Over the last 7 days, the United States market has experienced a 4.1% drop, yet it remains up by 21% over the past year with anticipated earnings growth of 18% per annum in the coming years. In this fluctuating environment, identifying stocks that may be priced below their estimated value can offer potential opportunities for investors seeking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Western Digital (WDC) | $490.09 | $963.12 | 49.1% |

| Solstice Advanced Materials (SOLS) | $77.69 | $154.41 | 49.7% |

| Rayonier (RYN) | $20.69 | $40.79 | 49.3% |

| MercadoLibre (MELI) | $1588.29 | $3090.91 | 48.6% |

| Live Oak Bancshares (LOB) | $38.21 | $74.21 | 48.5% |

| Kingstone Companies (KINS) | $15.84 | $31.31 | 49.4% |

| Gold Royalty (GROY) | $2.70 | $5.32 | 49.2% |

| Bowhead Specialty Holdings (BOW) | $27.08 | $52.60 | 48.5% |

| Alkami Technology (ALKT) | $15.01 | $29.64 | 49.4% |

| AbbVie (ABBV) | $224.95 | $440.96 | 49% |

Let's review some notable picks from our screened stocks.

First Community (FCCO)

Overview: First Community Corporation, with a market cap of $298.10 million, operates as the bank holding company for First Community Bank, offering a range of commercial and retail banking products and services to small-to-medium sized businesses, professionals, and individuals.

Operations: The company generates revenue through several segments, including Commercial and Retail Banking ($65.40 million), Mortgage Banking ($9.49 million), Investment Advisory and Non-Deposit services ($8.03 million), and the Corporate Segment ($6.81 million).

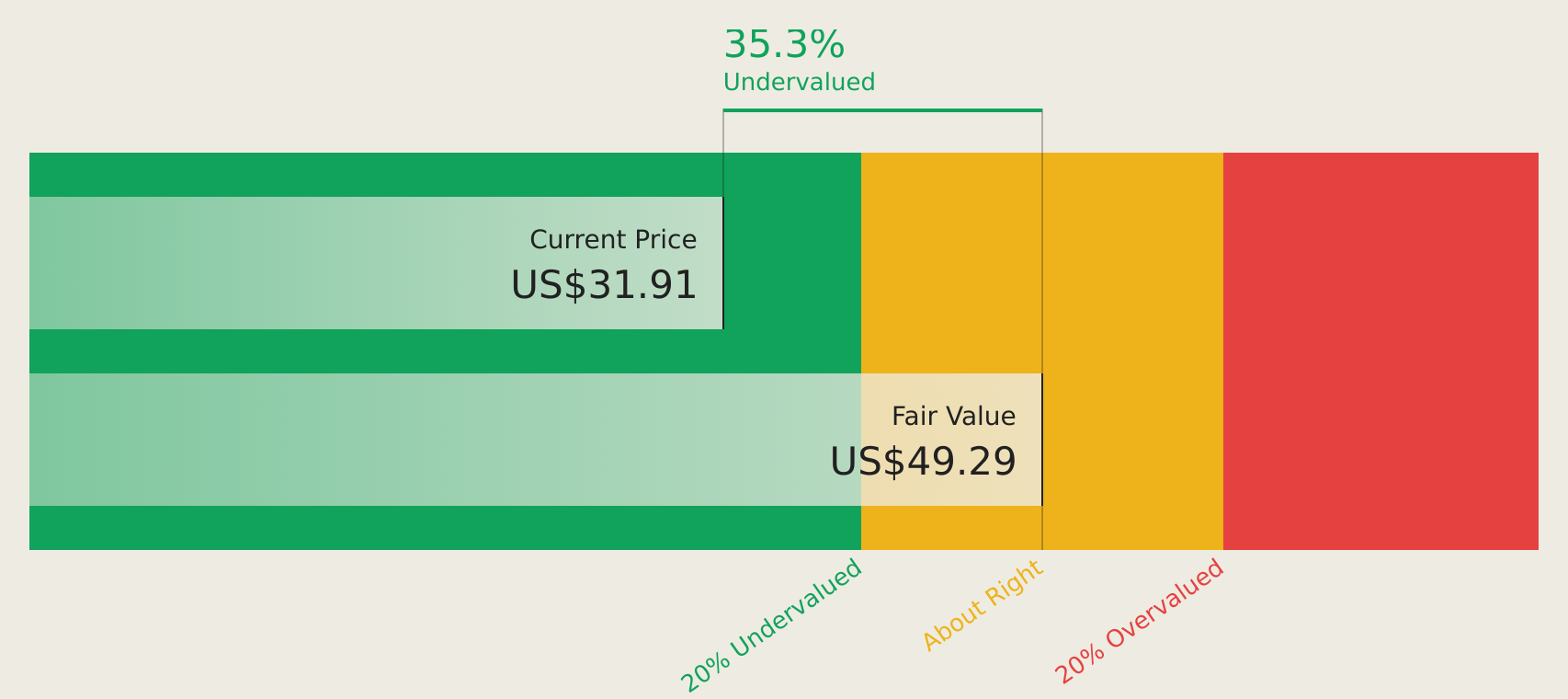

Estimated Discount To Fair Value: 35.1%

First Community Corporation appears undervalued, trading at 35.1% below its estimated fair value and over 20% below its future cash flow value. The company reported net interest income of US$18.37 million for Q1 2026, with net income rising to US$5.5 million from the previous year. Despite recent shareholder dilution, earnings are forecast to grow significantly at over 20% annually, supported by a share repurchase program worth up to US$7.5 million expiring in May 2027.

- According our earnings growth report, there's an indication that First Community might be ready to expand.

- Click to explore a detailed breakdown of our findings in First Community's balance sheet health report.

Chemung Financial (CHMG)

Overview: Chemung Financial Corporation is a bank holding company for Chemung Canal Trust Company, offering various banking, financing, fiduciary, and financial services with a market cap of $344.47 million.

Operations: The company's revenue segments include Core Banking at $84.59 million and Wealth Management Group (WMG) at $12.22 million, with adjustments from Holding Company and Cfs Group, Inc. (CFS) accounting for -$1.44 million.

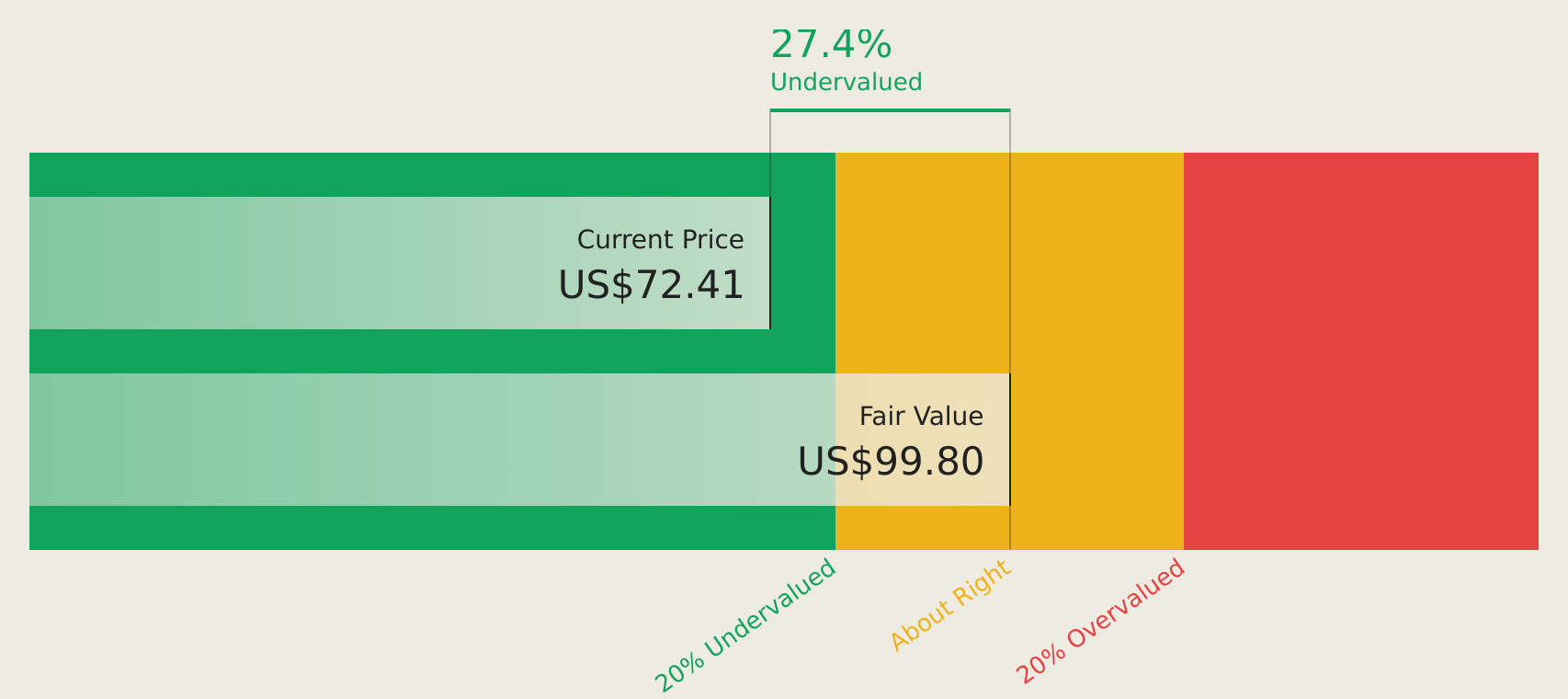

Estimated Discount To Fair Value: 27.6%

Chemung Financial is trading at US$72.23, below its estimated future cash flow value of US$99.77, suggesting undervaluation. Earnings are projected to grow significantly at 35% annually, outpacing the broader US market's growth forecast. Despite insider selling and moderate revenue growth expectations of 17.6%, recent earnings reports show strong performance with net income rising to US$9.2 million for Q1 2026 from the previous year’s US$6.02 million, supporting its investment appeal based on cash flows.

- Our growth report here indicates Chemung Financial may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Chemung Financial.

Consolidated Water (CWCO)

Overview: Consolidated Water Co. Ltd., operating through its subsidiaries, supplies potable water, treats wastewater, and offers water-related products and services across the Cayman Islands, the Bahamas, the United States, and the British Virgin Islands with a market cap of $482.57 million.

Operations: Consolidated Water's revenue segments are comprised of Bulk ($33.81 million), Retail ($32.75 million), Manufacturing ($14.28 million), and Services Excluding Manufacturing ($47.49 million).

Estimated Discount To Fair Value: 17.5%

Consolidated Water, priced at US$30.09, trades below its estimated future cash flow value of US$36.48, indicating potential undervaluation based on cash flows. While earnings grew 10.4% last year and are forecast to grow 19.9% annually, revenue is expected to rise 24.5%, surpassing market averages. Recent strategic hires and expansion plans in desalination and water infrastructure signal growth opportunities despite a slight decline in Q1 earnings compared to the previous year.

- The analysis detailed in our Consolidated Water growth report hints at robust future financial performance.

- Take a closer look at Consolidated Water's balance sheet health here in our report.

Where To Now?

- Discover the full array of 139 Undervalued US Stocks Based On Cash Flows right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com