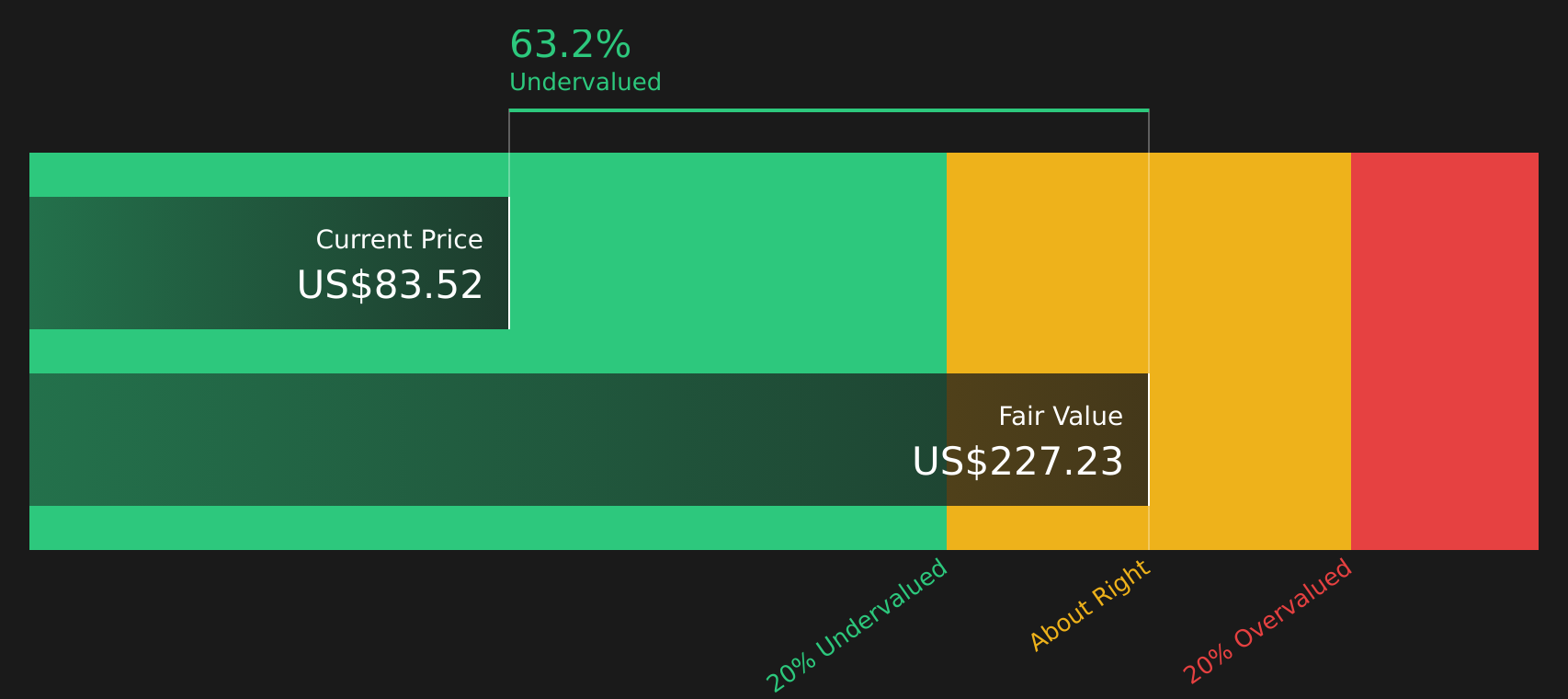

- Investors may be wondering if Delta Air Lines at around US$78.78 is still offering value after a strong run, or if most of the opportunity is already priced in.

- The stock has pulled back around 3.7% over the last week, but is still up about 15.0% over the past month, 14.1% year to date and 62.8% over the last year, with a 113.0% return over three years and 75.0% over five years.

- Recent headlines have focused on Delta's role as a major U.S. carrier, ongoing capacity and route decisions, and broader industry themes such as travel demand and operational reliability. Together, these news items help frame how investors are weighing both opportunity and risk around the stock.

- Even after these moves, Delta holds a valuation score of 4/6. This sets up a closer look at how different valuation methods are pricing the stock today and hints at an even richer way of thinking about value later in this article.

Approach 1: Delta Air Lines Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth today by projecting the cash the company may generate in the future and discounting those amounts back to the present.

For Delta Air Lines, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $3.09b. Analyst and extrapolated projections suggest free cash flow figures between 2026 and 2035 in the range of roughly $2.36b to $4.93b, with 2035 estimated at $4.93b and discounted back to $2.12b in today’s terms.

Pulling all those discounted cash flows together gives an estimated intrinsic value of $106.10 per share. Compared with the recent share price of about $78.78, the model implies a 25.7% discount, which indicates the stock is trading below this estimate of fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Delta Air Lines is undervalued by 25.7%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Delta Air Lines Price vs Earnings

For a profitable company, the P/E ratio is a useful yardstick because it ties the share price directly to the earnings that support it. Investors typically look for a P/E that reflects both what the business earns today and how reliable and sustainable those earnings might be.

A higher P/E often goes hand in hand with stronger growth expectations or lower perceived risk, while a lower P/E can reflect more muted growth expectations or higher uncertainty. With Delta Air Lines trading on a P/E of about 11.5x, the stock sits above the Airlines industry average of around 8.8x, but below a broader peer group average of about 21.5x.

Simply Wall St’s Fair Ratio framework estimates a P/E of roughly 19.0x for Delta Air Lines, based on factors such as earnings growth characteristics, industry, profit margins, company size and risk profile. This Fair Ratio can give a more tailored reference point than a simple comparison with industry or peers, because it is designed to adjust for those company specific features. Against this yardstick, Delta Air Lines’ current P/E of 11.5x is below the Fair Ratio of 19.0x, which indicates that the stock is trading at a discount on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Delta Air Lines Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple way for you to attach a clear story about Delta Air Lines to the numbers. This links what you believe about its routes, premium demand, balance sheet risk or tariffs to a concrete forecast for revenue, earnings, margins and ultimately a Fair Value that can be compared with today’s share price to help decide whether to act or wait.

On Simply Wall St’s Community page, Narratives are available as an easy tool that many investors already use. They update automatically when new information like earnings, guidance changes or news on fuel costs or travel demand is added, so your Fair Value view stays aligned with the latest data rather than a static spreadsheet.

Looking at existing Narratives for Delta Air Lines, one cautious perspective ties together concerns about waning travel demand, thin margins and tariff risks into a Fair Value around US$49 per share. A more optimistic view focuses on premium and international strength, partnerships and earnings resilience to arrive at a higher Fair Value near US$95. Your own narrative can sit anywhere along that spectrum depending on how you see the company’s story playing out in the numbers.

For Delta Air Lines, however, we’ll make it really easy for you with previews of two leading Delta Air Lines Narratives:

Fair value in this bullish narrative is set at about US$81.81 per share.

At the recent price of US$78.78, this view sees the stock trading at roughly a 3.7% discount to that fair value.

Revenue growth is modelled at around 3.9% a year.

- Premium, loyalty and international revenue are central, with flat capacity intended to support margins and free cash flow.

- Analysts in this camp expect earnings to reach about US$5.3b by June 2029 and apply a P/E of roughly 13.2x to those earnings.

- The consensus fair value of about US$81.81 sits close to the recent share price, so this view treats Delta as broadly fairly priced on current assumptions.

Fair value in this more cautious narrative is set at about US$63.21 per share.

At the recent price of US$78.78, this view sees the stock trading around 24.5% above that fair value.

Revenue growth is set at roughly 3.5% a year.

- This author highlights strong unit economics, with revenue per seat mile running ahead of cost per seat mile, but questions how much of that strength is already reflected in the share price.

- Concerns focus on a stretched balance sheet, thin margins and the potential impact of external shocks such as tariffs or weaker economic conditions on high value routes.

- The conclusion is that a fair value near US$63 leaves limited room for further valuation expansion from current levels.

If you want to see how your own view lines up with these, you can use the community narratives on Simply Wall St as a starting point. You can then adjust the assumptions to match what you think is realistic for Delta’s earnings, margins and balance sheet risk.

See what the community is saying about Delta Air Lines

Do you think there's more to the story for Delta Air Lines? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com