Why Century Communities (CCS) is on investors’ radar

Century Communities (CCS) has drawn fresh attention after recent share price moves, with the stock closing at US$60.66. That puts renewed focus on how its homebuilding and financial services operations are currently priced.

See our latest analysis for Century Communities.

Recent trading has been strong, with a 14.28% 1 month share price return and a 7.94% 7 day share price return. The 1 year total shareholder return of 13.08% contrasts with weaker 3 year results, which suggests that momentum has only recently improved.

If CCS’s rebound has you thinking more broadly about opportunities in housing related and cyclical stories, it may be worth scanning the wider market using the 20 top founder-led companies

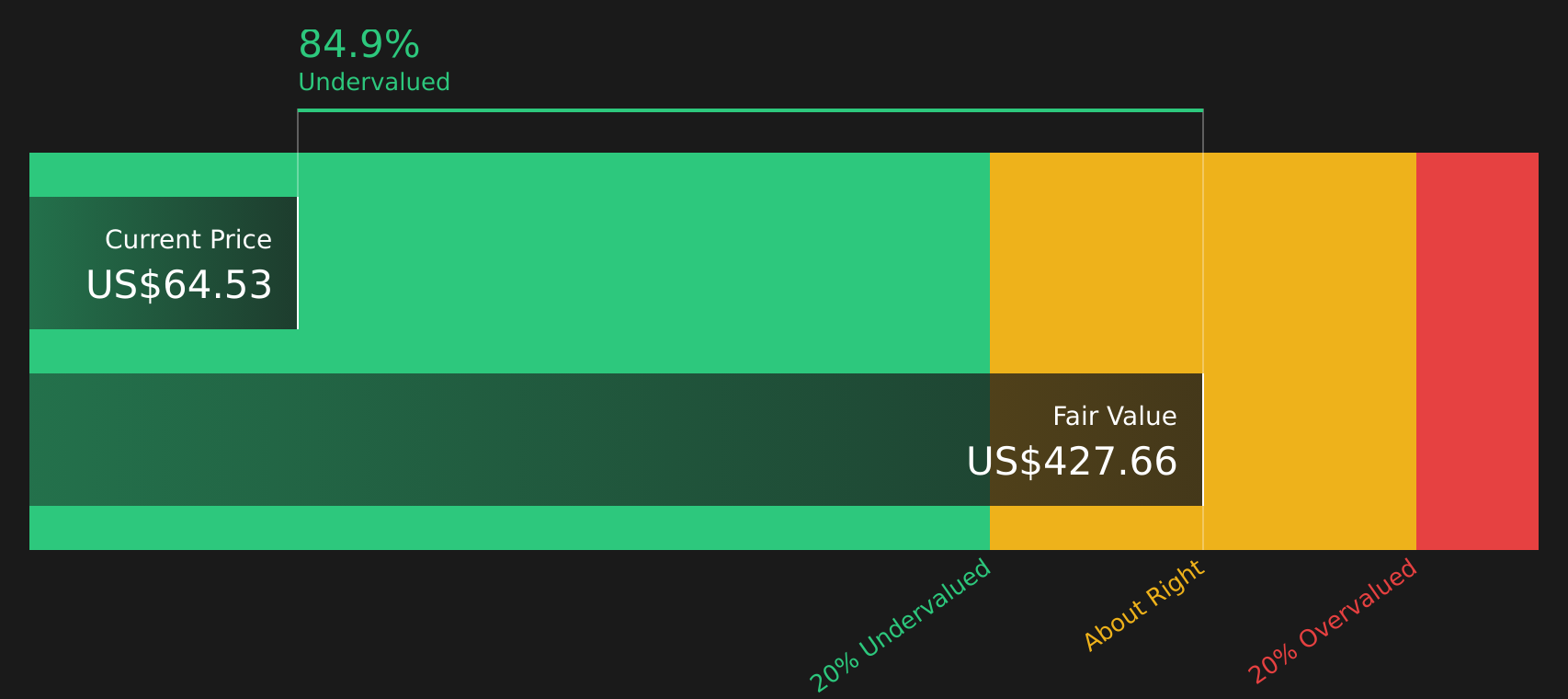

So with CCS trading around US$60.66, modest annual revenue and net income changes, and a market value of about US$1.6b, is the recent strength still leaving room for upside, or is the stock already pricing in future growth?

Most Popular Narrative: 9.5% Undervalued

Century Communities’ most followed valuation narrative pegs fair value at $67, compared with the last close at $60.66, which puts a spotlight on what assumptions sit underneath that gap.

Ongoing elevated mortgage rates and affordability constraints are dampening homebuyer demand, forcing Century Communities to increase sales incentives and accept lower average selling prices, which is already putting downward pressure on gross margins and is expected to weigh further on both revenues and earnings in the coming quarters. The company's reliance on price-sensitive entry-level buyers leaves it especially vulnerable to any further deterioration in affordability, shrinking the potential customer base and increasing the risk of slower sales volume and lower top-line growth.

Want to understand why this cautious demand outlook still results in a higher fair value estimate? The narrative leans on detailed revenue paths, margin compression assumptions, and a meaningfully higher future earnings multiple. Curious how those moving parts add up to $67 instead of $60.66? The full narrative lays out the math behind that call.

Result: Fair Value of $67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear risks, including weaker homebuyer demand in key regions, as well as pressure on margins from affordability constraints and higher build and land costs.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Paint A Tougher Picture

The analyst narrative argues CCS is about 9.5% undervalued at $67, but the Simply Wall St DCF model tells a different story. On that cash flow view, CCS at $60.66 is trading well above an estimated value of $22.65, which implies meaningful downside risk instead of upside. Which picture lines up more closely with your own assumptions on margins, growth, and discount rates?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Century Communities for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mixed messages on value and cash flows make this a good moment to look at the data yourself and move quickly to shape your view. A clear next step is to weigh both concerns and potential upside by checking the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If CCS has sharpened your view on housing stocks, do not stop there. Broaden your watchlist now so you are not late to the next idea.

- Target resilient companies by screening for 67 resilient stocks with low risk scores that may hold up better when conditions get choppy.

- Spot potential bargains early by running the screener containing 20 high quality undiscovered gems that focuses on quality businesses the crowd may be overlooking.

- Strengthen your core holdings with the solid balance sheet and fundamentals stocks screener (47 results) to focus on companies backed by healthier finances.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com