What recent performance suggests about Nelnet’s stock

Nelnet (NNI) has drawn fresh attention after a recent move in its share price, with the stock roughly flat over the past week but showing a gain over the past month and past 3 months.

See our latest analysis for Nelnet.

Looking beyond the latest move, Nelnet’s 30 day share price return of 9.43% and year to date share price return of 9.82% sit alongside a 1 year total shareholder return of 33.95%. Taken together, these figures suggest that momentum has been building over time.

If Nelnet’s recent gains have you thinking about where else you could put money to work, this can be a good moment to broaden your search and uncover 17 top founder-led companies

With the stock around $141.66 and trading at a small premium to the US$135 analyst price target and intrinsic value estimate, the key question is whether this reflects full value already or if the market is underestimating its future growth potential.

Preferred P/E of 11.9x: Is it justified?

On a P/E of 11.9x, Nelnet trades above both the US Consumer Finance industry average of 9.8x and the peer average of 10x. Its last close sits at $141.66.

The P/E ratio compares the share price to earnings per share and is a quick way to see how much investors are paying for each dollar of profit. For a company with consumer finance exposure and diversified service lines, this is a common yardstick for how the market is pricing current earnings against expectations.

Here, the market is assigning Nelnet a richer P/E than its industry and peer averages, which points to investors paying a premium for its earnings profile. At the same time, the P/E remains below the broader US market P/E of 19.4x. As a result, the premium appears more concentrated when you compare it directly with sector peers rather than the whole market.

That sector comparison is important, because a P/E above both the industry and peer averages suggests the market is more optimistic about Nelnet than about similar consumer finance stocks. This comes even though its long term earnings record includes a 15.6% per year decline over 5 years and its forecast revenue growth of 3.3% per year is slower than the wider US market growth forecast.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 11.9x (OVERVALUED).

However, higher expectations baked into the P/E and exposure to multiple regulated activities, including banking and student lending, could quickly challenge the current optimism if conditions turn.

Find out about the key risks to this Nelnet narrative.

Another way to look at Nelnet’s value

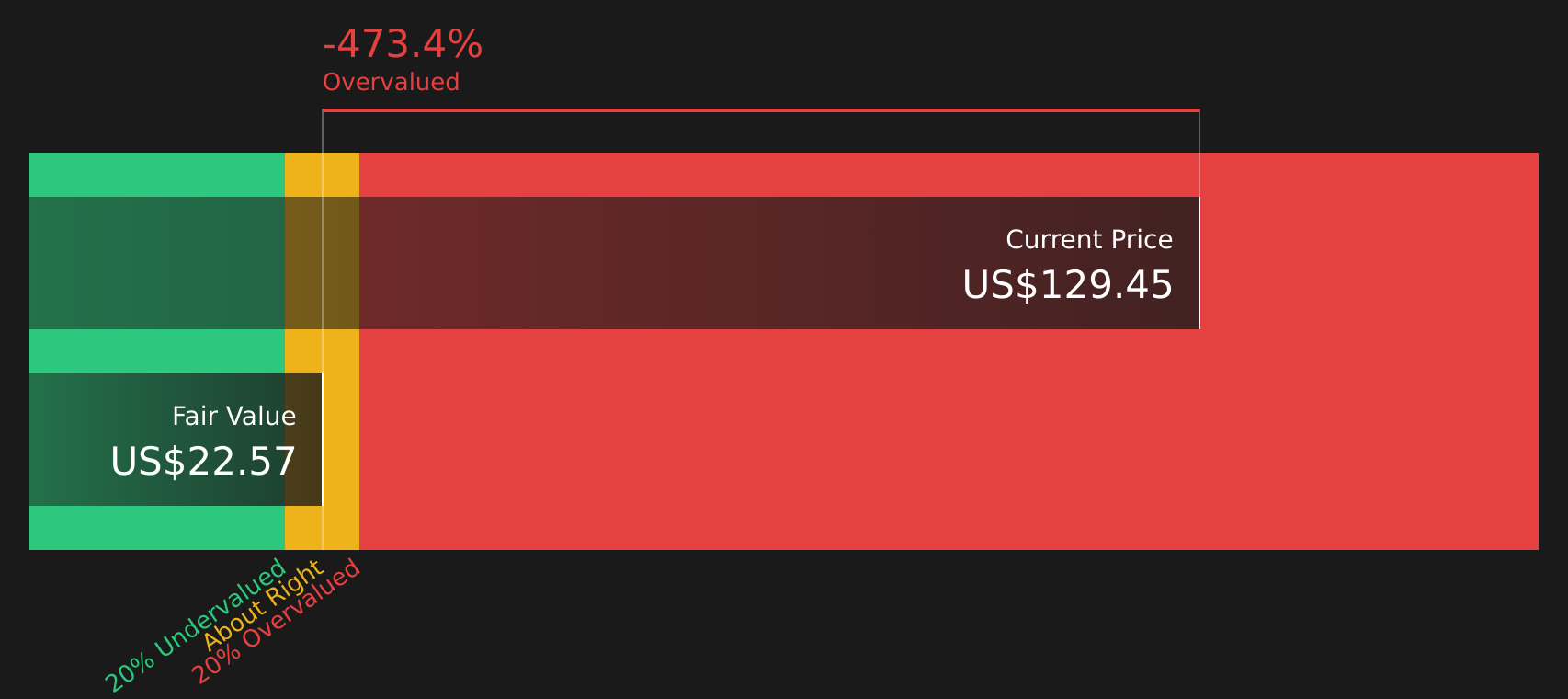

While the 11.9x P/E suggests the stock is expensive relative to Consumer Finance peers, the Simply Wall St DCF model points to an even starker picture, with an estimated future cash flow value of $23.64 versus a share price of $141.66. That gap raises a simple question: is the market pricing in too much?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nelnet for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment, this is a useful moment to look at the underlying data yourself, weigh the concerns against the potential upsides, and decide how comfortable you are with that balance in your own portfolio using 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Nelnet has sharpened your focus on valuation and risk, do not stop here. Broaden your watchlist with ideas that match different goals and comfort levels.

- Target steady compounding potential by reviewing 72 resilient stocks with low risk scores, which aim to keep volatility and fundamental risk in check.

- Hunt for quality at a discount through the 49 high quality undervalued stocks, where pricing and fundamentals line up more tightly.

- Strengthen your search for resilient balance sheets with the solid balance sheet and fundamentals stocks screener (44 results) to spot companies that may better withstand tougher conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com