- Huntington Ingalls Industries’ Mission Technologies division was awarded a US$418 million, five-year IDIQ contract to repair and maintain shipboard-based elevators, cargo handling equipment and related systems on U.S. Navy aircraft carriers and amphibious ships worldwide, with work and sailor training already underway following the June 2026 award.

- This elevator sustainment contract deepens Mission Technologies’ role in fleet readiness and adds a sizeable, multi-year services stream that complements HII’s large shipbuilding programs.

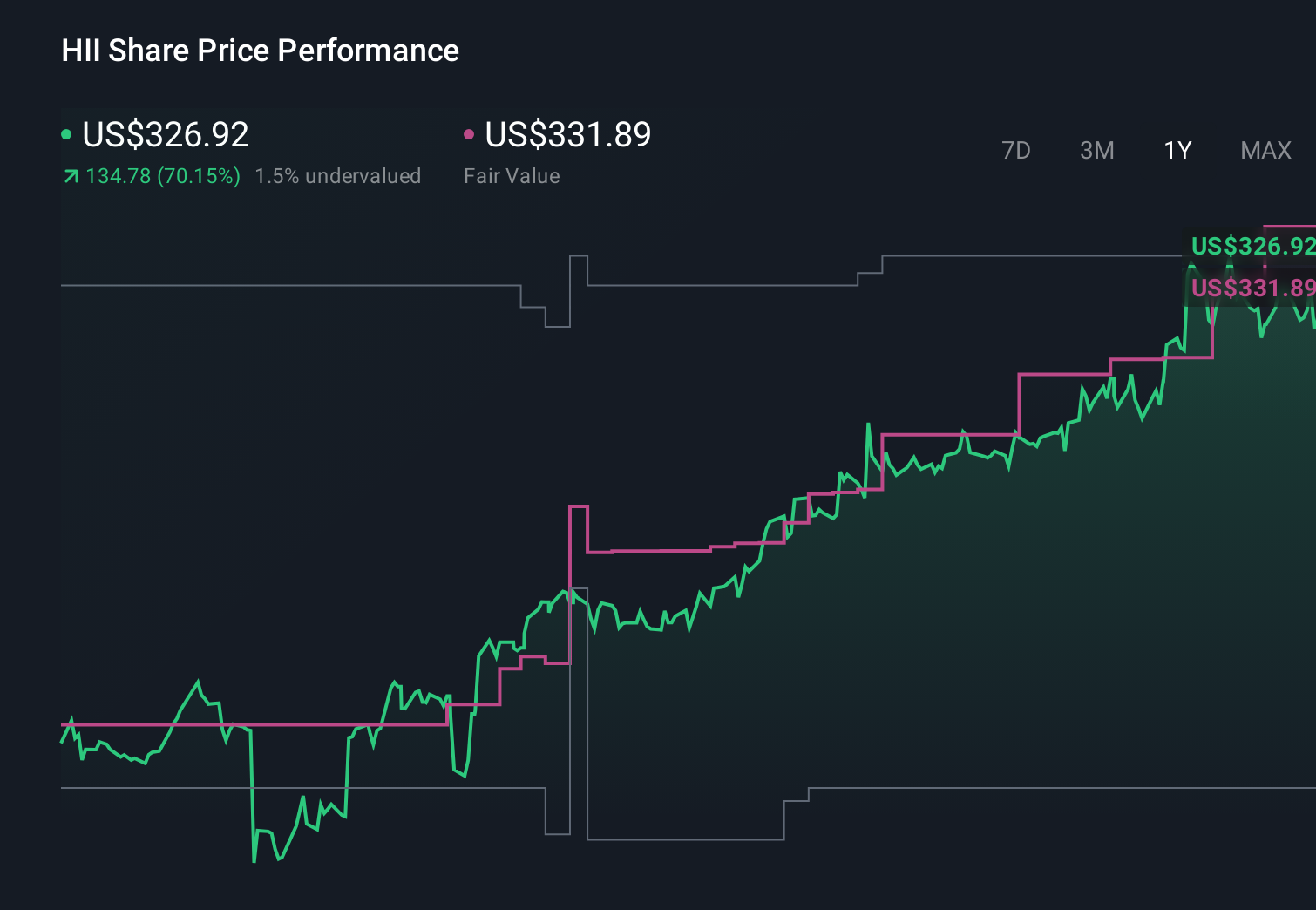

- Next, we’ll examine how this multi-year elevator maintenance contract could influence Huntington Ingalls Industries’ investment narrative and its services mix.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

Huntington Ingalls Industries Investment Narrative Recap

To own Huntington Ingalls Industries, you need to be comfortable with a shipbuilder that still leans on large, long-cycle Navy programs while gradually layering in higher-margin services and autonomy. The new US$418 million elevator sustainment award modestly supports that shift by adding a recurring Mission Technologies revenue stream, but it does not fundamentally change the key near term catalyst of major submarine and carrier contract timing, nor the biggest risk of schedule, cost and labor pressures in the yards.

The REMUS 130 unmanned underwater vehicle delivery to a U.S. ally is the other recent news that best fits this story. It highlights how Mission Technologies is building a parallel, tech-focused portfolio in autonomy and software, which many investors see as a potential counterbalance if funding or priorities for big, manned platforms become more volatile, and a possible support for more stable growth alongside contracts like the new elevator work.

Yet beneath these contracts, investors should also be aware that rising labor and execution risks could still...

Read the full narrative on Huntington Ingalls Industries (it's free!)

Huntington Ingalls Industries' narrative projects $14.6 billion revenue and $912.4 million earnings by 2029. This requires 5.4% yearly revenue growth and about a $307 million earnings increase from $605.0 million today.

Uncover how Huntington Ingalls Industries' forecasts yield a $407.09 fair value, a 46% upside to its current price.

Exploring Other Perspectives

While the new elevator contract supports Mission Technologies, the most optimistic analysts assume HII can reach about US$15.6 billion revenue and US$1.1 billion earnings by 2029, showing how differently you might weigh that upside against concerns about overreliance on large Navy programs and technology transition risks.

Explore 4 other fair value estimates on Huntington Ingalls Industries - why the stock might be worth as much as 56% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Ingalls Industries research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Huntington Ingalls Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Ingalls Industries' overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com