Pool (POOL) has drawn investor attention as its shares trade around US$198, with recent returns mixed over the past year and longer horizons. This has prompted fresh interest in how the stock’s fundamentals stack up.

See our latest analysis for Pool.

Recent trading shows Pool stock rebounding in the short term, with a 1 month share price return of 12.96%, while longer term total shareholder returns over 1, 3 and 5 years have declined. This suggests that momentum is still rebuilding.

If Pool has you reassessing where growth and resilience might come from next, it could be worth scanning the market using our curated list of 20 top founder-led companies

So with Pool stock trading around US$198 and recent returns under pressure over the past few years, are investors looking at an undervalued pool supplies leader here, or is the market already pricing in any future growth?

Most Popular Narrative: 22.6% Undervalued

Pool stock last closed at $198.08, while the most followed narrative pegs fair value at about $255.91, framing a sizable valuation gap to unpack.

Growing consumer emphasis on home-based leisure and wellness is maintaining structurally elevated demand for pools and related services, driving resilient recurring revenue for maintenance and enhancements, which should support top-line stability and growth even during new construction lulls.

Curious what underpins that fair value for Pool? The narrative leans heavily on steady revenue expansion, firmer margins and a richer future earnings multiple. The full story brings these moving pieces together into one valuation roadmap.

Result: Fair Value of $255.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Pool investors still need to factor in the drag from softer US housing activity and inflationary cost pressures, which could challenge those earnings and margin assumptions.

Find out about the key risks to this Pool narrative.

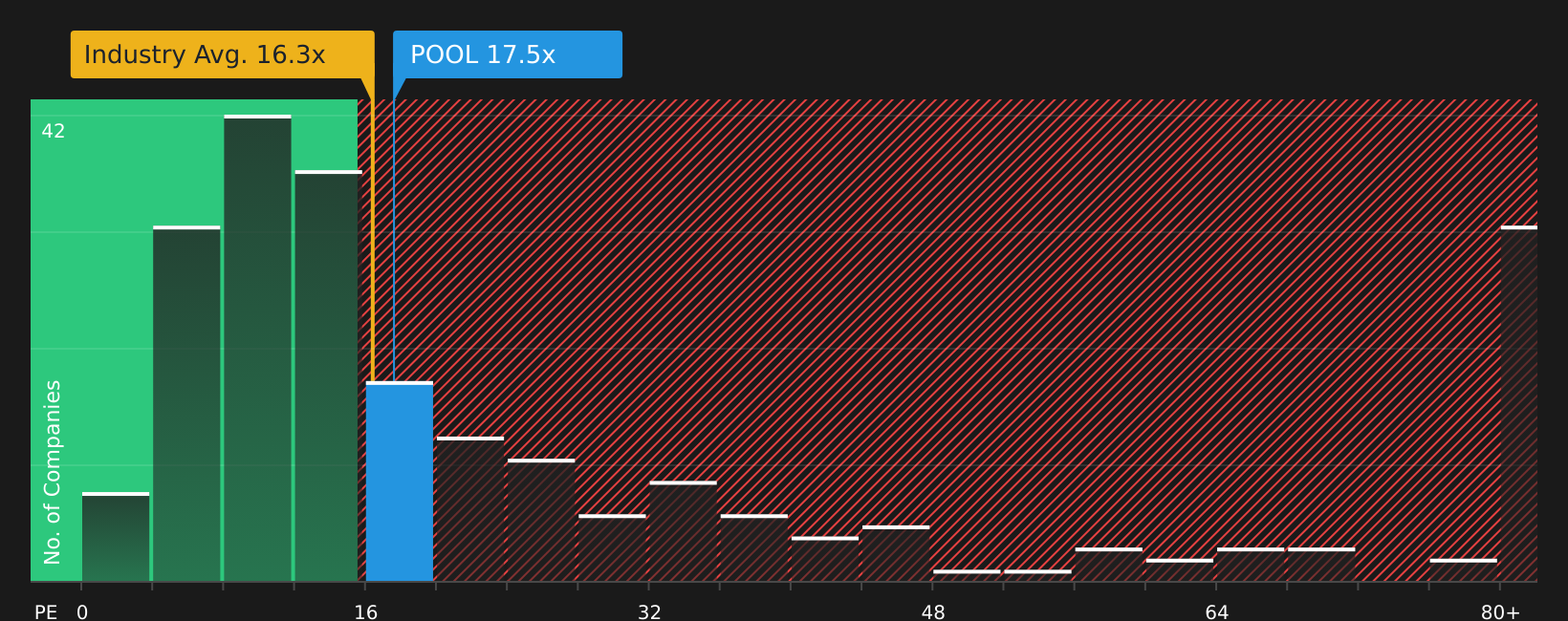

Another View on Pool Stock: What Do Earnings Multiples Say?

While the most followed Pool narrative and analyst target frame the stock as undervalued against a fair value of $255.91, the current P/E of 17.9x paints a different picture. It sits above the Global Retail Distributors average of 15.7x and the fair ratio of 13.9x, which suggests less margin for error if growth or profitability disappoints. This raises the question of whether the discount to fair value is a genuine opportunity or simply compensation for this richer earnings multiple.

To see how these earnings ratios stack up in more detail and what they might imply for valuation risk over time, check the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals around Pool’s valuation and earnings multiples, it makes sense to move quickly and examine the underlying data for yourself, including the balance of 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Pool stock?

If Pool has sharpened your focus on valuation and quality, now is the time to broaden your watchlist with other targeted opportunities built from the same data engine.

- Target potential mispricings by scanning a curated list of 44 high quality undervalued stocks before other investors catch on.

- Strengthen your income strategy by reviewing companies in the 9 dividend fortresses that meet your yield and stability preferences.

- Protect your capital by filtering for companies in the 68 resilient stocks with low risk scores that align with a steadier risk profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com