- In recent months, Delta Air Lines has pushed further into premium travel, expanding first-class seating, enhancing onboard meals, and rolling out more upscale lounges while leaning on loyalty partnerships to diversify revenue beyond standard economy fares.

- This premium focus has helped Delta generate around 20% more revenue per seat than many U.S. peers, highlighting how upselling higher-margin products can reshape an airline’s earnings mix and competitive position.

- Now we’ll examine how Delta’s emphasis on premium seats and diversified revenue streams could influence its existing investment narrative.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

Delta Air Lines Investment Narrative Recap

To own Delta, you need to believe its premium, loyalty and international focus can offset softer main cabin demand and support earnings, even with high debt and a new, relatively untested management team. The recent news about premium upselling reinforces the near term catalyst around higher margin revenue, but it does not materially change the key risk that a weaker economy could hit domestic and corporate travel.

Among recent announcements, the 10 year MRO agreement with UPS stands out alongside the premium push. While premium cabins and lounges target higher per seat revenue, the UPS contract supports a different catalyst: diversifying income beyond passenger tickets. Together, they frame Delta as a business increasingly tied to premium customers and third party services, rather than relying mainly on U.S. main cabin volume for growth.

Yet behind the premium story, investors should also be aware of the risk that...

Read the full narrative on Delta Air Lines (it's free!)

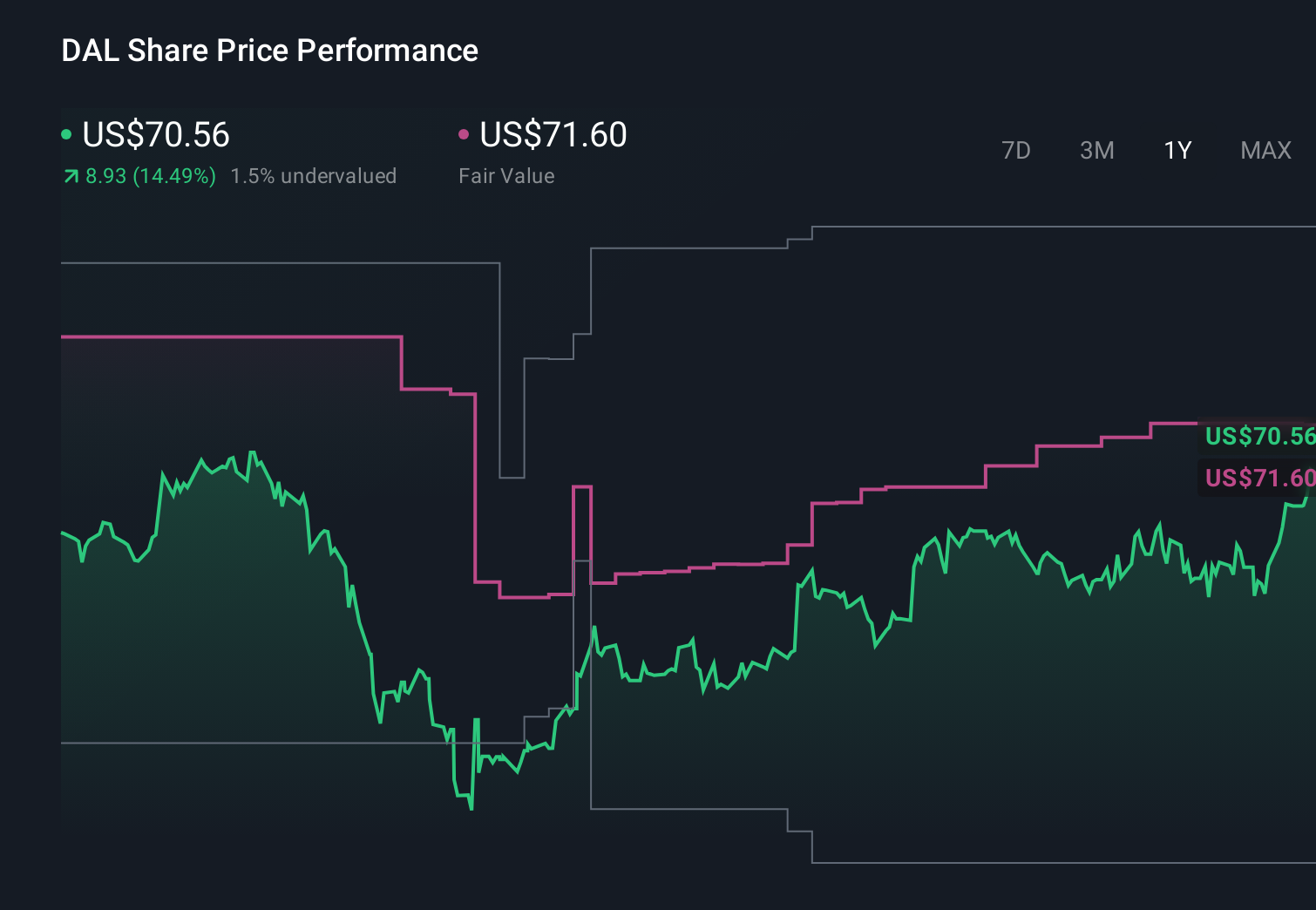

Delta Air Lines' narrative projects $72.9 billion revenue and $5.5 billion earnings by 2029. This requires 4.8% yearly revenue growth and an earnings increase of about $0.5 billion from $5.0 billion today.

Uncover how Delta Air Lines' forecasts yield a $79.89 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Delta could reach about US$82.1 billion in revenue and US$6.0 billion in earnings, which is far more upbeat than consensus. The latest premium focused news could either support that stronger view or prompt revisions, so it is worth weighing that optimism against the alternate risk that main cabin softness and macro uncertainty still...

Explore 9 other fair value estimates on Delta Air Lines - why the stock might be worth 36% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Delta Air Lines research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

No Opportunity In Delta Air Lines?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com