- Earlier this week, InterDigital announced a new patent license agreement with Amazon covering services and devices including Prime Video, alongside a regular US$0.70 per‑share quarterly dividend payable in July 2026 to shareholders of record on July 8, 2026.

- The Amazon agreement, which resolves all pending litigation and moves remaining terms into binding arbitration, highlights the central role of InterDigital’s intellectual property in video streaming and broad connected-device ecosystems.

- We’ll now examine how the Amazon licensing deal and litigation resolution may influence InterDigital’s investment narrative and perceived earnings durability.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

InterDigital Investment Narrative Recap

To own InterDigital, you need to be comfortable with a licensing model where long-term contracts and patent renewals drive value, while legal disputes and standard‑setting outcomes remain key swing factors. The Amazon license and litigation resolution appear to reinforce the near term catalyst of scaling video streaming and connected‑device royalties, while also reducing one of the more immediate legal and earnings volatility risks, even though the final economics will depend on binding arbitration outcomes that have not yet been disclosed.

Among recent announcements, the reiterated US$0.70 per share quarterly dividend, payable in July 2026, matters because it underlines management’s confidence in ongoing cash generation despite softer recent earnings and active arbitration and litigation activity. For investors focused on catalysts, a consistent and rising dividend track record can make it easier to look through quarter‑to‑quarter noise as InterDigital pushes deeper into areas like video streaming, consumer electronics, IoT, and future 6G‑related licensing opportunities.

But despite this progress, investors should also be aware of growing legal and enforcement costs that could...

Read the full narrative on InterDigital (it's free!)

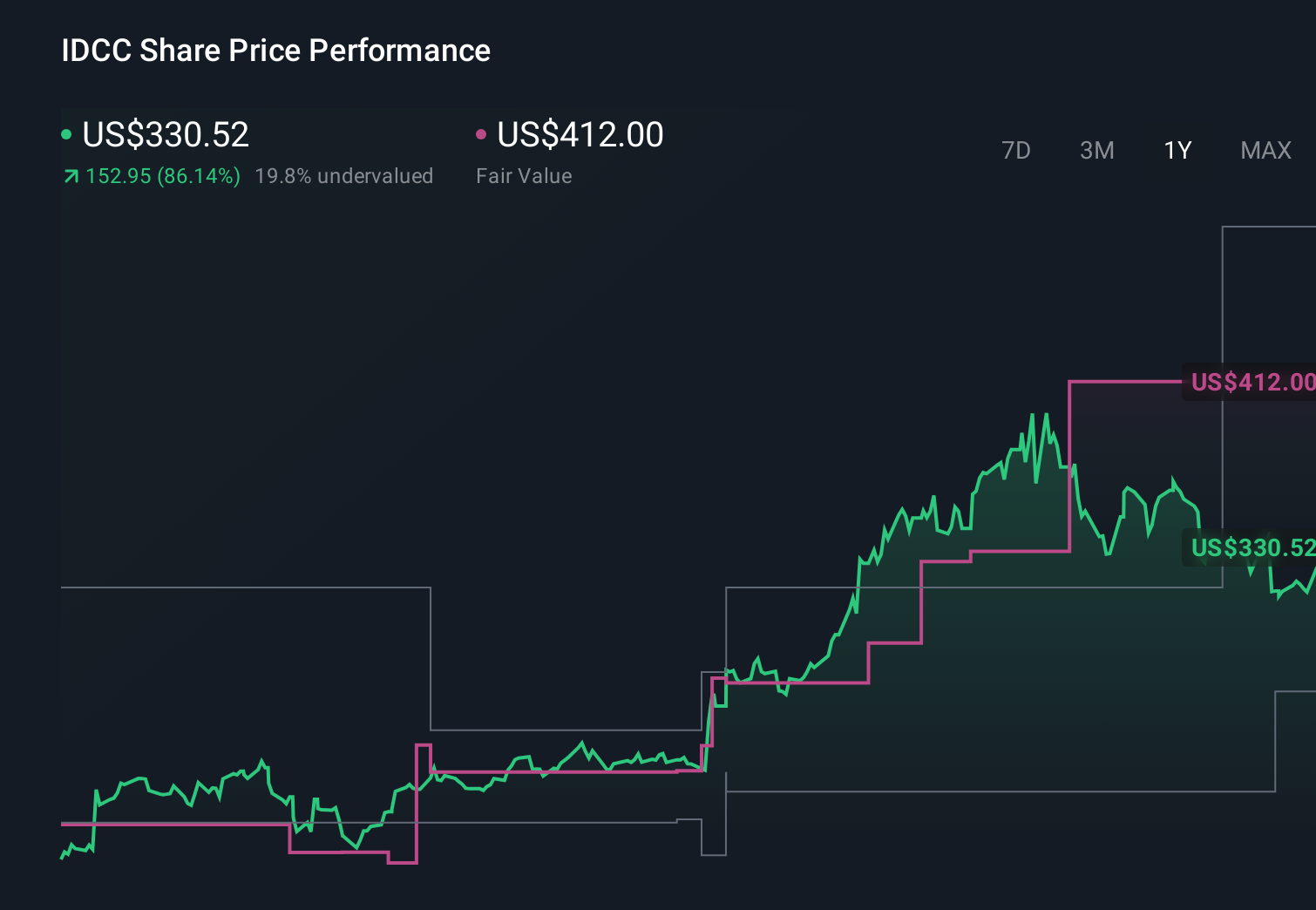

InterDigital’s narrative projects $824.6 million revenue and $350.8 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 63% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming about US$1.0 billion of 2029 revenue and US$504.9 million in earnings, and highlighting rising regulatory and legal pressures that could make monetizing big wins like Amazon much tougher than today’s consensus implies.

Explore 5 other fair value estimates on InterDigital - why the stock might be worth less than half the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com