FedEx stock snapshot and recent performance context

FedEx (FDX) stock has moved lower recently, with the price down 1.4% over the past day, 21.2% over the past week, 9.3% over the past month, and 13.1% over the past 3 months.

See our latest analysis for FedEx.

The recent pullback in FedEx’s share price contrasts with its stronger year to date share price return of 10.69%, while the 1 year total shareholder return of 88.17% points to earlier optimism that is now cooling as momentum fades.

If FedEx’s recent swings have you reassessing your options, this could be a good moment to broaden your search and check out 20 top founder-led companies

With FedEx shares pulling back after strong longer term returns, the key question for you is whether the current valuation reflects all the recent progress in revenue and net income, or if the market is overlooking a potential opportunity.

Most Popular Narrative: 19.3% Undervalued

FedEx's most followed narrative places fair value at about $401.89 per share compared with the latest close of $324.46. This frames a sizable valuation gap built on detailed cash flow and earnings assumptions using an 8.63% discount rate.

The Network 2.0 project aims to optimize 50 U.S. stations, streamlining operations to improve efficiency. By enabling about 12% of FedEx's daily global volume to flow through optimized facilities by the end of FY '25, this initiative should positively impact operating margins and earnings.

Curious what kind of revenue path and margin profile have to sit behind a fair value near $400, and what future earnings multiple ties it all together.

Result: Fair Value of $401.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on FedEx managing contract changes and tariff disputes. Any stumble in its freight separation or cost cuts could quickly challenge the current valuation story.

Find out about the key risks to this FedEx narrative.

Another way to look at FedEx’s valuation

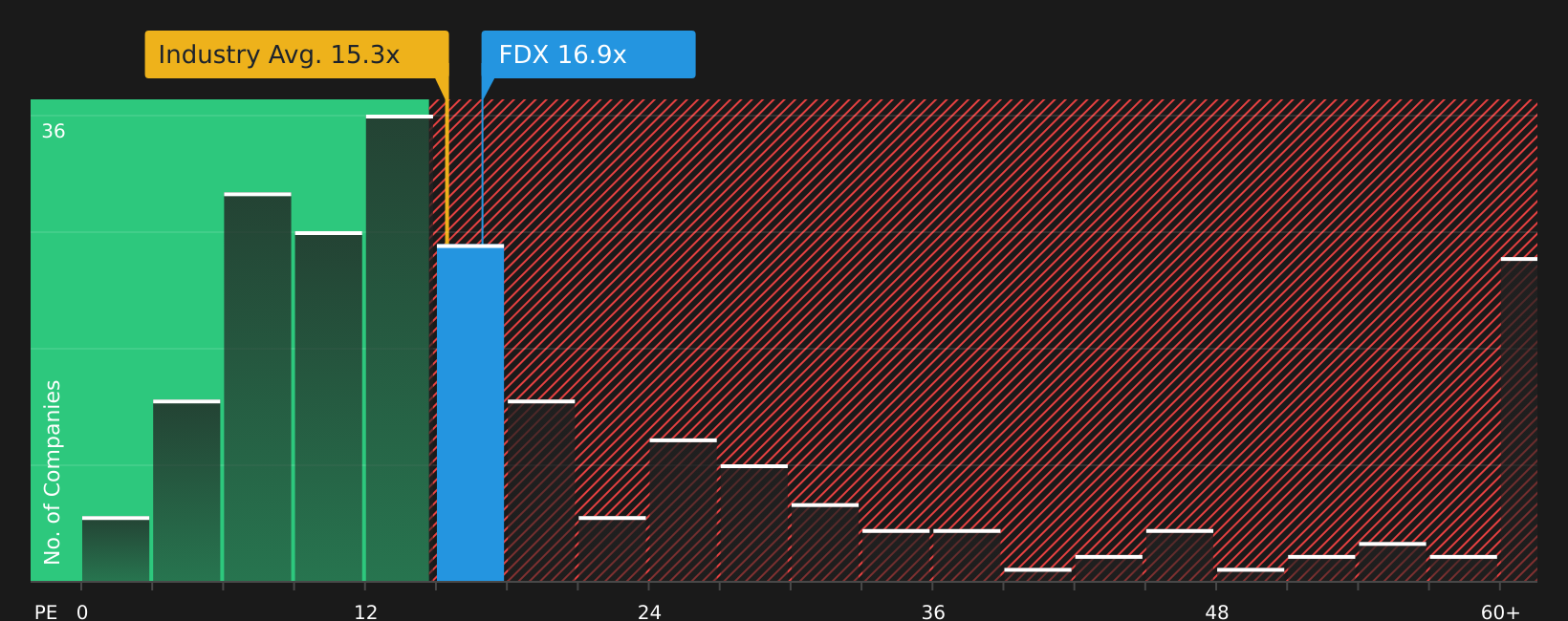

The first narrative leans on cash flows and earnings forecasts, but the current market price also reflects how investors are using earnings multiples. FedEx trades on a P/E of 17.3x compared with 15x for the global Logistics industry and 22.6x for its peer group, while the fair ratio sits higher at 23.5x. That mix of “cheaper than peers” yet “richer than the sector” leaves you weighing whether the market closes the gap toward the fair ratio, or cuts the premium versus the wider industry instead.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly mixed in the article so far, use this as a prompt to move quickly, review the evidence yourself and weigh both the optimism and concern behind FedEx’s 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If FedEx has sharpened your focus, do not stop here. Use this momentum to scan fresh opportunities that fit your goals before the market moves on.

- Target potential mispricings by reviewing companies highlighted in the 47 high quality undervalued stocks to see which stocks currently trade below their assessed worth.

- Protect your downside by checking out the 63 resilient stocks with low risk scores and focus on businesses with more resilient profiles and lower overall risk scores.

- Get ahead of the crowd by scanning the screener containing 22 high quality undiscovered gems and zero in on quality stocks that fewer investors are watching.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com