American International Group stock overview after recent performance

American International Group (AIG) has seen mixed share price movement recently, with the stock down over the past week and day but slightly higher over the past month, while year-to-date and 1-year returns are lower.

See our latest analysis for American International Group.

At a share price of US$77.05, AIG’s short term share price momentum has softened, although its multi year total shareholder returns, including dividends, have remained positive. This suggests sentiment has cooled after a stronger period for long term holders.

If this kind of mixed performance has you thinking about where else returns might be building, it could be a good moment to scan for potential opportunities in 20 top founder-led companies

With AIG stock easing this year yet still showing multi year gains, the key question now is whether its current US$77.05 price and earnings profile leave room for mispricing, or if the market is already pricing in future growth?

Most Popular Narrative: 10.9% Undervalued

On this view, American International Group’s fair value of $86.45 sits above the last close at $77.05, which is why many investors are studying the underlying thesis closely.

The acceleration of digitalization and artificial intelligence initiatives, such as the Gen AI deployment across underwriting and claims, positions AIG to enhance operational efficiency, improve underwriting precision, reduce fraud, and offer more tailored insurance products, supporting improved net margins and sustained earnings growth.

The core of this narrative is a detailed earnings blueprint built on efficiency gains, richer margins, and a recalibrated earnings multiple. Curious which assumptions really move that $86.45 fair value?

Result: Fair Value of $86.45 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on AIG containing climate and catastrophe losses, as well as keeping a lid on legal and claims inflation, which could quickly pressure margins and earnings expectations.

Find out about the key risks to this American International Group narrative.

Another angle on valuation

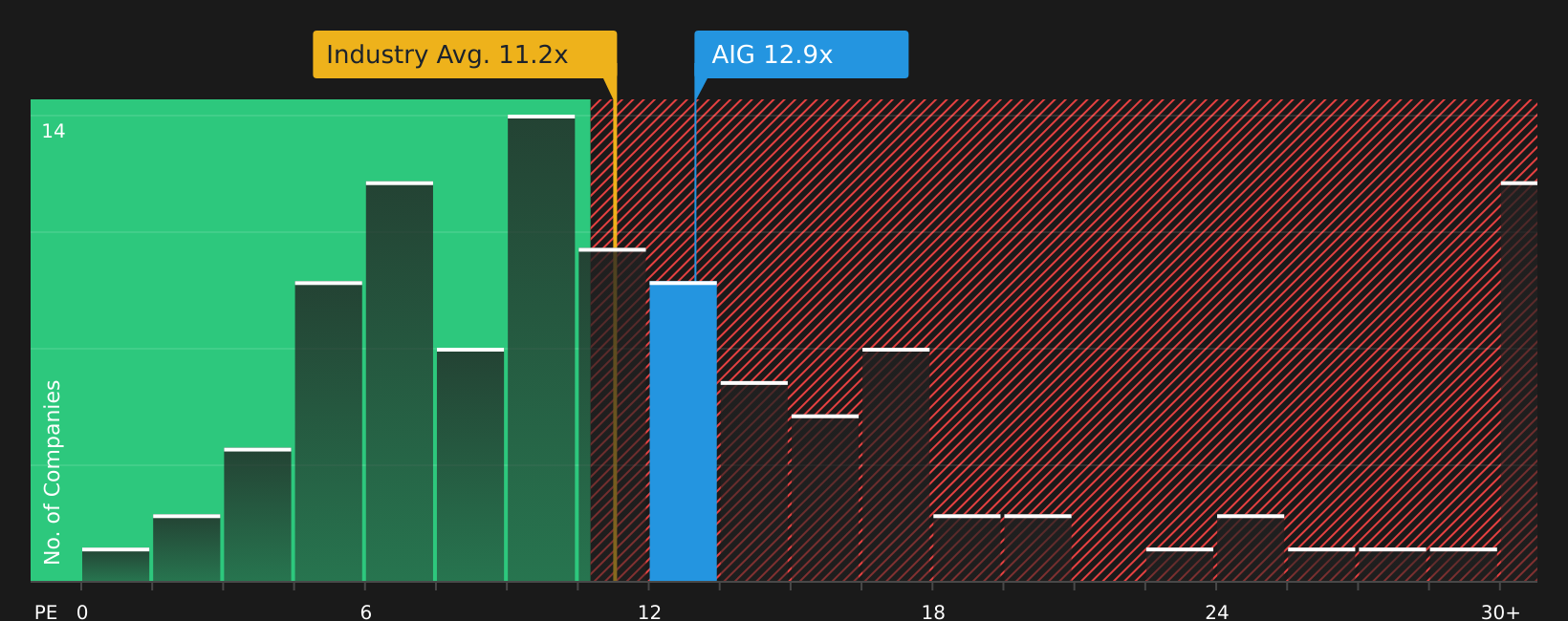

The earlier view argues AIG looks undervalued against its fair value estimate, yet the current P/E of 12.9x sits above the US Insurance industry at 11.3x, the peer average at 10.3x, and even above the fair ratio of 12.7x. That gap points to less of a clear bargain and more valuation risk if sentiment cools.

To see how those earnings multiples stack up in detail, and where the fair ratio suggests the market could drift next, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of signals leaves you on the fence, it can help to move quickly and test the assumptions against the data yourself, starting with the 3 key rewards.

Looking for more investment ideas?

Do not stop your research with a single stock. The best opportunities often show up where other investors are not looking yet.

- Target income potential with reliable cash flows by scanning for 10 dividend fortresses that could strengthen the foundation of your portfolio.

- Spot potential value gaps early by checking out screener containing 21 high quality undiscovered gems before they appear on everyone else's radar.

- Prioritize capital preservation while still staying invested by reviewing 69 resilient stocks with low risk scores that aim to keep risk in check without stepping completely to the sidelines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com