- On April 8, 2026, Life Time Inc. fully opened Life Time Eagle, its first 135,000-square-foot athletic country club in Idaho, adding one of the Treasure Valley’s largest recent wellness developments and employing more than 200 people.

- This expansion extends Life Time’s nearly 190-club North American network into the Boise area, highlighting its focus on comprehensive, premium wellness experiences that integrate fitness, recovery, family amenities and social spaces.

- We’ll now explore how this large-scale Idaho opening, with its extensive racquet sports and recovery facilities, may influence Life Time’s broader investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Life Time Group Holdings Investment Narrative Recap

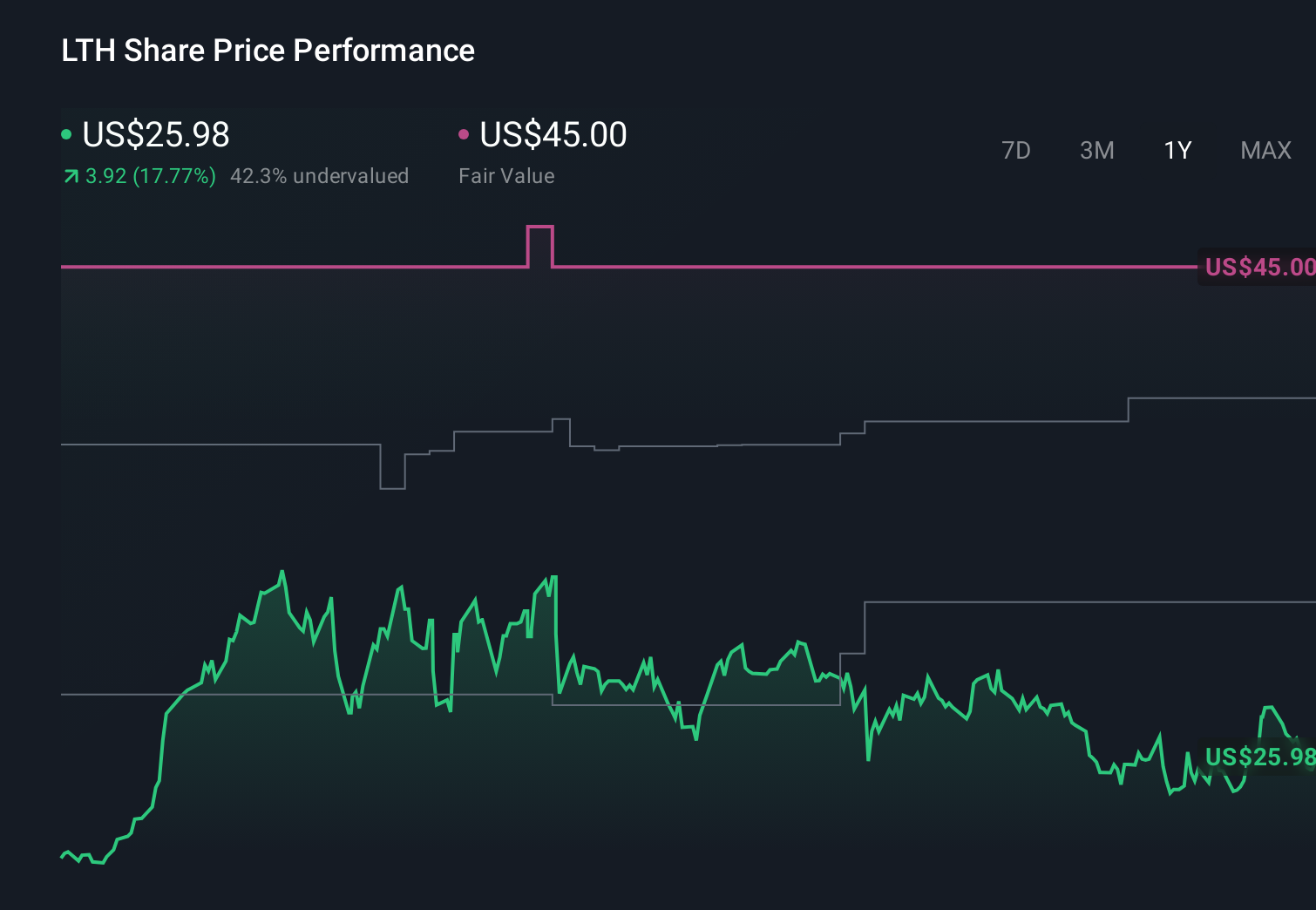

To own Life Time, you need to believe its premium, destination-club model can keep attracting and retaining members while supporting capital-heavy expansion. The Eagle opening in Idaho fits this thesis by extending the network into a new, affluent market, but it also reinforces the core risk: large, ground-up clubs require significant capital, leaving results sensitive to construction costs, interest rates and sale-leaseback markets. In the near term, the most important catalyst remains execution on the broader new-club pipeline and maintaining utilization across existing locations.

Among recent announcements, the US$500,000,000 share repurchase authorization from February 2026 is particularly relevant. It arrived alongside guidance calling for 2026 revenue of US$3,300 million to US$3,330 million and net income of US$330 million to US$336 million, all while Life Time continues to open large clubs such as Eagle. For investors, this combination of cash returned via buybacks and high capital expenditure underscores how dependent the story is on sustaining healthy cash generation and access to real estate financing.

Yet behind Life Time’s premium growth story, investors should also weigh how its heavy expansion and financing needs could affect returns if conditions change...

Read the full narrative on Life Time Group Holdings (it's free!)

Life Time Group Holdings' narrative projects $4.1 billion revenue and $448.6 million earnings by 2029. This requires 10.8% yearly revenue growth and an earnings increase of about $74.9 million from $373.7 million today.

Uncover how Life Time Group Holdings' forecasts yield a $40.00 fair value, a 43% upside to its current price.

Exploring Other Perspectives

More cautious analysts see Life Time very differently, warning that the same rapid expansion that adds clubs like Eagle could strain finances, even as they still penciled in revenue of about US$4,000 million and earnings of roughly US$408 million by 2029, reminding you that opinions on the stock’s risk and reward can diverge sharply and may shift again as new openings like Idaho play through the numbers.

Explore 3 other fair value estimates on Life Time Group Holdings - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com