DuPont de Nemours (DD) reaffirmed its earnings and net sales guidance for the second quarter and full year 2026, while also securing shareholder approval to enable a reverse stock split and a corresponding reduction in authorized shares.

See our latest analysis for DuPont de Nemours.

At a share price of $48.66, the stock has a 1 day share price return of 2.25%, with a 30 day share price return of 5.23% and a year to date share price return of 19.06%. The 1 year total shareholder return of 75.71% and 3 year total shareholder return of 73.60% point to momentum that recent guidance and the planned reverse stock split could be helping to sustain.

If this kind of capital structure reset has you thinking more broadly about where to put fresh money to work, you can also scan the market using our 20 top founder-led companies

With DuPont de Nemours trading at $48.66 and reportedly at a discount to both analyst price targets and intrinsic value estimates, the key question is simple: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 13.3% Undervalued

Against a last close of $48.66, the most followed narrative pegs DuPont de Nemours' fair value at $56.13, setting up a valuation gap investors will want to understand.

The company's renewed portfolio focus post Qnity spin and recent divestitures in non core segments enables greater resource allocation to high growth specialty businesses, contributing to improved operating margin and increased earnings stability. DuPont's robust innovation pipeline, including content and share gains in advanced nodes and the water tech portfolio, underpins premium pricing opportunities and sustainably enhances gross margins over the medium to long term.

Want the full story behind that valuation gap? This narrative leans heavily on rising earnings, fatter margins, and a richer future earnings multiple to justify that fair value. Result: Fair Value of $56.13 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside story still leans on PFAS legal risks staying contained and portfolio changes like the Qnity separation not leaving earnings more volatile.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

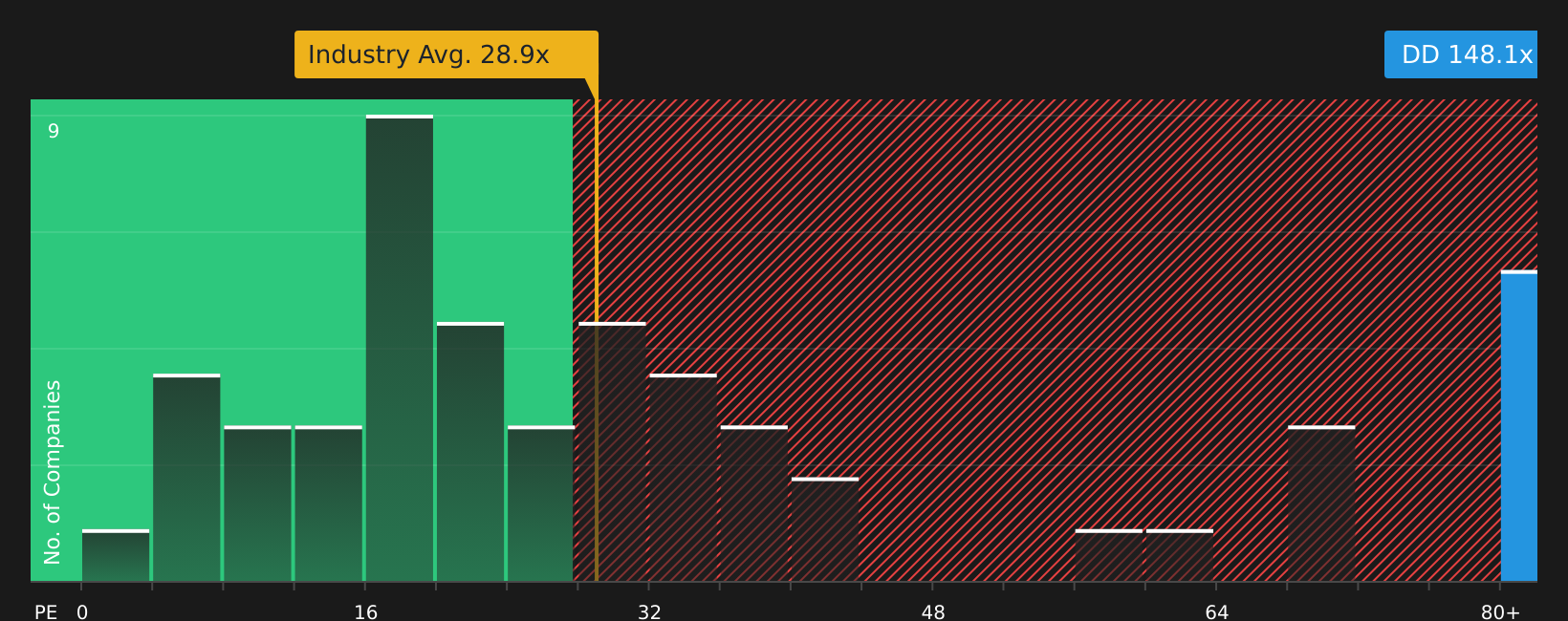

Another Angle: High P/E Keeps The Debate Alive

The SWS model flags DuPont de Nemours as trading at a very high P/E of 149.3x, while its fair ratio is 31.1x, the US Chemicals industry sits at 26.4x, and peers average 35.2x. That kind of gap could mean opportunity or simply extra valuation risk. Which side do you think it reflects?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With bulls and bears both finding support in the data, it makes sense to move quickly, review the numbers for yourself, and weigh both the upside and the risks by checking out these 3 key rewards and 2 important warning signs

Ready for more investment ideas?

If you stop here, you could miss stocks that better fit your goals, so take a few minutes to scan for opportunities that line up with your strategy.

- Target resilience by focusing on companies that score well on financial strength with the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for value by checking out companies that look mispriced on quality and fundamentals using the 46 high quality undervalued stocks.

- Spot potential standouts early by scanning the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com