Polaris (PII) is back on investors’ radar after its off-road vehicles swept the UTV overall podium at the SCORE Baja 500, while management focuses on supply chain adjustments and cost controls related to tariffs.

See our latest analysis for Polaris.

The recent UTV racing success comes as the stock shows improving momentum, with a 90 day share price return of 29.87% and a 1 year total shareholder return of 70.20%, while longer term total shareholder returns over three and five years remain weak.

If this kind of performance shift has your attention, it may be worth scanning other powersports and recreational equipment players through the 20 top founder-led companies

With Polaris shares up 70.20% over the past year and trading slightly above one analyst target, while some models flag potential overvaluation, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 2.2% Overvalued

Polaris closed at $69.47 against a most followed fair value estimate of $68.00, a small premium that puts the focus on what is driving that number.

Polaris is focused on a strategic approach to mitigate the impact of tariffs through supply chain adjustments and cost control initiatives, which could potentially preserve net margins and improve earnings over time.

Analysts are effectively sketching a turnaround map built on steadier revenue, a swing from losses to profits, and a re rated earnings multiple. Want to see how those moving parts fit together.

Result: Fair Value of $68.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear watchpoints, including the withdrawn full year guidance around tariffs and the forecast range of US$320 million to US$370 million in gross tariff costs.

Find out about the key risks to this Polaris narrative.

Another View: Sales Multiple Paints A Cheaper Picture

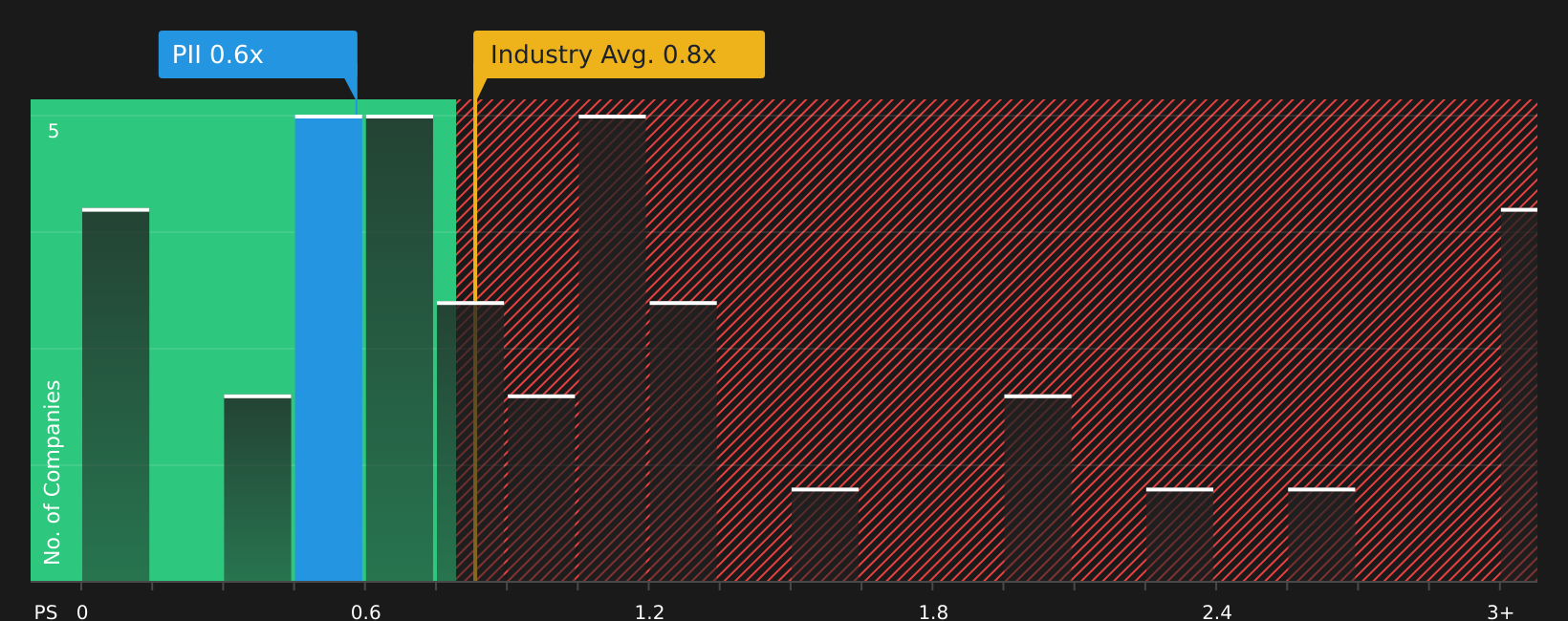

While the analyst fair value implies Polaris is slightly overvalued, the current P/S of 0.5x looks lower than the fair ratio of 0.6x and well below both the US Leisure industry at 0.9x and peers at 1.2x. That gap suggests the stock carries more caution than its sales line alone might imply.

This leaves a simple question for you: is the discount on sales a warning about future execution, or a chance to back a recovery story at a lower multiple?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed signals here leave you unsure, move quickly to review the full picture and weigh both the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop your research with a single stock. Broaden your watchlist using focused stock lists that surface different types of opportunities across quality, value and income.

- Target dependable balance sheets by scanning companies in the solid balance sheet and fundamentals stocks screener (46 results) to spot businesses backed by stronger financial foundations.

- Hunt for potential value opportunities by reviewing the 46 high quality undervalued stocks that highlight stocks combining quality fundamentals with pricing that may look more attractive.

- Build a watchlist of under followed prospects by checking the screener containing 21 high quality undiscovered gems and see which companies the market might not be paying close attention to yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com