- Earlier in May 2026, Univar Solutions B.V. expanded its long-standing partnership with Dow to distribute Dow’s silicone additives for plastics and composites across EMEA, while Dow and X-energy received a Finding of No Significant Impact from the U.S. Nuclear Regulatory Commission for their proposed advanced nuclear project in Seadrift, Texas.

- Together, these moves broaden Dow’s access to specialty materials customers and progress its plans for low-carbon industrial power and steam at a major U.S. manufacturing site.

- We’ll now examine how progress on Dow’s advanced nuclear project could influence its existing investment narrative built around capital discipline and asset optimization.

Outshine the giants: these 12 early-stage AI stocks could fund your retirement.

Dow Investment Narrative Recap

To own Dow, you need to be comfortable with a cyclical, capital‑intensive chemicals business that is currently unprofitable but focused on cash generation, asset optimization, and cost cuts. The Seadrift advanced nuclear milestone does not change the main near‑term catalyst, which remains execution on asset sales, cost savings, and European portfolio actions, nor the biggest current risk around sustained margin pressure from high feedstock and energy costs and a sluggish macro backdrop.

The recent NRC Finding of No Significant Impact for the Long Mott nuclear project is most relevant here, as it directly touches Dow’s long‑term energy and cost base. While still early in the permitting process, this step sits alongside project deferrals like Path2Zero and the expanded European asset review, giving investors more context on how Dow may be re‑shaping its footprint and future operating cost structure over time.

Yet, against this story of disciplined capital and cost focus, investors should be aware that prolonged margin pressure from energy and feedstock costs could still...

Read the full narrative on Dow (it's free!)

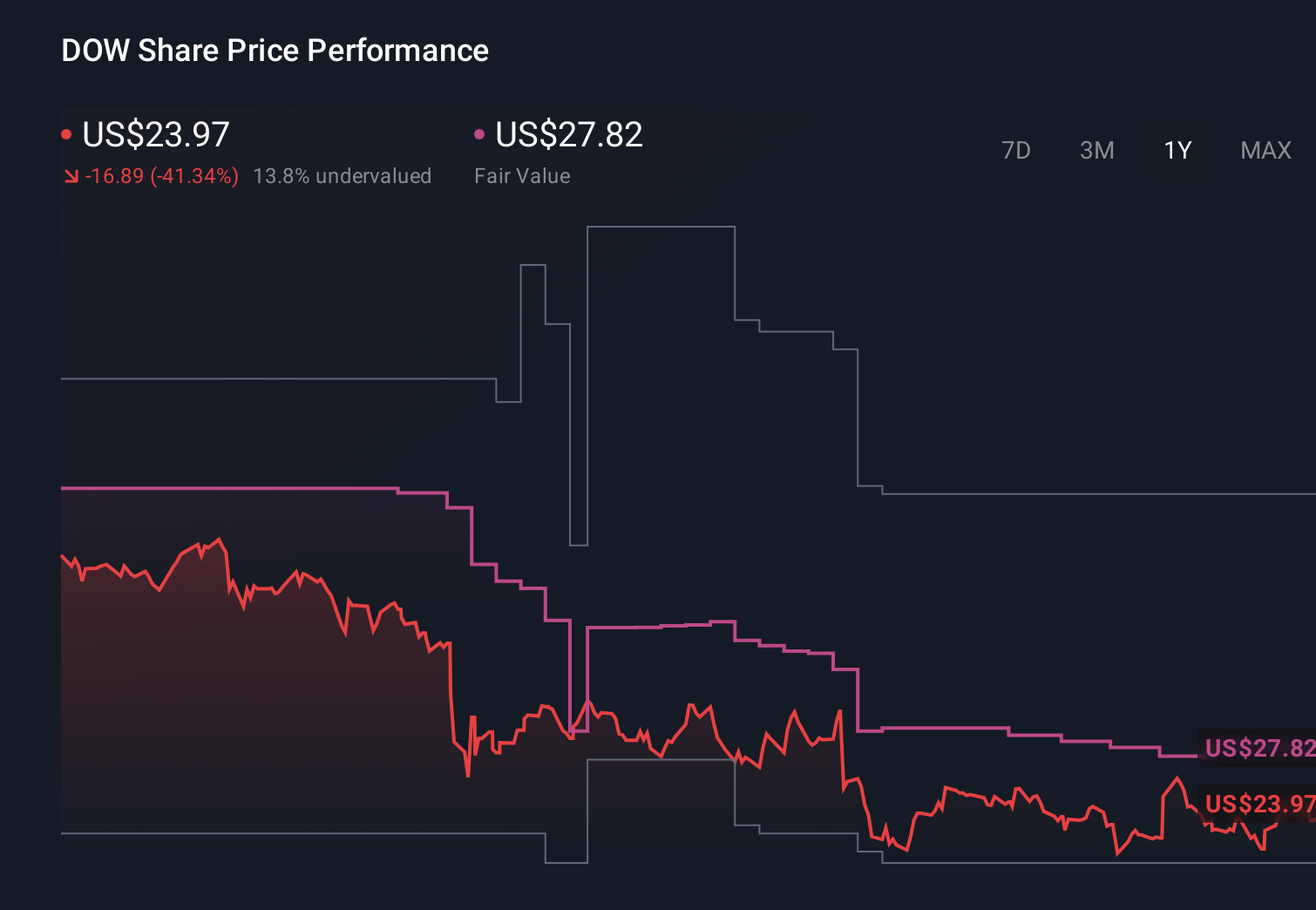

Dow's narrative projects $45.1 billion revenue and $1.6 billion earnings by 2029. This requires 4.6% yearly revenue growth and a $4.5 billion earnings increase from -$2.9 billion today.

Uncover how Dow's forecasts yield a $42.94 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in US$47.4 billion of revenue and US$1.7 billion of earnings by 2029, which contrasts sharply with concerns about delayed sustainability projects and possible structural oversupply, reminding you that interpretations of today’s nuclear and distribution news could shift these narratives in very different directions.

Explore 6 other fair value estimates on Dow - why the stock might be worth 20% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Dow research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Dow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dow's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com