- In recent days, Boot Barn Holdings reported record fiscal 2026 results, with strong same-store sales and rapid store openings drawing praise from analysts and supporting bullish commentary on the business.

- These developments, reinforced by firm U.S. retail sales data in May, have strengthened investor confidence in Boot Barn’s growth-driven expansion story.

- Next, we’ll examine how these strong fiscal results and upbeat analyst commentary influence Boot Barn’s existing investment narrative and risk profile.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn, you have to believe its aggressive store expansion and western and workwear focus can keep attracting customers without eroding margins. The latest record fiscal 2026 results and bullish analyst reactions appear to support the near term growth catalyst of new store openings, while also highlighting the key risk that rapid expansion could eventually pressure returns and profitability. For now, the news reinforces rather than materially alters that balance of opportunity and risk.

Among recent announcements, the plan to open about 70 new stores stands out as most connected to the current discussion. It directly ties into the growth-driven narrative that analysts praised after Boot Barn’s strong same store sales and earnings performance, while also amplifying concerns about higher occupancy costs and the possibility of overexpansion if newer markets do not perform as well as the existing base.

Yet behind the upbeat headlines, investors should also be aware that overextension in newer markets could...

Read the full narrative on Boot Barn Holdings (it's free!)

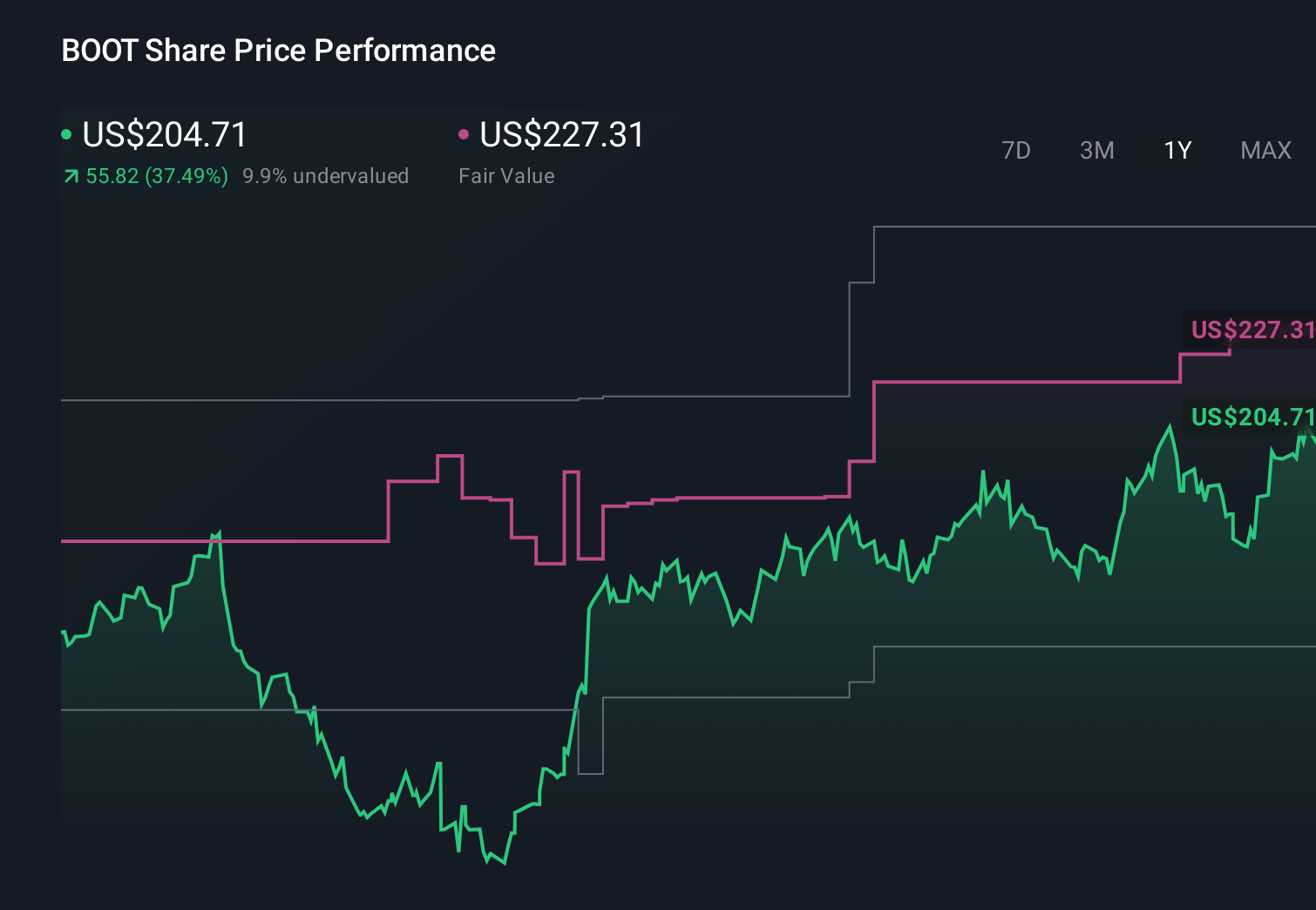

Boot Barn Holdings' narrative projects $3.3 billion revenue and $350.9 million earnings by 2029. This requires 13.9% yearly revenue growth and about a $125 million earnings increase from $225.9 million today.

Uncover how Boot Barn Holdings' forecasts yield a $225.14 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Some lower ranked analysts take a more cautious view, assuming revenue of about US$3.3 billion and earnings near US$333 million by 2029, and worrying that aggressive store growth and tariff exposure could restrain margins more than the recent strong results suggest.

Explore 4 other fair value estimates on Boot Barn Holdings - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com