- Walker & Dunlop, Inc. recently arranged a US$101,561,900 HUD Section 223(f) refinancing loan for Enclave Heritage Flats, a 312-unit multifamily community in Chula Vista, California, on behalf of The Baldwin Company.

- This HUD-backed refinancing, which replaces bridge financing Walker & Dunlop helped secure in 2024, highlights the firm’s ability to convert shorter-term capital solutions into longer-term agency debt within a growing Southern California multifamily market.

- Next, we’ll examine how arranging this large HUD-backed multifamily refinancing influences Walker & Dunlop’s investment narrative around capital markets execution.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 32 best rare earth metal stocks of the very few that mine this essential strategic resource.

Walker & Dunlop Investment Narrative Recap

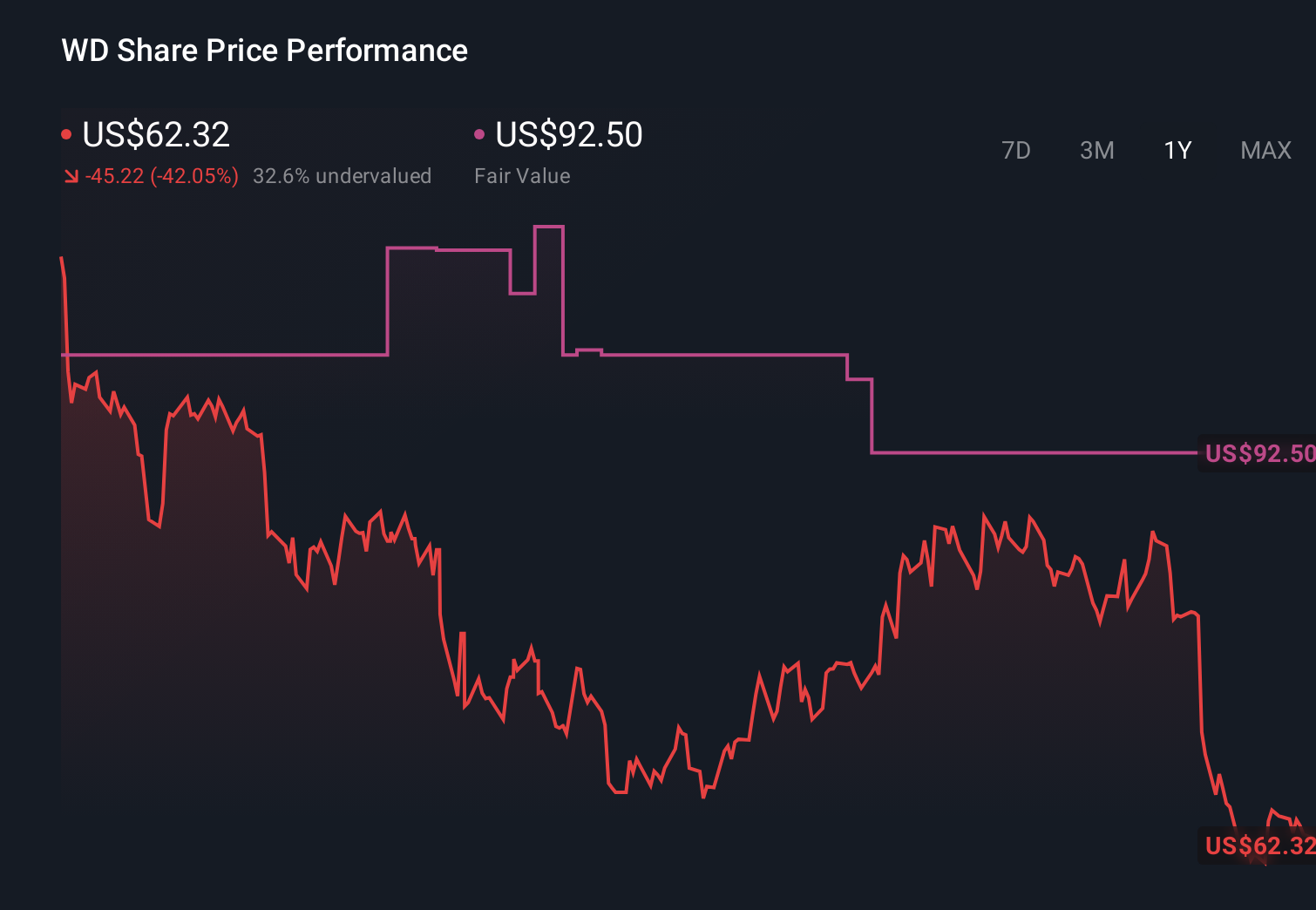

To own Walker & Dunlop, you need to believe in its role as a key intermediary in U.S. commercial real estate finance, especially multifamily and agency-backed lending. The Enclave Heritage Flats refinancing underscores execution in HUD and affordable housing, but does not materially change the near term picture where interest rate volatility and dependence on government backed programs remain the central catalyst and risk for earnings and origination volumes.

The most directly relevant recent announcement is Walker & Dunlop’s Q1 2026 earnings, which showed higher revenue and net income year over year. Transactions like the Enclave Heritage Flats HUD refinancing help illustrate how the existing capital markets and affordable housing platforms feed into those results, and why future fee income and servicing revenue still depend heavily on sustained agency lending activity and broader credit conditions.

Yet investors should also weigh how reliant Walker & Dunlop remains on government backed lending programs and what that means if agency limits or regulations shift...

Read the full narrative on Walker & Dunlop (it's free!)

Walker & Dunlop's narrative projects $1.7 billion revenue and $214.2 million earnings by 2029. This requires 12.2% yearly revenue growth and about a $145.9 million earnings increase from $68.3 million today.

Uncover how Walker & Dunlop's forecasts yield a $68.67 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value views for Walker & Dunlop span roughly US$30.94 to US$68.67, underscoring wide disagreement on worth. As you weigh these opinions, consider how interest rate volatility and its impact on refinancing volumes could influence the company’s ability to convert transactions like recent HUD deals into consistent earnings, and why reviewing several perspectives may help you frame that risk more clearly.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth 36% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com