Acadia Healthcare Company (ACHC) is back in focus after a strong first quarter, with Raymond James upgrading the stock and the company modestly lifting its 2026 earnings and EBITDA guidance.

See our latest analysis for Acadia Healthcare Company.

Despite a 2.9% decline in the 1 day share price return to US$24.48, Acadia’s strong first quarter update and higher 2026 guidance sit alongside a 71.31% year to date share price return and a weaker 3 year total shareholder return. This suggests recent momentum is rebuilding after a tougher few years.

If this kind of recovery story has your attention, it can be worth seeing what else is moving in healthcare, including 39 healthcare AI stocks

With the stock up 71.31% year to date, yet trading below analyst price targets and carrying a high intrinsic discount, you have to ask: Is Acadia still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 105% Overvalued

According to the most followed narrative, Acadia Healthcare's fair value sits at $11.94, well below the last close of $24.48. This creates a wide valuation gap for investors to assess.

Behavioral health has long been one of the most under-resourced areas of the U.S. healthcare system. That is changing, slowly, unevenly, but decisively. Acadia Healthcare (NASDAQ: ACHC), one of the largest pure-play behavioral health operators, sits at the center of that shift.

The narrative leans heavily on behavioral health moving from the sidelines to the core of care. It ties Acadia's scale, non cyclical demand, and integrated treatment model into one valuation story. It also raises questions about which revenue and margin assumptions sit underneath that fair value and how they align with an unprofitable starting point and future profit forecasts.

Result: Fair Value of $11.94 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this narrative could be tested if operational execution weakens, with Acadia already reporting an annual net income loss of US$1,107.041m and a three-year decline in shareholder returns.

Find out about the key risks to this Acadia Healthcare Company narrative.

Another View: Cash Flows Tell a Very Different Story

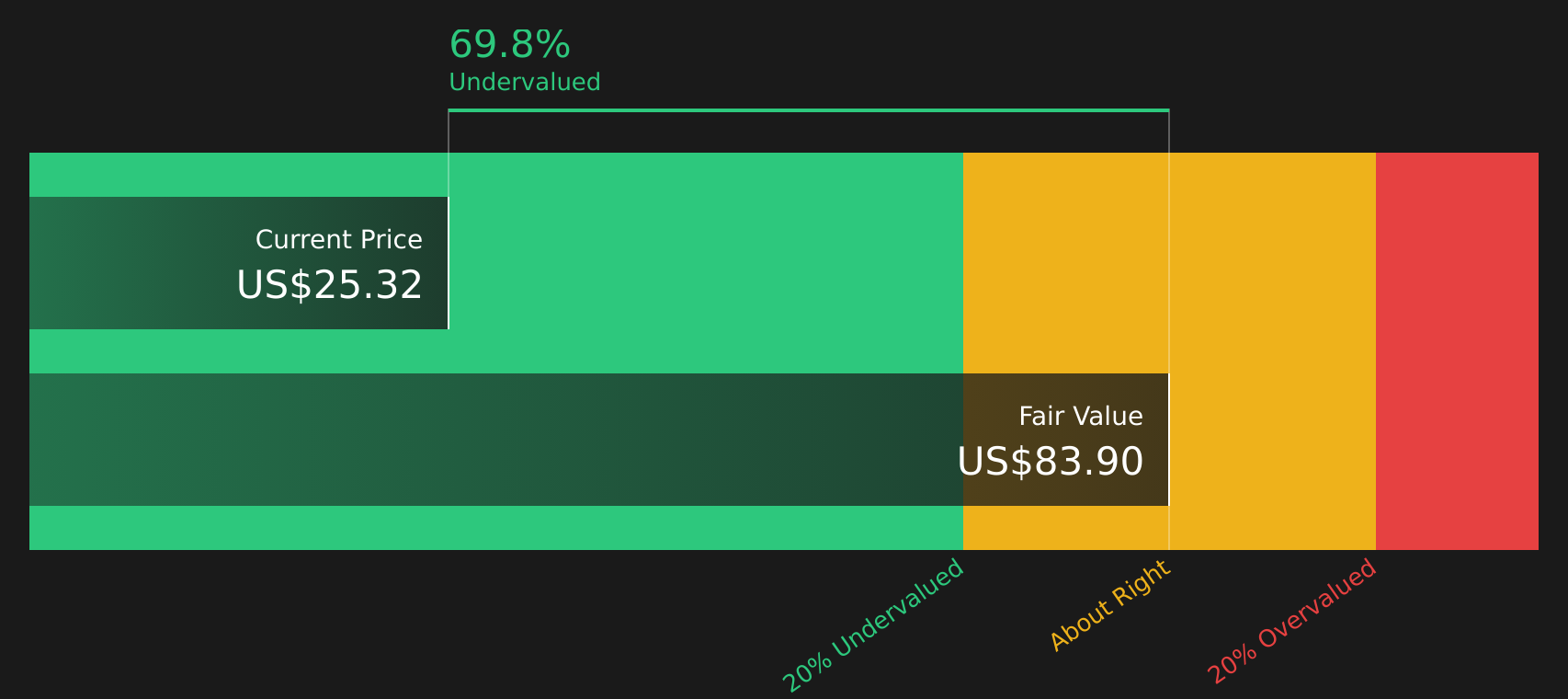

While the popular narrative points to Acadia Healthcare being 105% overvalued at a fair value of $11.94, our DCF model presents a different perspective, with an estimated future cash flow value of $83.90 and the stock trading at a 70.8% discount. Which story do you trust more, sentiment or cash flows?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment clearly split between overvaluation concerns and a bullish cash flow view, it makes sense to move quickly. Review the numbers yourself and weigh both the risks and potential upsides captured in 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

Do not stop with a single stock story. Widen your watchlist with focused ideas that could sharpen your portfolio decisions and highlight opportunities you might otherwise miss.

- Target potential mispricing by scanning 49 high quality undervalued stocks that pair strong fundamentals with prices that may not fully reflect their underlying business strength.

- Strengthen your income playbook by reviewing 9 dividend fortresses that aim for yields of 5% or more with a focus on resilience.

- Prioritize capital preservation by checking 61 resilient stocks with low risk scores that aim for lower risk scores while still offering room for return potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com