Acushnet Holdings (GOLF) is back on investors’ radar after a recent move in the share price, with the stock last closing at US$90. That puts fresh focus on how its golf focused business is currently valued.

See our latest analysis for Acushnet Holdings.

Recent trading has been mixed, with the 1 day share price return of 1.14% and year to date share price return of 9.61% set against a weaker 90 day share price return. However, the 1 year total shareholder return of 25.73% and 5 year total shareholder return of 93.24% point to momentum that has been building over time.

If this move in GOLF has you thinking about where else capital could work harder, it may be worth scanning 20 top founder-led companies

With GOLF trading at US$90 against an analyst price target of US$96 and an estimated intrinsic value gap of about 17%, the key question is whether this signals genuine undervaluation or indicates that markets are already pricing in future growth.

Most Popular Narrative: 6.2% Undervalued

At a last close of $90 against a narrative fair value of $96, the current setup frames GOLF as modestly discounted with room for debate on what assumptions support that gap.

Secular demand growth, premium products, geographic diversity, and operational efficiency support Acushnet's resilience, margin strength, and commitment to shareholder value.

Want to see what sits behind that confidence in resilience and margins? The narrative leans on measured revenue growth, firmer profitability, and a future earnings multiple that has to work hard to justify today’s fair value.

Result: Fair Value of $96 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could unravel if golf participation stalls or reverses, or if tariffs and inflation squeeze margins harder than analysts currently assume.

Find out about the key risks to this Acushnet Holdings narrative.

Another Way To Look At The Price

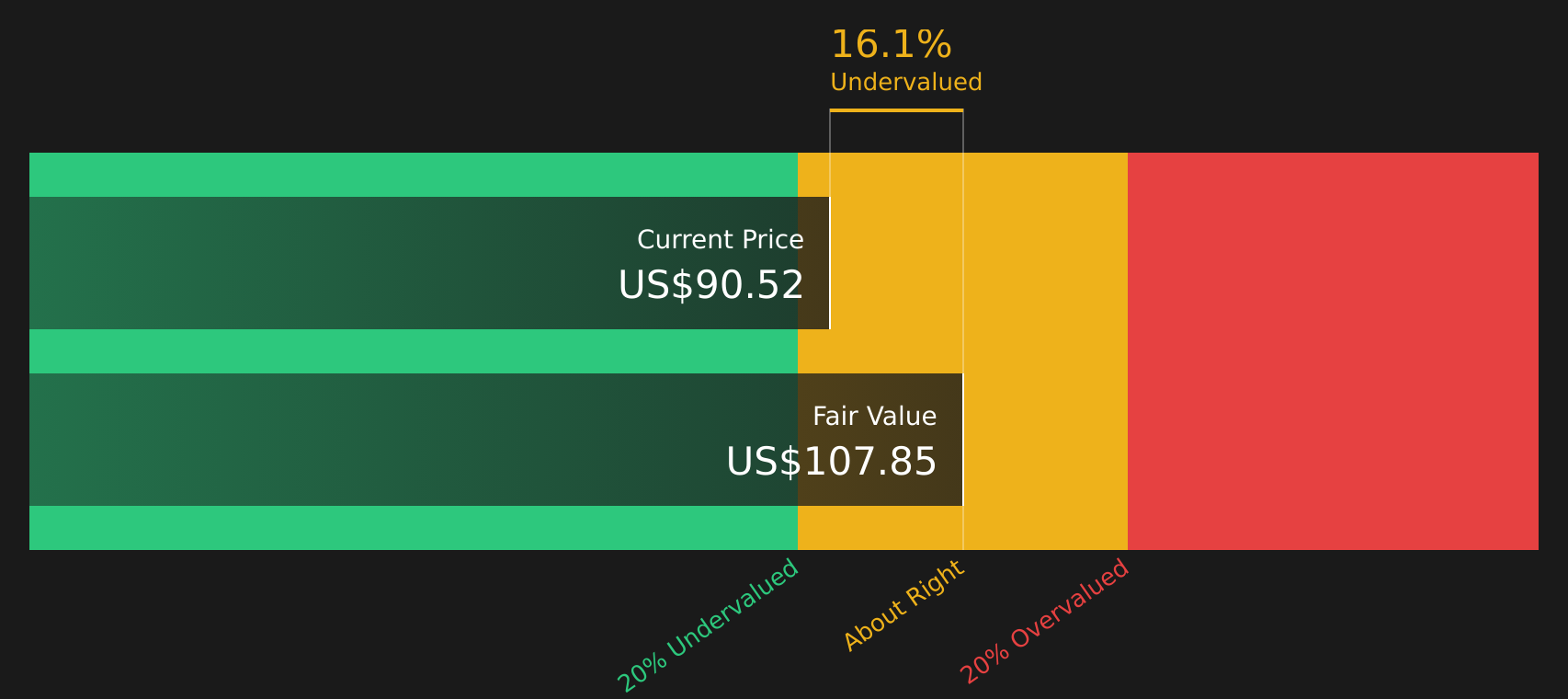

The SWS DCF model presents a different perspective compared to the simple fair value narrative. From this viewpoint, GOLF at $90 sits below an estimated future cash flow value of $107.85, which suggests undervaluation despite a P/E of 30.9x. Which signal do you put more weight on?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals on value, risk, and reward, it makes sense to review the full picture yourself and decide quickly where you stand on GOLF, starting with 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If GOLF has sharpened your interest, do not stop here. Use the Simply Wall Street Screener to hunt for other stocks that could suit your goals.

- Target quality at a discount by scanning 48 high quality undervalued stocks that combine strong fundamentals with prices that may not fully reflect their strengths.

- Strengthen your income stream by reviewing 10 dividend fortresses built around higher yielding companies that still prioritize resilience.

- Focus on resilience first by checking 63 resilient stocks with low risk scores featuring stocks with lower risk scores that can help steady a portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com