- Recently, Polaris reported first-quarter earnings per share of US$0.13 and revenue that both exceeded market forecasts, and also declared a quarterly dividend payable in June 2026.

- These stronger-than-expected results, coupled with the dividend announcement, highlight management’s confidence in the company’s operational footing despite recent market volatility.

- Next, we’ll examine how Polaris’ earnings beat and dividend declaration may influence its existing investment narrative and risk-reward balance.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Polaris Investment Narrative Recap

To own Polaris, you need to believe its powersports brands and product pipeline can support a sustained recovery in earnings, even through industry and economic swings. The latest earnings beat and dividend declaration support that view but do not materially change the near term swing factor, which is how well Polaris manages tariffs and softer demand, or the key risk that prolonged weakness in retail powersports spending and higher rates continue to weigh on volumes.

The most relevant recent announcement here is the Board’s decision to maintain a quarterly dividend of US$0.68 per share, payable in June 2026. Paired with the Q1 revenue and EPS beat, it reinforces the idea that management is comfortable returning cash to shareholders while still absorbing tariff costs and uneven retail demand, which sits right at the heart of the current risk reward debate.

Yet, even with these positives, the ongoing uncertainty around tariff costs and their impact on margins is something investors should be aware of...

Read the full narrative on Polaris (it's free!)

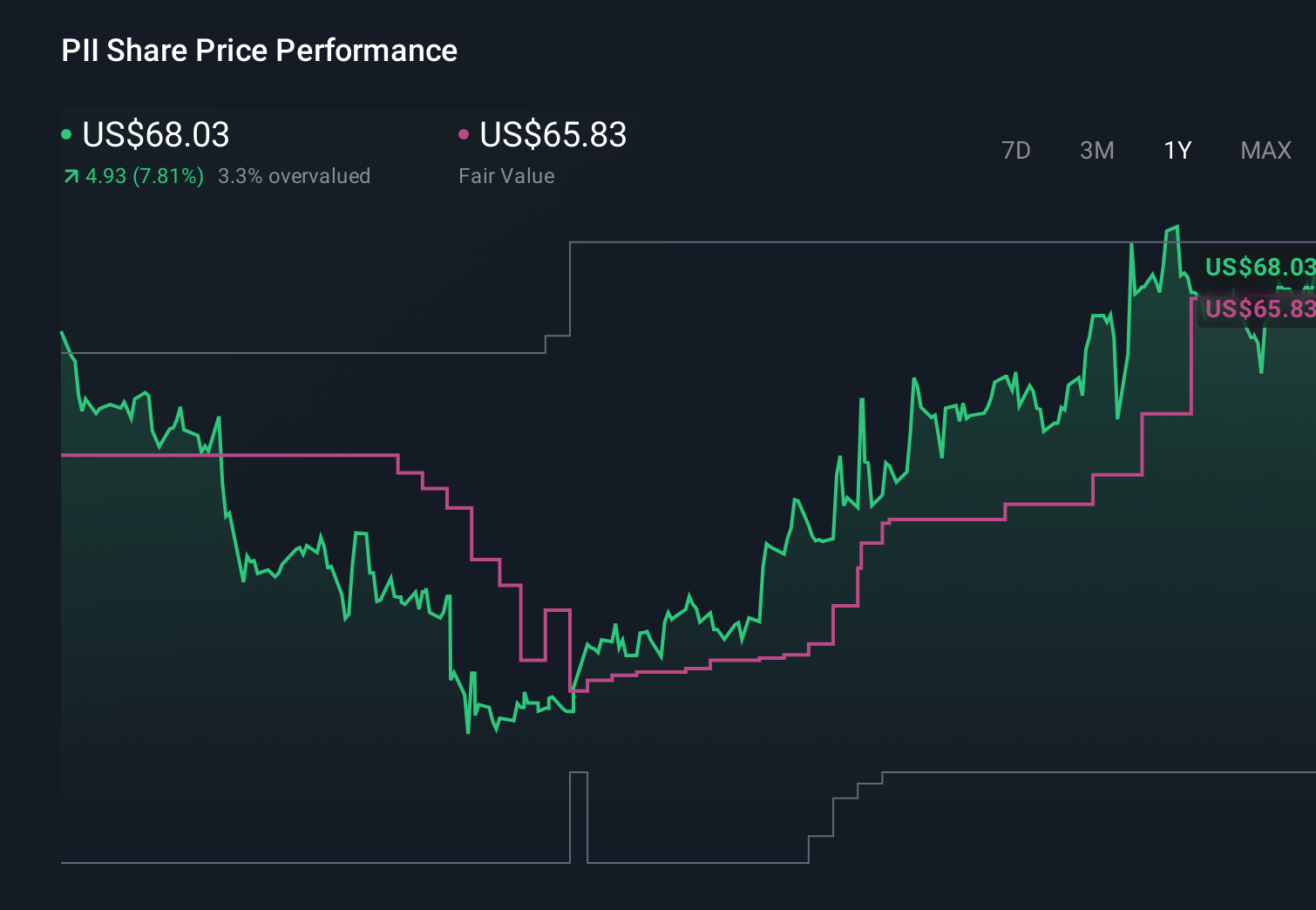

Polaris' narrative projects $7.8 billion revenue and $425.0 million earnings by 2029. This requires 2.1% yearly revenue growth and an earnings increase of about $871 million from -$446.1 million today.

Uncover how Polaris' forecasts yield a $68.00 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Before this Q1 surprise, the most optimistic analysts were modeling revenues near US$8.0 billion and earnings of US$376.3 million by 2028, a far more upbeat view than consensus, and this earnings beat plus dividend continuity may prompt you to reconsider whether that bullish tariff relief and margin recovery story still feels too aggressive or perhaps closer to achievable.

Explore 3 other fair value estimates on Polaris - why the stock might be worth as much as 23% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com