Forestar Group (FOR), a residential lot developer and subsidiary of D.R. Horton, is drawing investor interest after recent share gains, with the stock up 0.8% today and 6.9% over the past week.

See our latest analysis for Forestar Group.

Recent gains build on a solid run, with the share price return of 13.9% year to date and a 1 year total shareholder return of 45.03%, suggesting momentum has been positive rather than fading.

If Forestar Group has sharpened your interest in housing related themes, you might also want to check out infrastructure driven opportunities through our 33 power grid technology and infrastructure stocks

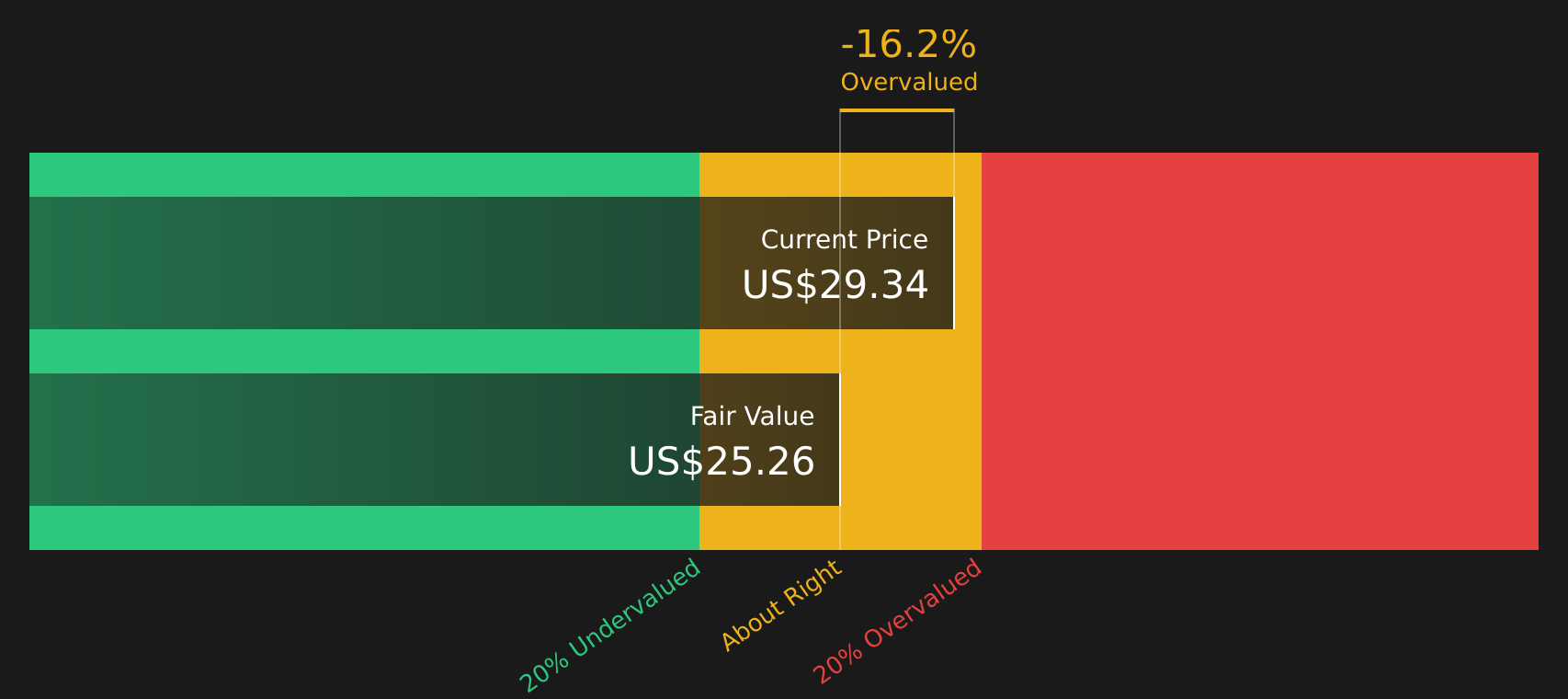

With Forestar Group trading at $27.70 against an analyst price target of $31.33 and a value score of 3, the key question is whether the stock is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 16.1% Undervalued

Forestar Group's most followed narrative pegs fair value at $33, compared with the last close at $27.70, which frames the recent share gains as only part of the story.

Forestar's capital-efficient, disciplined development model, supported by a strong balance sheet and high liquidity, enables the company to manage working capital efficiently, execute selective land acquisition despite tighter credit across the industry, and deliver robust returns on invested capital, driving higher net margins and sustained long-term EPS growth.

Want to see what sits behind that fair value gap? Revenue expectations, margin assumptions and a higher future earnings multiple all feed into this narrative's $33 figure.

Result: Fair Value of $33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the picture can change quickly if Forestar's reliance on D.R. Horton limits lot sales, or if tighter regulations and project delays start to pressure margins.

Find out about the key risks to this Forestar Group narrative.

Another Angle: DCF Points the Other Way

There is a catch. While the narrative-based fair value sits at $33, Simply Wall St's DCF model puts Forestar Group's value at $14.45 per share, which is well below the current $27.70 price and frames the stock as trading rich rather than cheap.

When two methods point in opposite directions like this, it really comes down to which assumptions you find more realistic over the long run.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Forestar Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value, it helps to look past the headlines and compare the underlying drivers yourself, then move quickly if the story changes in your eyes. To balance the risks against what the market already likes, review the company's 2 key rewards

Looking for more investment ideas?

If Forestar has your attention, do not stop here. Broaden your watchlist now so you are not chasing opportunities after everyone else has moved.

- Target quality at a discount by scanning companies that combine strong fundamentals with appealing prices through the 47 high quality undervalued stocks.

- Prioritize resilience by checking stocks that rank well on balance sheet strength and financial footing using the solid balance sheet and fundamentals stocks screener (45 results).

- Spot potential early movers by running a focused search of under-followed companies with solid fundamentals via the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com