Several bullish analyst updates and strong recent earnings have put F5 (FFIV) in focus as investors weigh how hybrid multicloud demand, cybersecurity spending, and growing AI workloads might shape the stock ahead of the upcoming investor day.

See our latest analysis for F5.

The recent analyst optimism and earnings beat sit alongside a strong run in the stock, with a 26.6% 1 month share price return helping lift the year to date share price return to 59.4%. The 3 year total shareholder return of 181.8% points to momentum that has been in place for some time.

If the AI angle of F5's story has caught your attention, this could be a useful moment to widen your search using our screener for 62 profitable AI stocks that aren't just burning cash

With F5 now trading close to analyst targets and some valuation models flagging the stock as expensive, the key question is simple: is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 21.3% Overvalued

The most followed narrative pegs F5's fair value at $337.40, which sits below the last close of $409.13 and frames the current debate around how much optimism is already in the price.

Accelerated enterprise adoption of hybrid multi-cloud architectures and data center modernization is fueling durable demand for F5's application delivery and security solutions, positioning the company for sustained product and software revenue growth over the next several years.

Curious what kind of revenue mix, margin profile, and future earnings multiple need to line up to support that fair value estimate and still point to a premium valuation story.

Result: Fair Value of $337.40 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

Still, heavy reliance on enterprise and telecom budgets, along with intense competition from hyperscalers and security peers, could pressure F5's growth profile and investor confidence in this premium story.

Find out about the key risks to this F5 narrative.

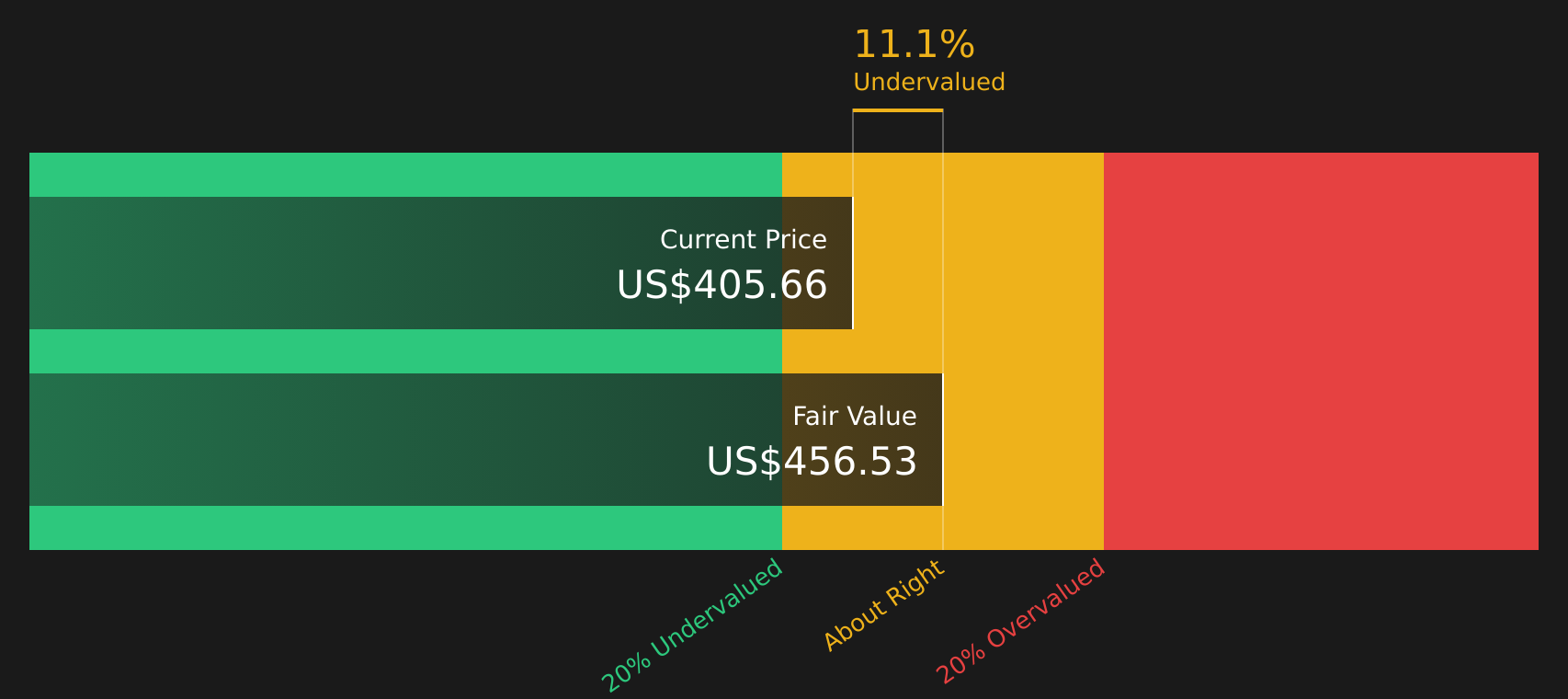

Another View: Cash Flows Paint a Different Picture

The narrative fair value of $337.40 points to F5 being 21.3% overvalued, but our DCF model lands in a different place, with a future cash flow value of $457.19 per share. On that basis, F5 at $409.13 screens as undervalued, which raises a simple question: which lens do you trust more, earnings multiples or cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out F5 for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment running high, this is a good time to review the numbers yourself and decide where you stand. To help frame both sides of the story, take a closer look at the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If F5 has sharpened your focus, do not stop here, some of the most compelling opportunities come from looking broadly across sectors, sizes, and styles.

- Target potential mispricing by scanning for quality companies trading below what their fundamentals may justify using the 47 high quality undervalued stocks.

- Strengthen the income side of your portfolio by zeroing in on stocks that offer reliable 5%+ yields with the 11 dividend fortresses.

- Dial down portfolio risk by focusing on companies with resilient finances through the 63 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com