Moody's stock in focus after recent trading moves

Moody's (MCO) has drawn attention after recent price swings, with the stock up 0.8% over the past day and 4.7% over the past week, but down about 3.8% for the month.

See our latest analysis for Moody's.

Recent strength, with a 7 day share price return of 4.7% after a softer 30 day period, sits against a year to date share price decline of 10% and a 3 year total shareholder return of 47.1%. This suggests that momentum has cooled compared with longer term gains.

If you are comparing Moody's with other potential opportunities in financial services, it can be useful to scan a focused set of high quality businesses through a 20 top founder-led companies

With Moody's trading around $449.12 and an intrinsic value estimate that is roughly 3% above that, plus a sizeable gap to the average analyst target of $536, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 182.5% Overvalued

Against Moody's last close at $449.12, the most followed narrative pegs fair value at $159, implying a sizeable premium in the current share price.

Moody's Corporation is a regulatory-moated oligopoly wrapped in a compounding software business. The MIS ratings franchise holds the most durable structural position in financial services, the duopoly with S&P has been unbroken for over four decades, and the proprietary century-old default database cannot be replicated at any cost.

Want to understand why this framework still lands on a low fair value? The narrative leans on specific revenue growth, margin strength and a rich exit multiple. The tension between those assumptions and today’s price is the real story.

Result: Fair Value of $159 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this thesis still faces real tests, including potential shifts in credit rating regulation and any slowdown in demand for Moody's risk and compliance software tools.

Find out about the key risks to this Moody's narrative.

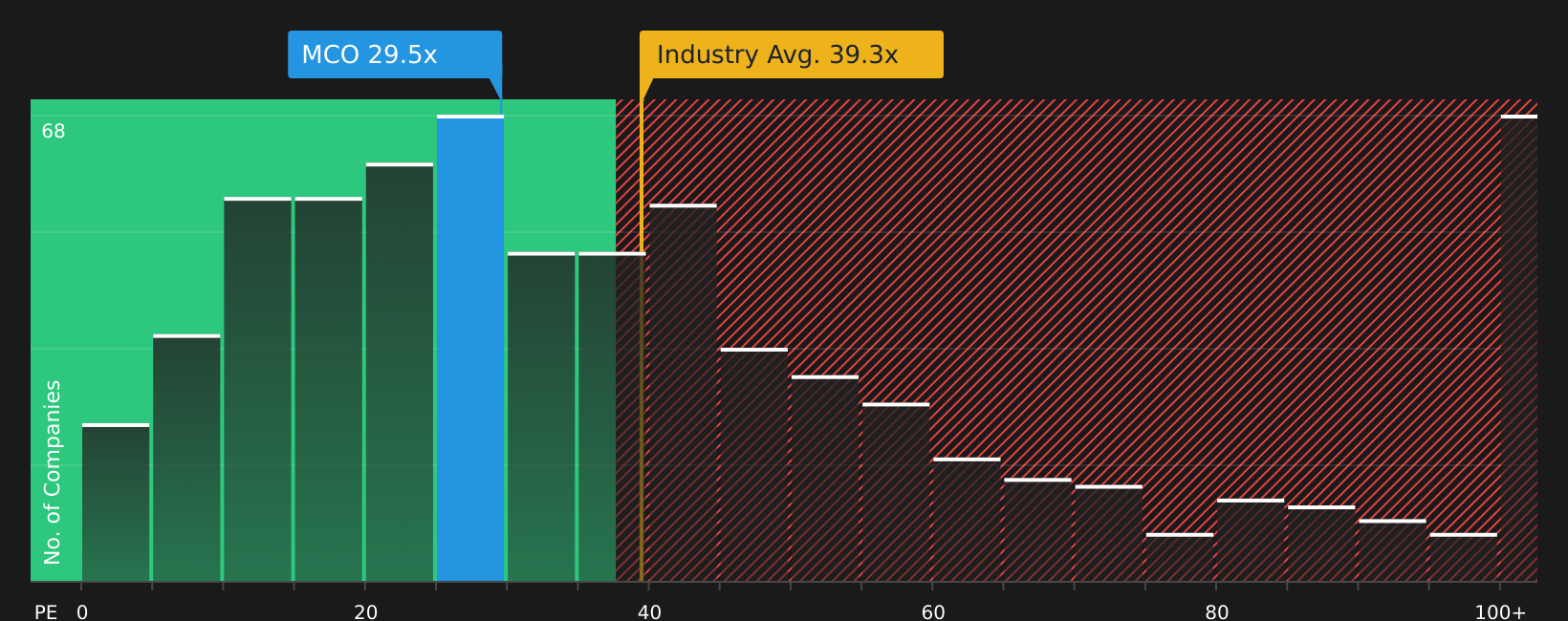

Another angle on valuation: earnings multiples

The narrative fair value of $159 suggests Moody's is expensive, but the current P/E of 31.4x sits below the US Capital Markets industry on 40.1x, even though it is above the peer average of 24.9x and the fair ratio of 17.2x that the market could move toward. That mix of relative discount and fair ratio premium raises a simple question for you: is the risk that expectations cool, or that peers and the fair ratio catch up instead?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of concern and optimism in this story, it is worth reviewing the numbers yourself to decide where you stand. Then check out the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Moody's has sharpened your focus, do not stop here. Use the tools available to compare quality, value and risk so your next move is deliberate.

- Target income potential by checking out companies offering reliable yields through the 10 dividend fortresses

- Hunt for value opportunities that pair strong fundamentals with appealing prices using the 49 high quality undervalued stocks

- Prioritize capital protection by focusing on resilient businesses through the 66 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com