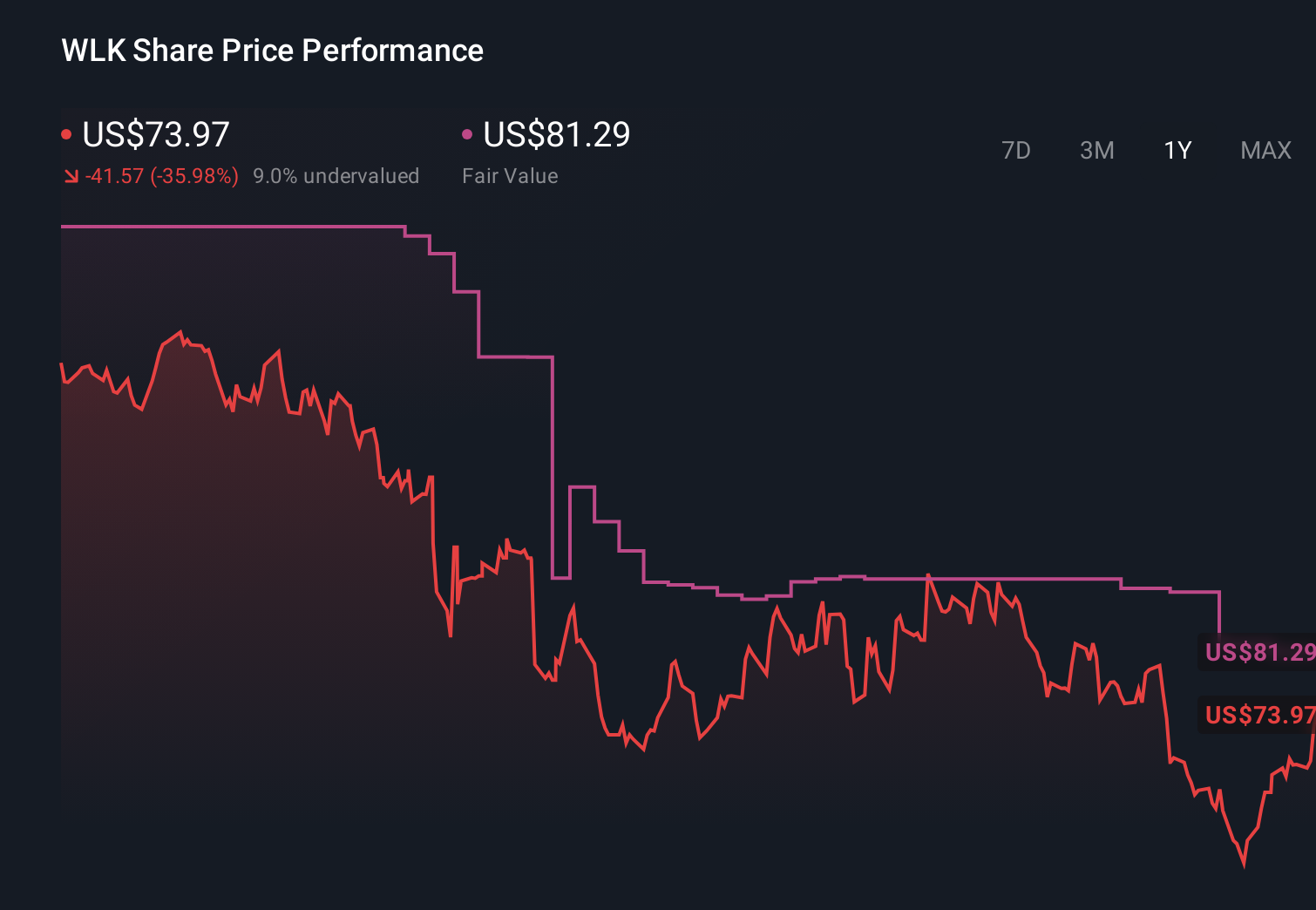

- Westlake Corporation recently reported first-quarter 2026 results showing sales of US$2,652 million versus US$2,846 million a year earlier and a net loss of US$169 million, and subsequently declared a regular first-quarter 2026 dividend of US$0.53 per share, paid on June 11, 2026 to shareholders of record on May 27, 2026.

- An interesting contrast for investors is Westlake’s decision to maintain its regular dividend despite reporting a wider quarterly loss than in the prior year.

- We’ll now examine how Westlake’s decision to maintain its regular dividend despite a wider quarterly loss affects its investment narrative.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Westlake Investment Narrative Recap

To own Westlake, you generally need to believe its mix of basic chemicals and housing and infrastructure products can return to consistent profitability, supported by long term construction and municipal spending. The latest quarter’s wider net loss of US$169 million on lower sales adds weight to concerns about margin pressure and weak demand, but the decision to hold the dividend at US$0.53 per share does not materially change the near term earnings risk that is already front of mind.

The most relevant recent announcement here is the first quarter 2026 earnings release, which showed a larger net loss of US$169 million compared with US$40 million a year earlier. Against that backdrop, keeping the dividend unchanged highlights the tension between returning cash to shareholders and addressing ongoing pressures from global oversupply, cost inflation and underutilized assets, all of which remain central to the short term earnings catalyst for Westlake.

Yet behind this steady dividend, one risk investors should be aware of is prolonged weak demand and pricing in key chemical chains that could...

Read the full narrative on Westlake (it's free!)

Westlake's narrative projects $12.8 billion revenue and $364.4 million earnings by 2029. This requires 4.6% yearly revenue growth and an earnings increase of about $1.9 billion from -$1.5 billion today.

Uncover how Westlake's forecasts yield a $121.29 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming flat revenue near US$11.2 billion and only US$255.7 million of earnings by 2029, a far more pessimistic path than the cost savings and footprint improvements many others focused on before this latest loss, reminding you that views on Westlake can differ widely and may shift again as the impact of these results becomes clearer.

Explore 3 other fair value estimates on Westlake - why the stock might be worth 25% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Westlake research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 43 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com