- On May 29, 2026, activist investor Voss Capital urged Sempra to spin off its Texas-based Oncor electricity business, arguing that a standalone Oncor, serving more than 4 million customers over 144,000 miles of lines, could be worth up to US$78.00 billion by the end of 2028 and simplify Sempra’s structure.

- Voss Capital’s proposal highlights how separating Oncor from Sempra’s California utilities and Sempra Infrastructure could clarify each unit’s risk profile, especially by isolating Oncor’s Texas-focused growth from California wildfire exposure that has weighed on utility valuations.

- We’ll now consider how this push to separate Oncor, and the potential simplification of Sempra’s business mix, may reshape its investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Sempra Investment Narrative Recap

To own Sempra, you need to be comfortable with a complex, largely regulated utility that is balancing California risk with Texas and LNG exposure. The Voss Capital push to spin off Oncor could influence how investors view Sempra’s structure, but until management responds, the most immediate catalyst remains the company’s earnings and guidance, while wildfire and regulatory risk in California still looks like the key overhang.

Among recent announcements, Sempra’s May 15, 2026 follow on equity offering of about US$416 million, with capacity for up to US$2.584 billion more, stands out in this context. How Sempra finances its capital plan, particularly if any portfolio changes follow from the Oncor discussion, may shape both its earnings trajectory and balance sheet flexibility.

Yet investors should be aware that California wildfire and policy risk could still materially affect...

Read the full narrative on Sempra (it's free!)

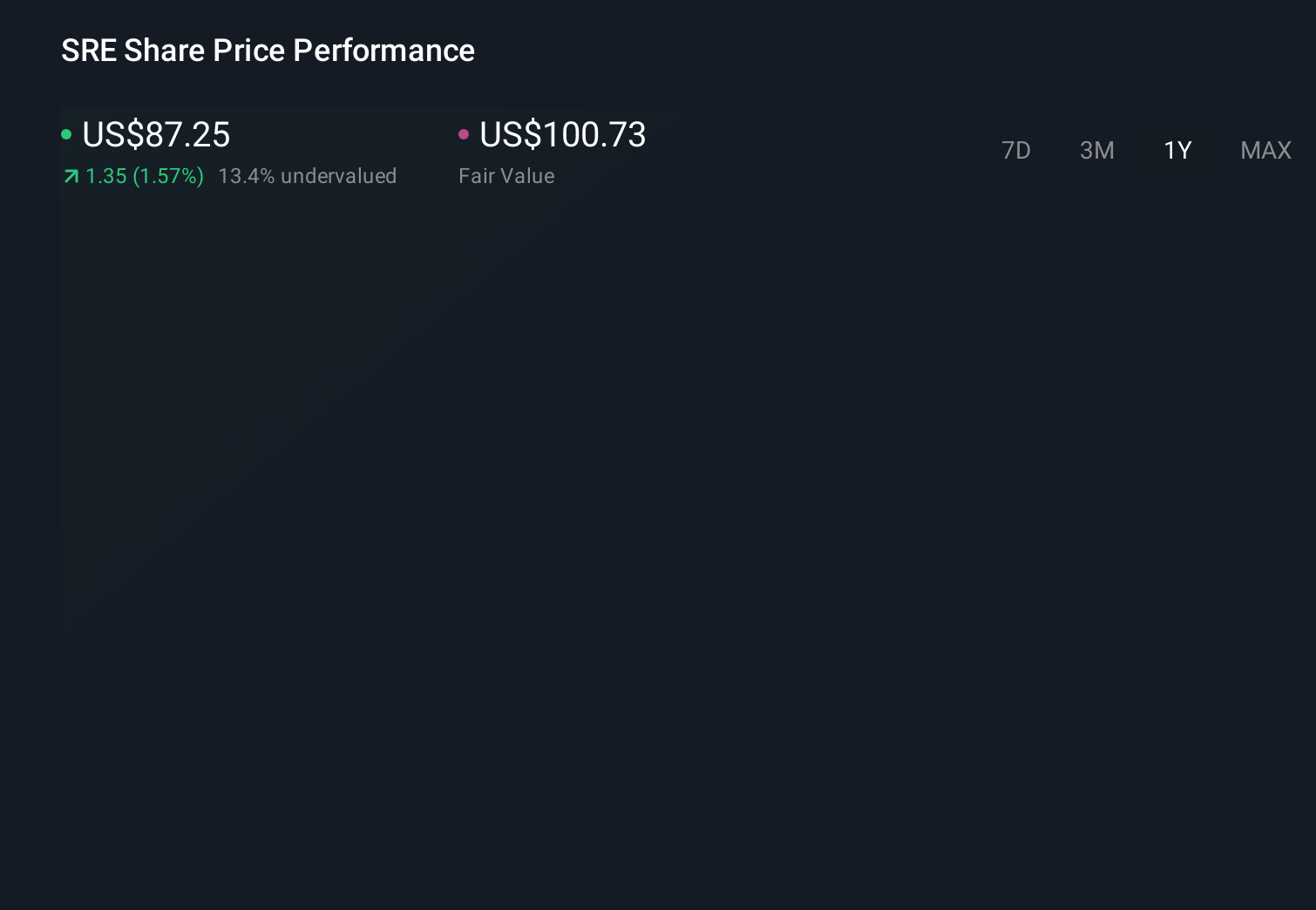

Sempra's narrative projects $14.4 billion revenue and $4.1 billion earnings by 2029.

Uncover how Sempra's forecasts yield a $104.00 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members’ fair value estimates for Sempra span roughly US$51 to US$104 across 2 views, underscoring how far apart individual assessments can be. When you contrast that with concerns about California wildfire and regulatory risk, it underlines why you may want to weigh several different viewpoints before deciding how Sempra fits into your portfolio.

Explore 2 other fair value estimates on Sempra - why the stock might be worth as much as 16% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Sempra research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Sempra research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sempra's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com