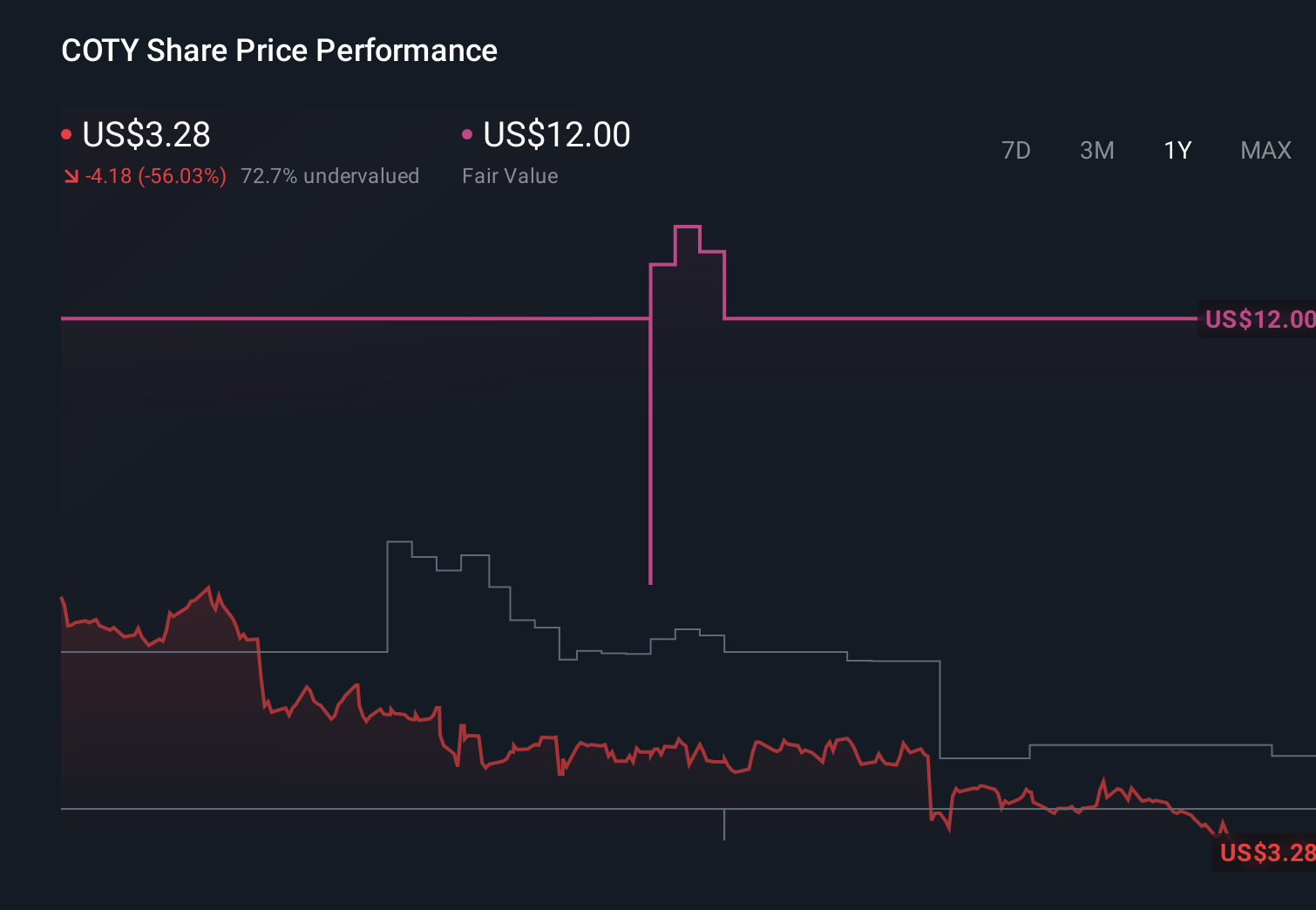

- Coty recently reported declining organic sales in its core beauty business and a weaker growth outlook, prompting fresh concern about the company’s fundamentals.

- This setback is particularly important because it highlights a potential mismatch between earlier expectations for margin improvement and the company’s current operating trends.

- We’ll now assess how concerns over weakening organic sales could reshape Coty’s previously optimistic investment narrative around margins and innovation.

This technology could replace computers: discover 31 stocks that are working to make quantum computing a reality.

Coty Investment Narrative Recap

To stay invested in Coty today, you generally have to believe the company can turn weak organic sales and ongoing losses into a more resilient, profitable beauty portfolio. The latest drop in core beauty sales directly challenges that belief, because it undercuts the near term catalyst of margin recovery while amplifying the biggest current risk around shaky fundamentals and continued stock price pressure.

The recent launch of the Marc Jacobs Beauty color cosmetics line is especially relevant here, because it is positioned as a high profile innovation meant to support growth in Coty’s core categories. Against the backdrop of declining organic sales and recent earnings losses, this launch becomes a test of whether Coty’s new products can offset category softness and help rebuild confidence in its ability to grow revenue and improve profitability over time.

Yet investors should also be aware that weakening organic sales could compound Coty’s already elevated debt burden and refinancing needs, which...

Read the full narrative on Coty (it's free!)

Coty's narrative projects $5.9 billion revenue and $411.8 million earnings by 2029.

Uncover how Coty's forecasts yield a $3.17 fair value, a 63% upside to its current price.

Exploring Other Perspectives

Compared with the baseline story, the most pessimistic analysts sound far more cautious, even before this setback. They were assuming essentially flat revenue around US$5.8 billion and only US$239.5 million of earnings by 2029, which sits uncomfortably against fresh signs of softer organic sales and highlights how widely your view on Coty’s risks and catalysts can differ from others.

Explore 5 other fair value estimates on Coty - why the stock might be worth over 5x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com