- In late May 2026, The Hershey Company announced that Mitchell Arends will become Chief Supply Chain Officer on June 22, 2026, as long-time leader Jason Reiman steps aside and continues through early 2027 to oversee supply chain modernization and a smooth transition.

- The move brings in Arends’ extensive experience running large integrated supply chains at UTZ Brands and Kraft Heinz, underscoring Hershey’s intention to accelerate digital integration, automation, and insights-driven planning across its manufacturing and logistics network.

- We will now consider how this supply chain leadership change and push toward greater digital automation may affect Hershey’s existing investment narrative.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Hershey Investment Narrative Recap

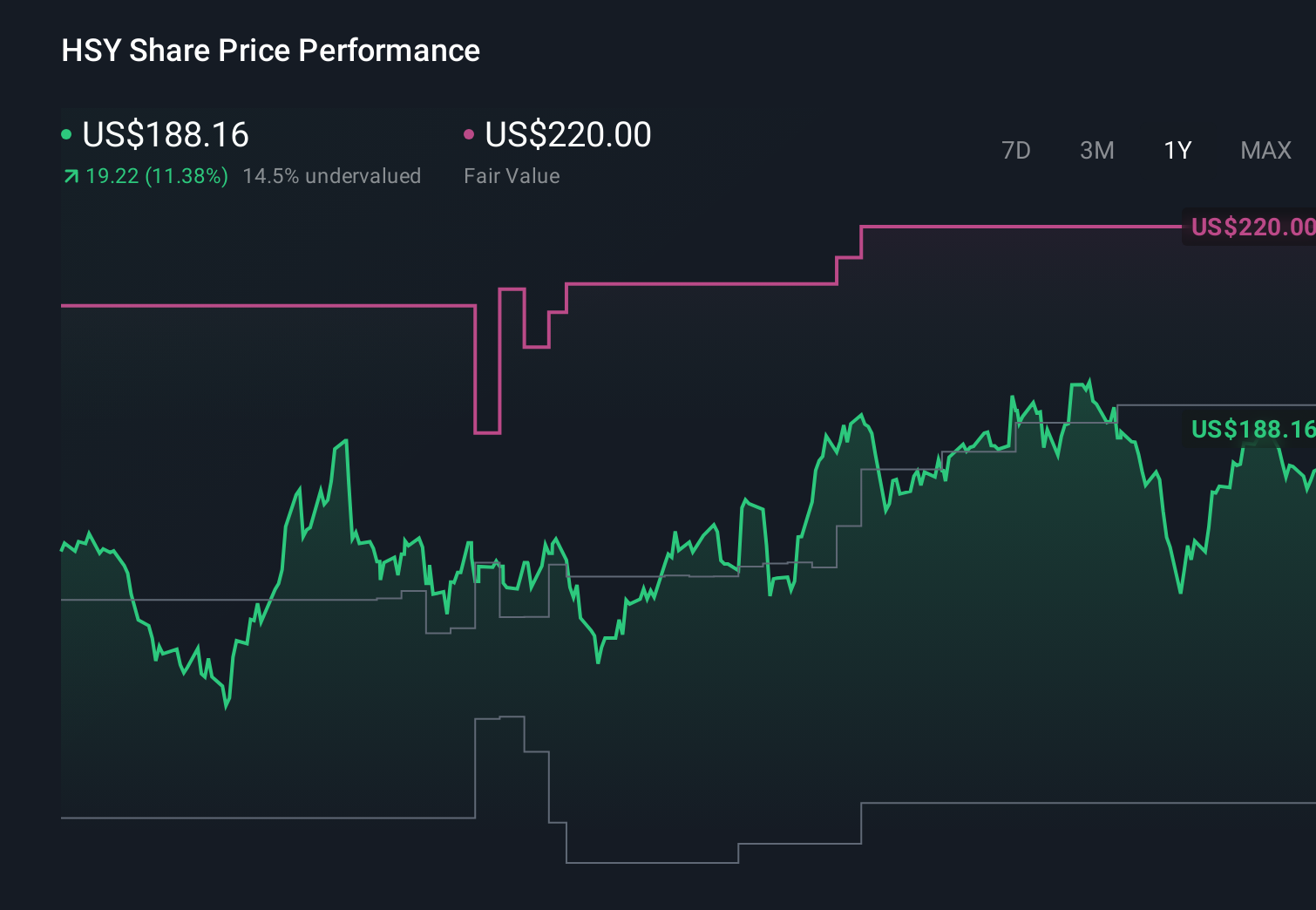

To own Hershey today, you generally need to believe its brands can keep earning solid returns even as cocoa costs, tariffs, and a weaker consumer squeeze margins. The new Chief Supply Chain Officer appointment looks incremental rather than transformative for near term earnings, though better execution in manufacturing and logistics could modestly support Hershey’s efforts to manage input cost and pricing risk.

Among recent announcements, Hershey’s reaffirmed 2026 guidance for 4%–5% net sales growth and US$7.77–US$8.19 in diluted EPS matters most here. Any supply chain gains under Mitchell Arends may eventually influence how confidently Hershey can stick to or refine that outlook, especially as it balances higher cocoa and tariff exposure with productivity programs and its push into snacks beyond chocolate.

Yet, despite these strengths, investors should still be alert to how prolonged cocoa inflation and tariff uncertainty could...

Read the full narrative on Hershey (it's free!)

Hershey's narrative projects $12.9 billion revenue and $2.1 billion earnings by 2029. This requires 3.4% yearly revenue growth and about a $1.2 billion earnings increase from $883.3 million today.

Uncover how Hershey's forecasts yield a $227.78 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts once projected Hershey’s earnings near US$2.4 billion and an 18.3% margin, but views differ widely and this supply chain shift could challenge or reinforce those expectations.

Explore 4 other fair value estimates on Hershey - why the stock might be worth as much as 52% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hershey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hershey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hershey's overall financial health at a glance.

No Opportunity In Hershey?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com