- Earlier in June 2026, Bruker Corporation filed an omnibus shelf registration covering a wide range of securities and showcased expanded infectious disease diagnostics capabilities, including new FDA-cleared enhancements for its MALDI Biotyper CA System and advanced workflows for rapid antimicrobial susceptibility testing.

- By pairing a broad financing toolkit with an enlarged microbiology and molecular diagnostics portfolio, Bruker is signaling both product ambition and flexibility in how it might fund future growth initiatives.

- Next, we’ll examine how Bruker’s broadened infectious disease diagnostics portfolio could influence its existing investment narrative and risk‑reward profile.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Bruker Investment Narrative Recap

To own Bruker, you need to be comfortable with a company that is trying to offset choppy research spending with higher value diagnostics and software rich workflows. The new shelf registration gives Bruker more optionality, but it does not materially change the near term catalyst, which is execution on cost savings and portfolio expansion, or the key risk, which remains weak academic and biopharma funding in the US and China.

The expanded FDA cleared capabilities for the MALDI Biotyper CA System are the most relevant development here, because they add depth to Bruker’s infectious disease diagnostics portfolio at a time when analysts already expect only modest revenue growth. How quickly laboratories adopt these upgraded workflows will matter for Bruker’s ability to lean more on consumables and software based recurring revenue, rather than relying solely on large research instrument budgets.

Yet beneath the promising diagnostics updates, investors still need to watch for signs that prolonged funding and order softness could...

Read the full narrative on Bruker (it's free!)

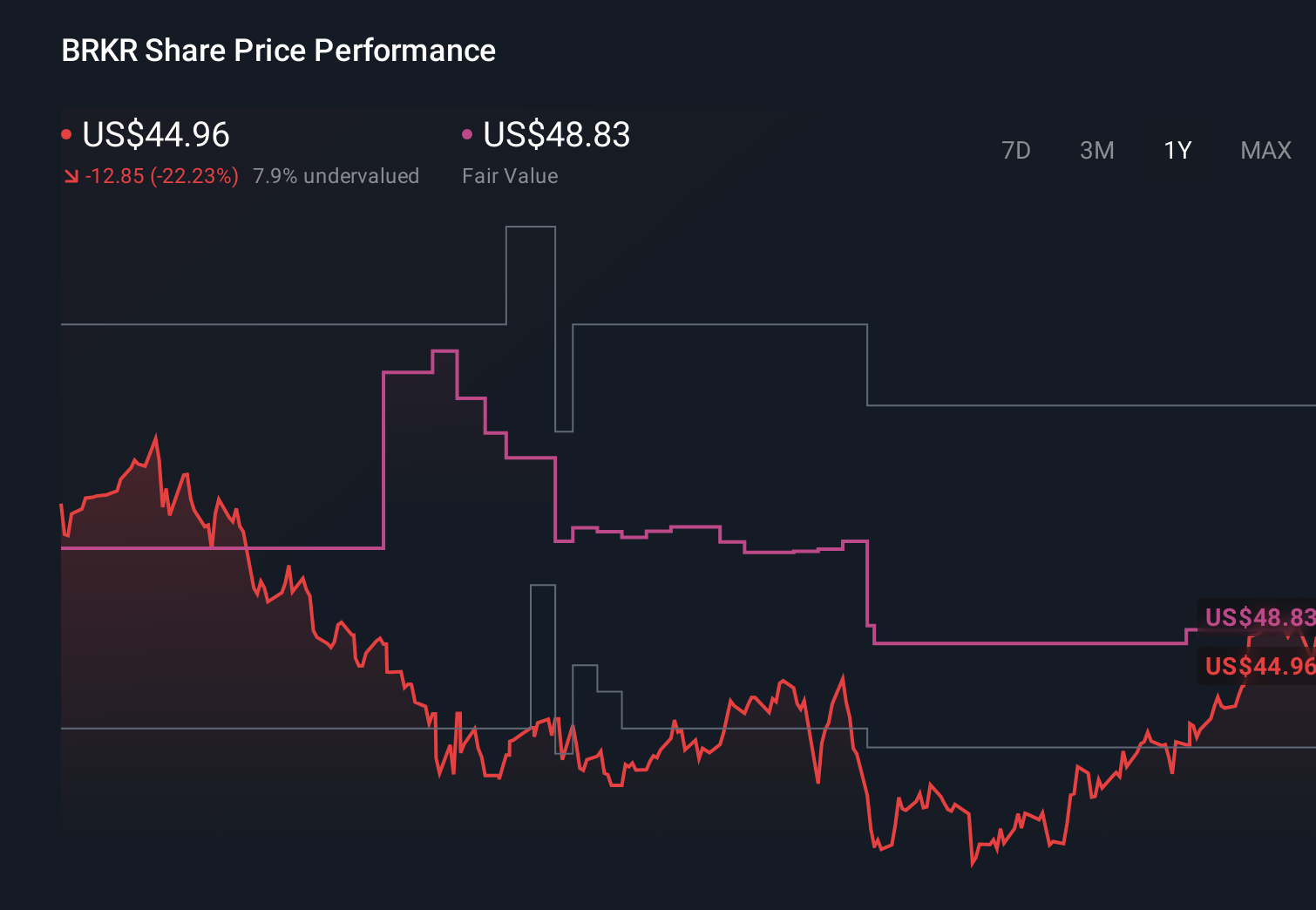

Bruker's narrative projects $4.0 billion revenue and $328.4 million earnings by 2029. This requires 5.1% yearly revenue growth and a $364.8 million earnings increase from -$36.4 million today.

Uncover how Bruker's forecasts yield a $53.25 fair value, a 5% downside to its current price.

Exploring Other Perspectives

While consensus assumes Bruker can grow revenue about 4 percent annually with improving margins, the most pessimistic analysts see US$3.9 billion of revenue and US$322.6 million of earnings by 2029 as far from assured, especially if academic funding and cost pressures play out closer to their harsher expectations.

Explore 4 other fair value estimates on Bruker - why the stock might be worth 44% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bruker research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bruker research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bruker's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com