- Baxter International recently published its renamed 2025 Sustainability Report, outlining refreshed environmental, social, and governance priorities, including targets for net-zero greenhouse gas emissions by 2050 and 100% renewable electricity by 2040.

- The company has also created its first chief sustainability officer role and strengthened sustainability governance, signaling a deeper integration of ESG accountability into enterprise-wide decision-making.

- Next, we’ll examine how Baxter’s new net-zero and renewable energy commitments could influence its broader investment narrative and long-term positioning.

AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

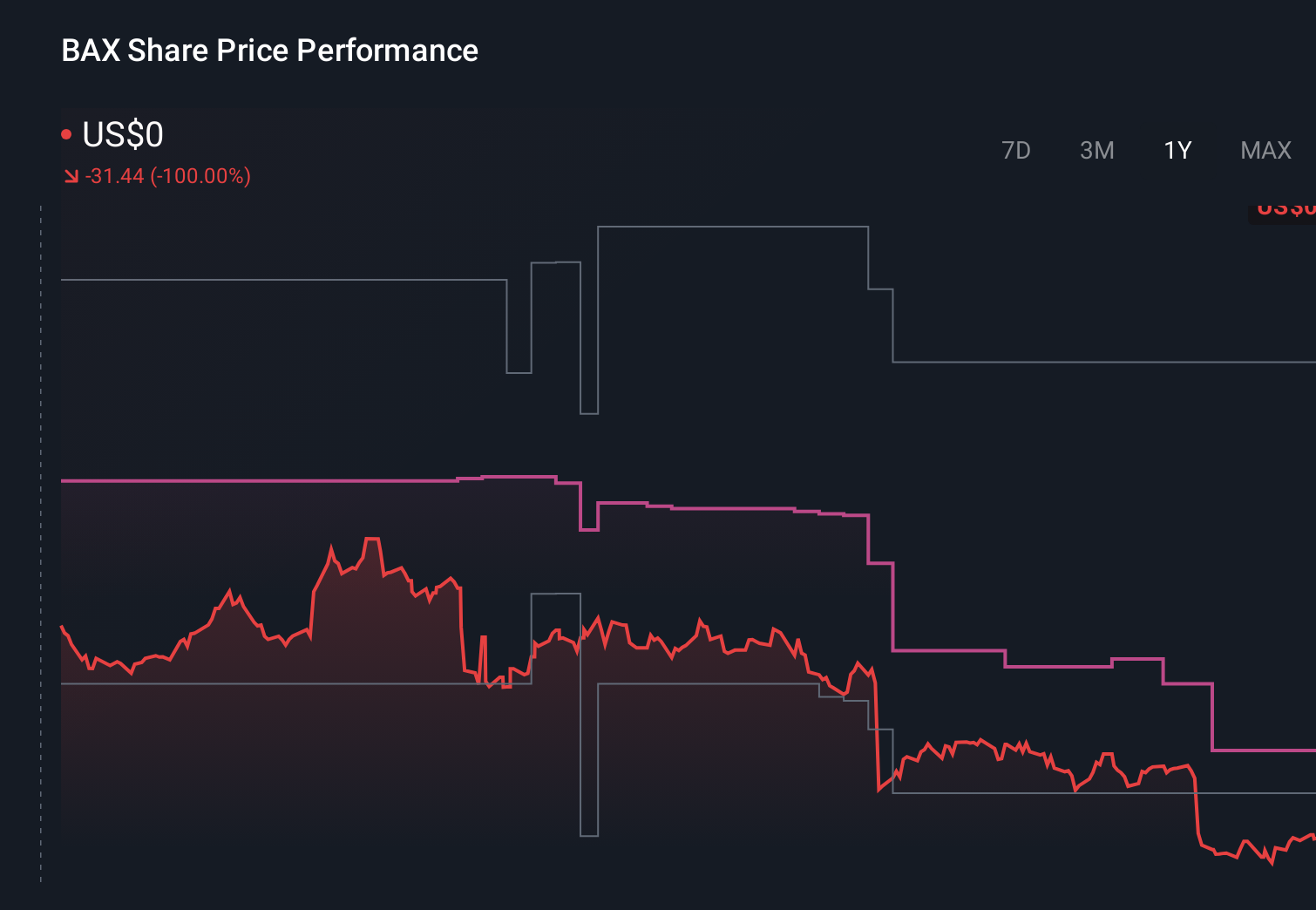

Baxter International Investment Narrative Recap

To own Baxter, you need to believe its core hospital and surgery franchises can translate modest sales growth into improved profitability, despite current losses and margin pressure. The new 2025 Sustainability Report and net zero roadmap do not materially change near term drivers, which still center on stabilizing IV solutions volumes, resolving Novum IQ pump issues, and executing post divestiture cost reductions, with the biggest risk remaining sustained margin compression if volumes and mix do not improve.

The sustainability report’s creation of a chief sustainability officer and tighter ESG governance is most relevant here, because it reinforces board level oversight at a time when Baxter is also reshaping its leadership, capital allocation, and cost structure. For investors watching margin execution, the combination of a refreshed governance framework and ongoing board and executive changes may matter as much as the environmental targets themselves when assessing how effectively the company can manage risk and accountability.

Yet even if Baxter delivers on its ESG goals, investors should be aware that...

Read the full narrative on Baxter International (it's free!)

Baxter International's narrative projects $12.1 billion revenue and $629.2 million earnings by 2029. This requires 2.2% yearly revenue growth and a $1,610.2 million earnings increase from -$981.0 million today.

Uncover how Baxter International's forecasts yield a $21.54 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some analysts were far more optimistic before this news, assuming Baxter could lift margins to 6.3% and earn about US$766.3 million by 2029, but if hospital cost pressure or regulatory scrutiny around devices like Novum IQ intensifies, those forecasts could look very different, so it is worth comparing these upbeat assumptions with more cautious views before you decide which story you find most convincing.

Explore 6 other fair value estimates on Baxter International - why the stock might be worth 26% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Baxter International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Baxter International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Baxter International's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com