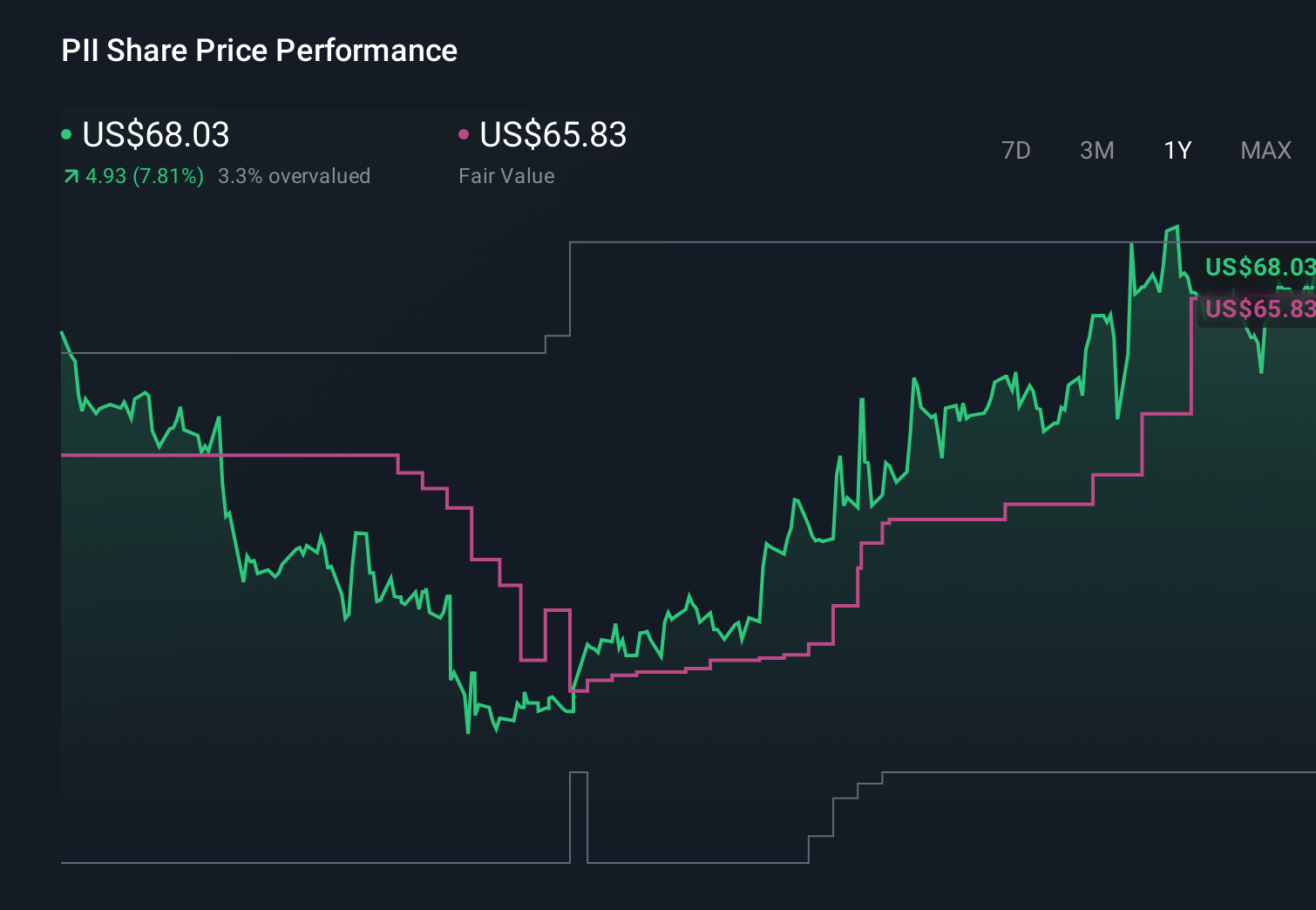

- In recent months, Polaris Inc has seen institutional investors lift their ownership to 111.05% of shares, the highest institutional shareholding score in the Automobiles & Auto Parts industry, with the top holder ETHSX now owning 818.34K shares after a very large increase in its position.

- This surge in institutional participation suggests that professional investors are becoming more engaged with Polaris’ story, potentially amplifying the impact of any changes in its operations, risk profile, or market expectations.

- We’ll now examine how this heightened institutional interest, alongside the recent share price gains, may influence Polaris’ existing investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

Polaris Investment Narrative Recap

To own Polaris, you have to believe it can turn recent losses into sustainable earnings while managing tariffs, soft powersports demand, and elevated financing costs. The sharp rise in institutional ownership reinforces that professional investors are paying closer attention, but it does not fundamentally change the key near term catalyst: evidence that tariff mitigation and cost controls can stabilize margins. The biggest current risk remains that tariffs and weaker consumer demand keep pressuring volumes and profitability despite those efforts.

Against this backdrop, the board’s decision on 4 May 2026 to maintain a regular quarterly dividend of US$0.68 per share stands out. Keeping the dividend flat, after years of small increases, ties directly into the catalyst of careful capital allocation while the business is loss making. It also reminds investors that, alongside institutional buying, Polaris is still balancing shareholder returns with the need to fund tariff mitigation, product innovation, and potential demand softness.

Yet, even with rising institutional interest, investors should be aware that the tariff burden and demand uncertainty could still...

Read the full narrative on Polaris (it's free!)

Polaris' narrative projects $7.8 billion revenue and $425.0 million earnings by 2029.

Uncover how Polaris' forecasts yield a $68.00 fair value, a 5% downside to its current price.

Exploring Other Perspectives

By contrast, the most pessimistic analysts saw tariffs and weak demand as so serious that even with revenue reaching about US$7.7 billion and earnings near US$292 million by 2029, Polaris might still fall short of what today’s buyers expect, so it is worth considering how this fresh surge in institutional ownership could alter that view.

Explore 3 other fair value estimates on Polaris - why the stock might be worth 34% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com