- In recent days, Vulcan Materials has attracted attention as investors reacted to management’s 2026 guidance, recent earnings miss, and shifting analyst opinions, all set against strong cash flow and industry tailwinds that were previously highlighted.

- The key development is that management’s expectations for modest growth in aggregate shipments and adjusted EBITDA, combined with favorable sector trends, appear to have strengthened investor confidence despite earlier earnings challenges and mixed brokerage updates.

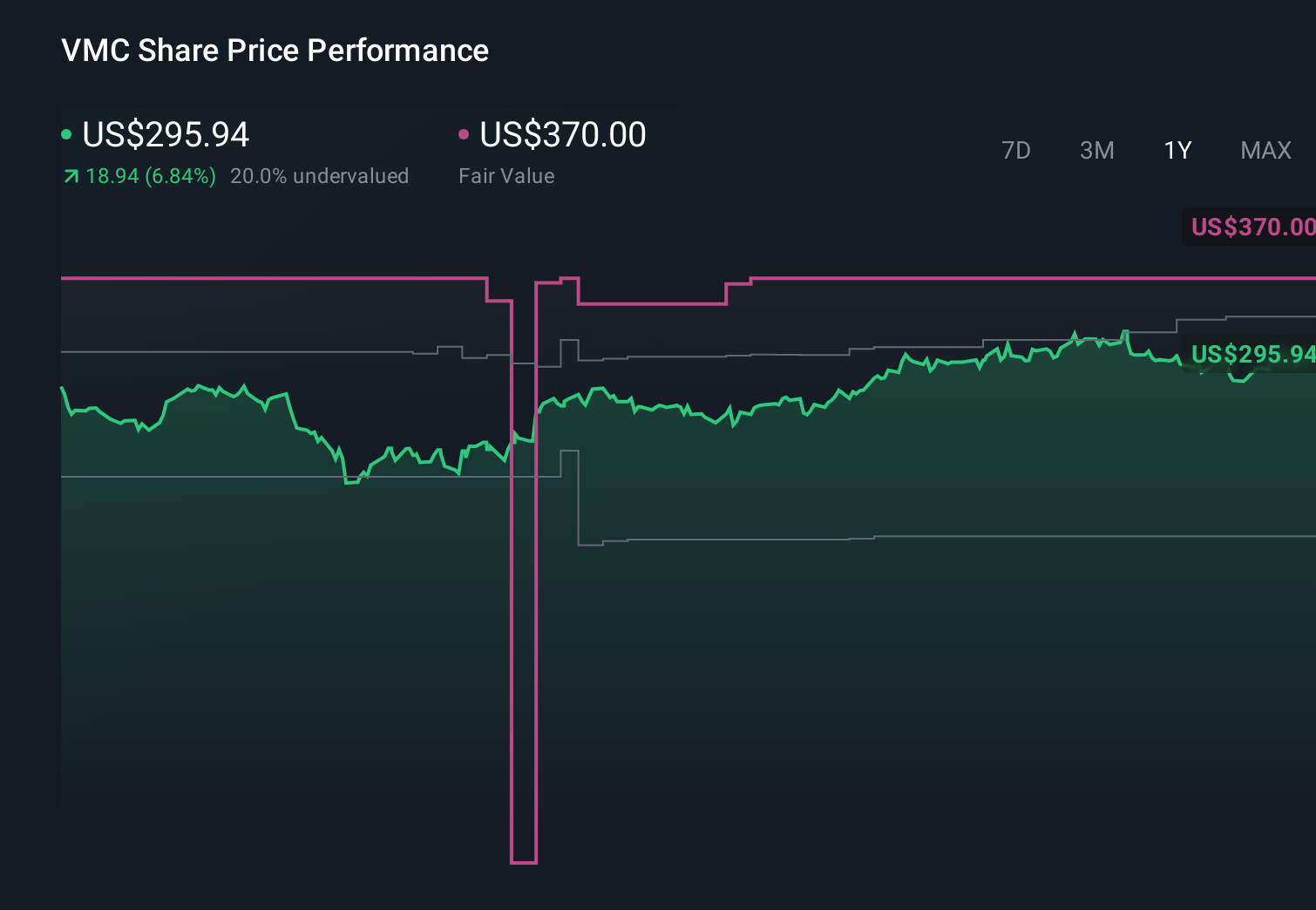

- Now we’ll examine how management’s 2026 guidance for modest growth in aggregate shipments and adjusted EBITDA reshapes Vulcan Materials’ investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 26 companies in the world exploring or producing it. Find the list for free.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you generally need to believe that steady aggregate demand from infrastructure and non-residential projects will matter more than quarter-to-quarter earnings noise. The latest guidance for modest 2026 growth in shipments and adjusted EBITDA, along with an “Outperform” analyst consensus, supports that view and appears to have eased immediate concerns after the recent earnings miss. The biggest near term risk still looks tied to project timing and funding, and this news does not materially change that.

Among the recent announcements, management’s 2026 outlook and the reaffirmed Barclays Overweight rating, even with a reduced US$296 price target, are most relevant. Together, they highlight how modest growth expectations in volume and profitability, set against favorable infrastructure trends, can still underpin confidence in Vulcan’s long-term aggregates story, even as mixed quarterly results and cautious EPS estimates keep short term sentiment sensitive around execution and valuation.

Yet behind this improving sentiment, investors should be aware of how project delays and funding shifts could still...

Read the full narrative on Vulcan Materials (it's free!)

Vulcan Materials' narrative projects $9.6 billion revenue and $1.5 billion earnings by 2028. This requires 8.1% yearly revenue growth and roughly a $541.9 million earnings increase from $958.1 million today.

Uncover how Vulcan Materials' forecasts yield a $327.57 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already more cautious, assuming Vulcan’s revenue would reach about US$9.0 billion and earnings US$1.6 billion by 2029, and the latest guidance plus analyst revisions may either reinforce that caution or soften it, depending on how you weigh those projections against the risk that stricter environmental rules could lift costs and limit new quarries over time.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth 7% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com