Wyndham Hotels & Resorts (WH) is back in focus after its Trademark Collection surpassed 100 U.S. hotels and the company named Amit Sripathi as CFO, alongside broader development leadership changes.

See our latest analysis for Wyndham Hotels & Resorts.

Those brand milestones and leadership changes come as the share price has recorded a 7.02% 1 month share price return and a 9.15% year to date share price return. The 3 year total shareholder return of 30.11% points to steadier long term gains.

If you are comparing Wyndham with other potential opportunities in travel related and experience driven themes, it can be useful to see what else is moving using the 20 top founder-led companies

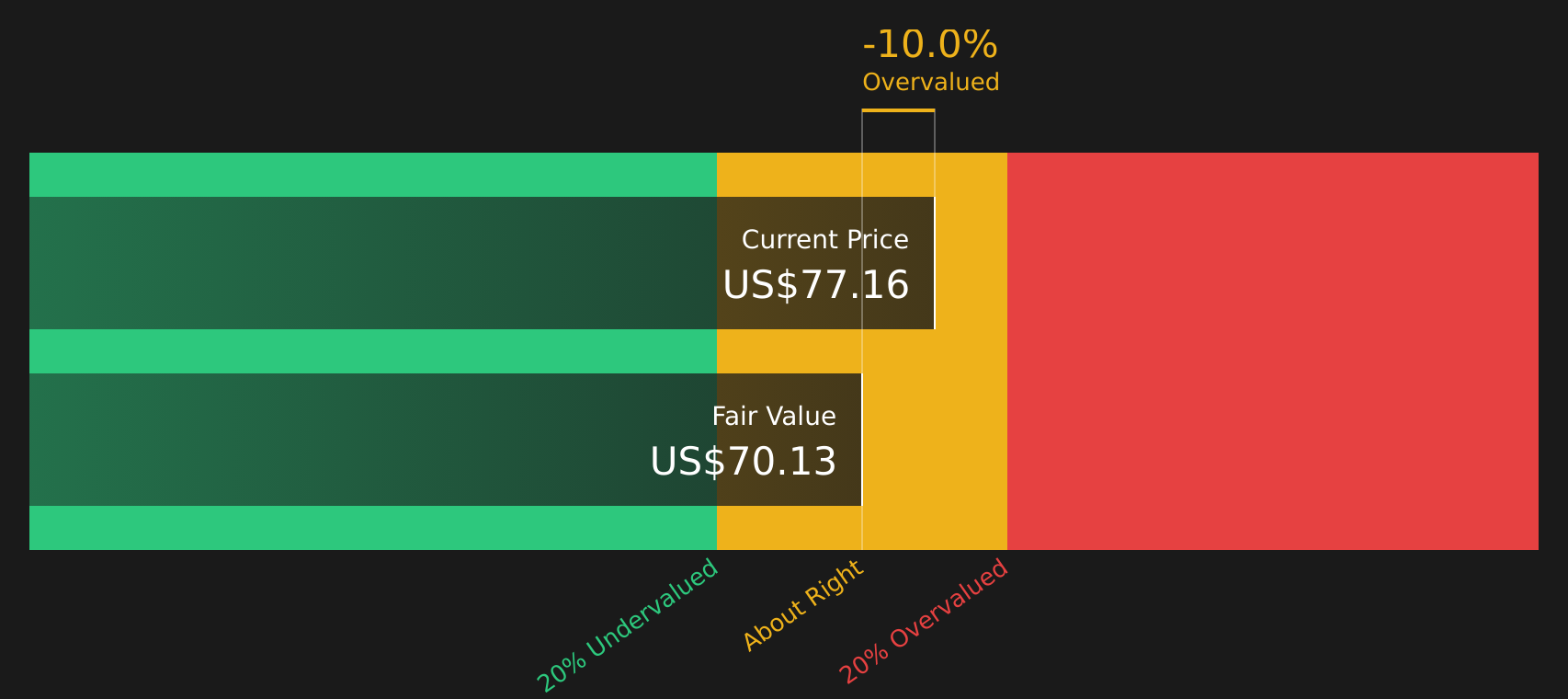

With Wyndham trading at $82.16, alongside an indicated 20.70% intrinsic discount and an 18.06% gap to analyst targets, the question is whether the market is still underestimating its hotel franchising engine or is already pricing in future growth.

Most Popular Narrative: 15.3% Undervalued

With Wyndham shares at $82.16 against a narrative fair value of $97.00, the current price sits below what this widely followed view considers reasonable, setting up an interesting tension between market pricing and long term franchise and fee based potential.

Record development pipeline growth, with contract signings up 40% and new, high FeePAR-accretive hotels comprising a larger share of additions, enhances base royalty rate accretion and fee-related revenue, directly supporting higher net margins and long-term earnings potential.

Want to see what is powering that pipeline story into a higher fair value? The core of this narrative blends steady top line expansion, a sharp margin reset and a future earnings multiple that implies real confidence in the fee engine. Curious which specific growth and profitability assumptions have to line up to reach that $97.00 figure?

Result: Fair Value of $97.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can unwind if U.S. RevPAR weakens for an extended period or if overlapping midscale and economy brands begin to dilute pricing power and owner returns.

Find out about the key risks to this Wyndham Hotels & Resorts narrative.

Another Angle on Valuation

The SWS DCF model points to a fair value of $103.60 for Wyndham, with the current price of $82.16 sitting below that estimate. This contrasts with a P/E of 31.9x that looks expensive versus peers and the US Hospitality industry. Which signal do you think matters more for your own thesis?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Seeing mixed signals on Wyndham so far? Take a closer look at both sides of the story and weigh the 2 key rewards and 5 important warning signs

Looking for more investment ideas?

If you stop with just one company, you risk missing out on other opportunities that match your style, so put the Simply Wall St screener to work.

- Spot potential value opportunities by scanning 58 high quality undervalued stocks that combine quality fundamentals with room for the market to re-rate them.

- Prioritize resilience by focusing on 68 resilient stocks with low risk scores that aim to keep overall portfolio risk in check.

- Hunt for lesser known opportunities across the screener containing 25 high quality undiscovered gems that might not yet be on every investor's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com