Why Pursuit Attractions and Hospitality Is Back on Investors’ Radar

Pursuit Attractions and Hospitality (PRSU) has drawn fresh attention after reporting a 37.42% year-over-year rise in quarterly revenue and 19.91% growth in net profit, alongside higher institutional ownership from large asset managers.

See our latest analysis for Pursuit Attractions and Hospitality.

The strong quarterly update and increased institutional interest in Pursuit Attractions and Hospitality line up with a 14.34% 1-month share price return and a 52.47% year-to-date share price return. The 87.21% 1-year total shareholder return points to building momentum rather than a short-lived spike.

If this kind of renewed interest has your attention, it can be useful to see what else is gaining traction, starting with 20 top founder-led companies

With Pursuit Attractions and Hospitality posting double digit revenue and profit growth, strong recent returns and a share price that sits only slightly below analysts’ targets, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 2.5% Undervalued

On the most followed narrative, Pursuit Attractions and Hospitality looks slightly cheaper than its fair value of $52.25 when set against the latest close at $50.94. This puts the focus squarely on the growth and margin story behind that gap.

Significant long-term pipeline of organic reinvestment ("Refresh and Build" projects) and disciplined acquisition strategy (with financial flexibility for larger and smaller deals) provides opportunities to scale, drive operational leverage, and enhance earnings reliability and growth over multiple years.

Want to see what that pipeline really implies for Pursuit Attractions and Hospitality? The narrative leans on earnings compounding, rising margins, and a richer future earnings multiple. Curious which combination of growth and profitability has been used to reach that $52.25 mark and how sensitive it is to those assumptions? The full breakdown spells it out in black and white.

Result: Fair Value of $52.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Pursuit Attractions and Hospitality story could be tested if high capital spending on projects like Hotel Whitefish fails to pay off, or if climate related disruptions hit key destinations.

Find out about the key risks to this Pursuit Attractions and Hospitality narrative.

Another View on Pursuit Attractions and Hospitality’s Valuation

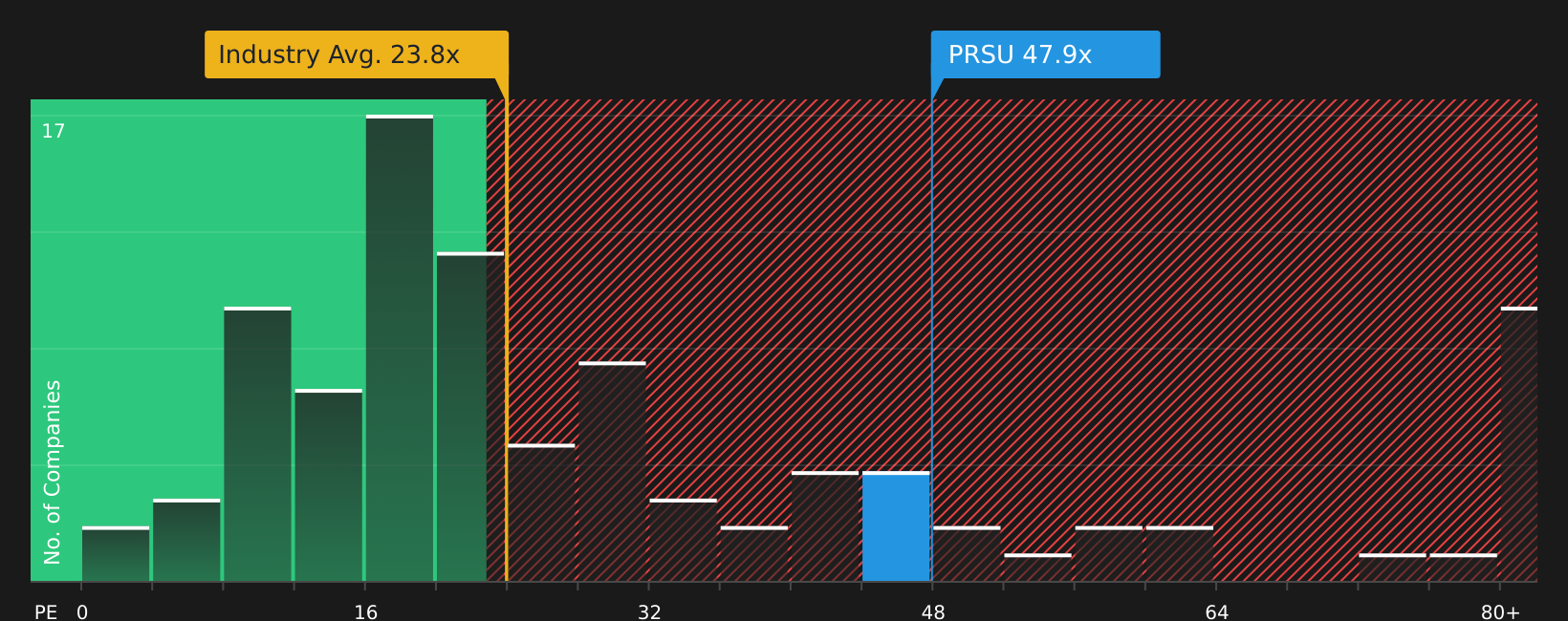

The fair value narrative pegs Pursuit Attractions and Hospitality at $52.25, suggesting the current $50.94 share price is about 2.5% below that mark. On earnings multiples, though, the stock trades on a P/E of 44.9x versus 23.2x for the US Hospitality industry and a 23x fair ratio. This points to a rich valuation if growth or margins fall short of expectations, which raises the question of which signal to rely on more when weighing the risk of overpaying.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of optimism and caution around Pursuit Attractions and Hospitality feels finely balanced, it makes sense to check the data yourself and move quickly while sentiment is still forming, starting with 2 key rewards

Looking for More Investment Ideas Beyond Pursuit Attractions and Hospitality?

If Pursuit Attractions and Hospitality has sharpened your focus, use this momentum to scan the market for other opportunities before they move out of reach.

- Spot potential upside early by reviewing a curated group of screener containing 19 high quality undiscovered gems that pair quality fundamentals with relatively low market attention.

- Strengthen your defensive side by filtering for 66 resilient stocks with low risk scores that aim to keep volatility in check while you pursue returns.

- Target resilient balance sheets by assessing companies in the solid balance sheet and fundamentals stocks screener (48 results) that prioritize financial strength and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com