators across key U.S. markets.

- This framework aims to turn existing residential equipment into what could be the country’s largest distributed power plant, freeing grid capacity while offering households lower bills, rewards, and improved resilience without requiring new hardware or land.

- We’ll now examine how this large-scale residential capacity aggregation affects Sunrun’s investment narrative, particularly its storage and grid services ambitions.

This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

Sunrun Investment Narrative Recap

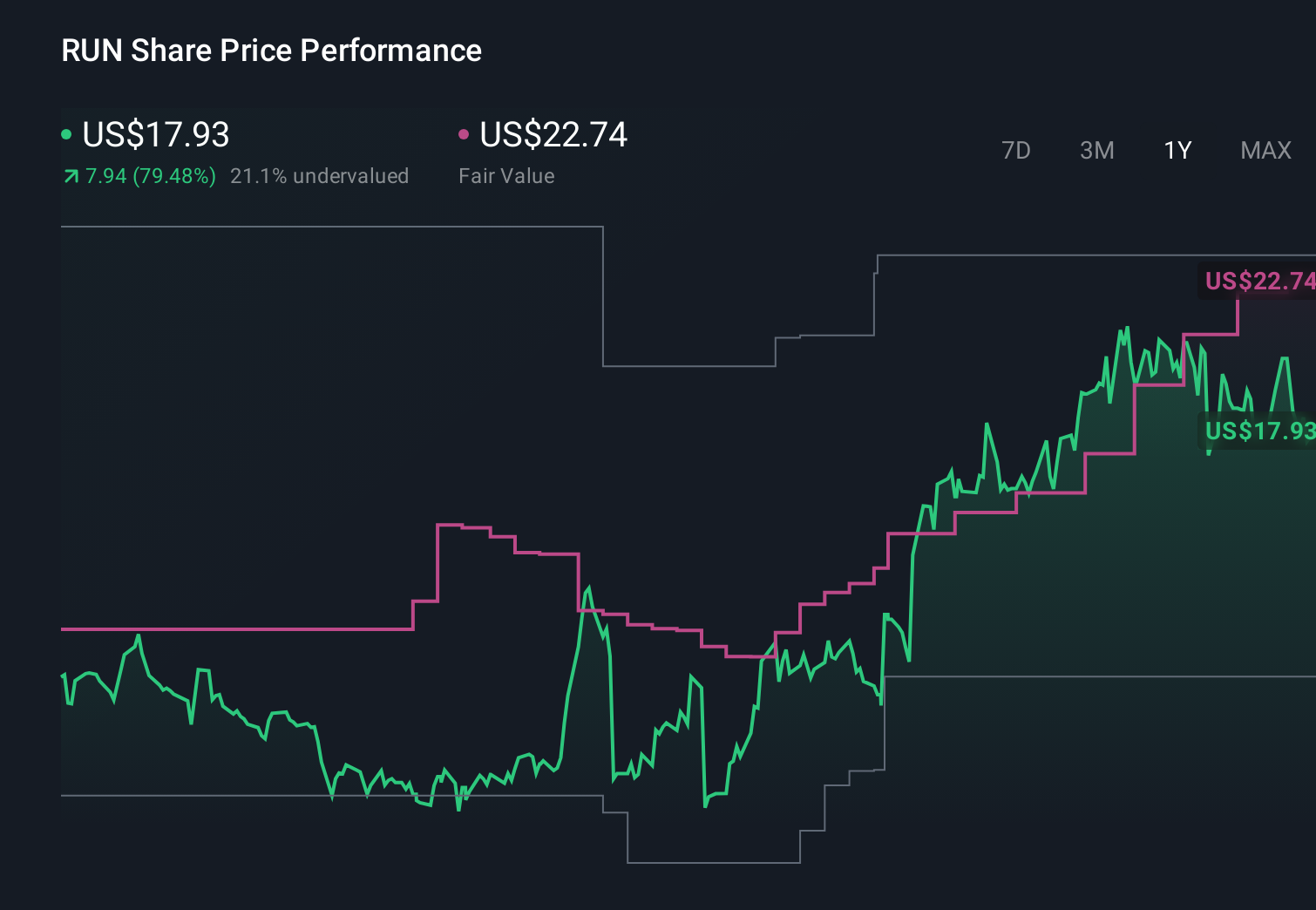

To own Sunrun, you need to believe that residential solar plus storage and grid services can become a durable, cash generative business, even as tax credits expire and financing stays capital intensive. The 16 gigawatt aggregation framework with Tesla and Renew Home directly reinforces Sunrun’s most important near term catalyst: scaling storage and grid services revenue. It also slightly reframes the biggest risk, as policy and incentive changes now affect not just rooftop demand but also how these large, aggregated resources are valued and compensated.

The new alliance builds on Sunrun’s earlier grid services work, particularly its 2025 Texas collaborations with Tesla Electric and NRG’s Reliant brand in ERCOT. Those programs gave Sunrun practical experience in aggregating home batteries and compensating customers for sharing stored energy, with Sunrun earning fees for dispatchable capacity. The 16 gigawatt framework looks like an order of magnitude expansion of that same concept, which could make grid services performance more central to how investors think about Sunrun’s future cash generation.

Yet while this growth story is appealing, investors should be aware that Sunrun’s dependence on tax incentives and external financing still leaves it exposed to...

Read the full narrative on Sunrun (it's free!)

Sunrun's narrative projects $3.7 billion revenue and $56.5 million earnings by 2029. This requires 8.0% yearly revenue growth and a $391.1 million earnings decrease from $447.6 million today.

Uncover how Sunrun's forecasts yield a $19.67 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Sunrun to reach about US$4.9 billion in revenue and US$1.1 billion in earnings by 2029, yet this new 16 gigawatt agreement could either reinforce those expectations or highlight how much they relied on aggressive grid service monetization without fully accounting for the policy and financing risks you have just seen.

Explore 3 other fair value estimates on Sunrun - why the stock might be worth just $19.09!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sunrun research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com