Mastercard (MA) has turned more attention to digital asset rails, expanding its settlement system to support on-chain, real-time payments using regulated stablecoins across multiple blockchains, alongside new collaborations in open banking and account-to-account payments.

See our latest analysis for Mastercard.

Despite the news around stablecoin settlement and new account to account partnerships, Mastercard’s recent share price momentum has been weak, with the stock down about 16% year to date and its 1 year total shareholder return down about 19%, while the 3 year and 5 year total shareholder returns remain positive.

If you are interested in how payment and crypto themes are reshaping listed opportunities, it can be useful to scan beyond Mastercard and review 20 cryptocurrency and blockchain stocks

With Mastercard stock down this year but still carrying a US$471.55 price tag, along with analyst targets and intrinsic value estimates that sit higher, investors may be wondering whether this is a reset that offers a potential opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 20.8% Undervalued

The most followed valuation narrative for Mastercard places fair value at about $595, compared with the last close of $471.55, framing the recent share price pullback against a higher intrinsic value estimate.

📈Mastercard has a wide moat displayed in its stellar operating margin. It also shows solid revenue and EPS growth along with a return on its capital 7-8 times more than its estimated cost of capital.

Curious what has to happen for that valuation to make sense? The narrative leans on strong margins, steady revenue expansion, and compounding earnings power. The detailed assumptions are where it gets interesting.

Result: Fair Value of $595.22 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on assumptions around margins and growth staying resilient. Any pressure on profitability or a reset in valuation multiples could quickly challenge that view.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle On Valuation

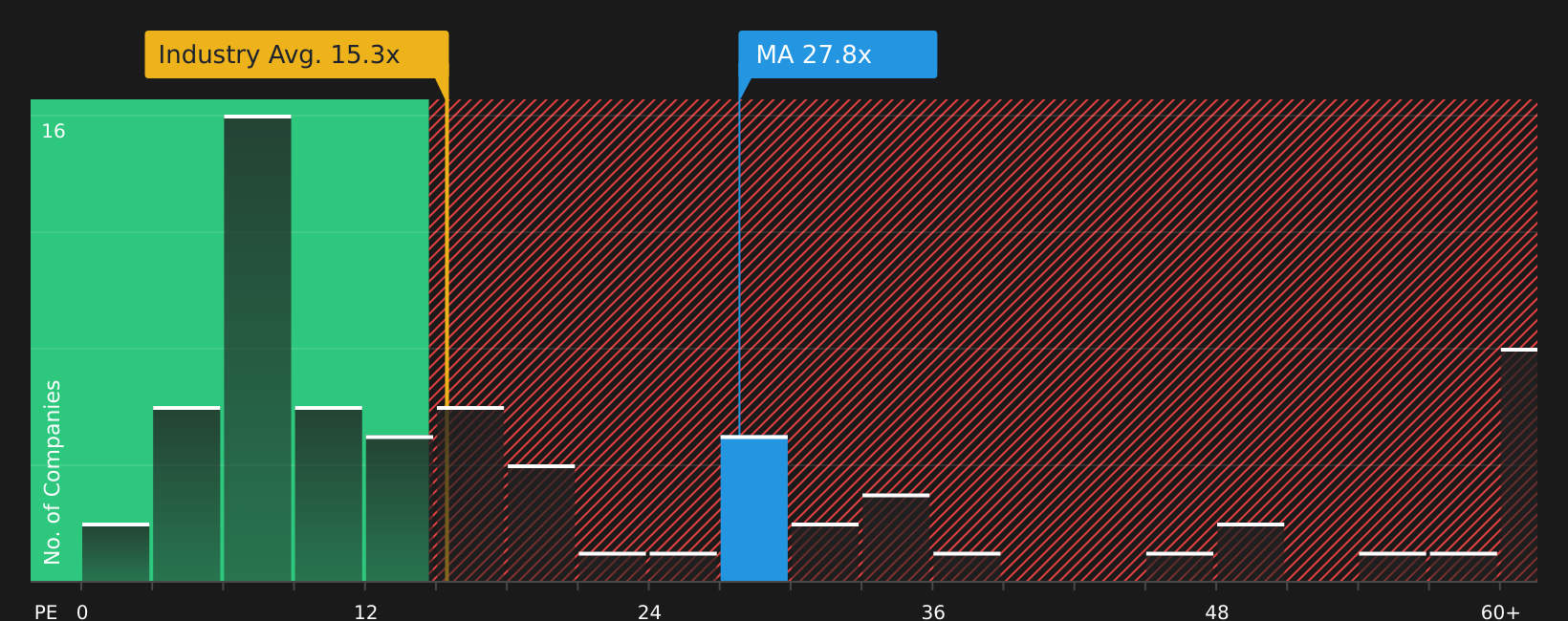

The user narrative leans heavily on discounted cash flows and historical averages to argue Mastercard looks undervalued around $471.55, with a fair value near $595. Yet on a simple P/E basis of 26.8x, the stock looks expensive versus peers at 23.7x and an estimated fair ratio of 20.7x. This raises the question of how much optimism is already in the price.

For investors who pay close attention to earnings multiples and how they compare across a sector, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The mixed signals on valuation and fundamentals make this a good moment to look past headlines and review the underlying data directly. To weigh potential upside against possible downside in more detail, take a closer look at the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Mastercard has your attention, do not stop there. Broaden your watchlist now so you are not the one hearing about tomorrow's winners after they move.

- Target resilience first by scanning 63 resilient stocks with low risk scores, which may help steady your portfolio when markets turn noisy.

- Spot potential value upsides early by reviewing 47 high quality undervalued stocks, which combine quality fundamentals with discounted prices.

- Strengthen your core holdings by focusing on solid balance sheet and fundamentals stocks screener (47 results), which prioritise financial stability and disciplined capital use.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com