- In late March 2026, JLens and the Anti-Defamation League urged GE Aerospace shareholders to oppose a proposal criticizing the company’s defense sales to Israel and calling for a human-rights due diligence report, arguing it could harm its defense business and misplace political debates in the boardroom.

- At the same time, GE Aerospace has drawn heightened analyst and investor attention as it reports strong operating results and expands partnerships, even as geopolitical tensions and security threats increasingly intersect with its role as a major defense and commercial aviation supplier.

- We’ll now examine how this shareholder activism around GE Aerospace’s defense ties to Israel may influence the company’s investment narrative.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

General Electric Investment Narrative Recap

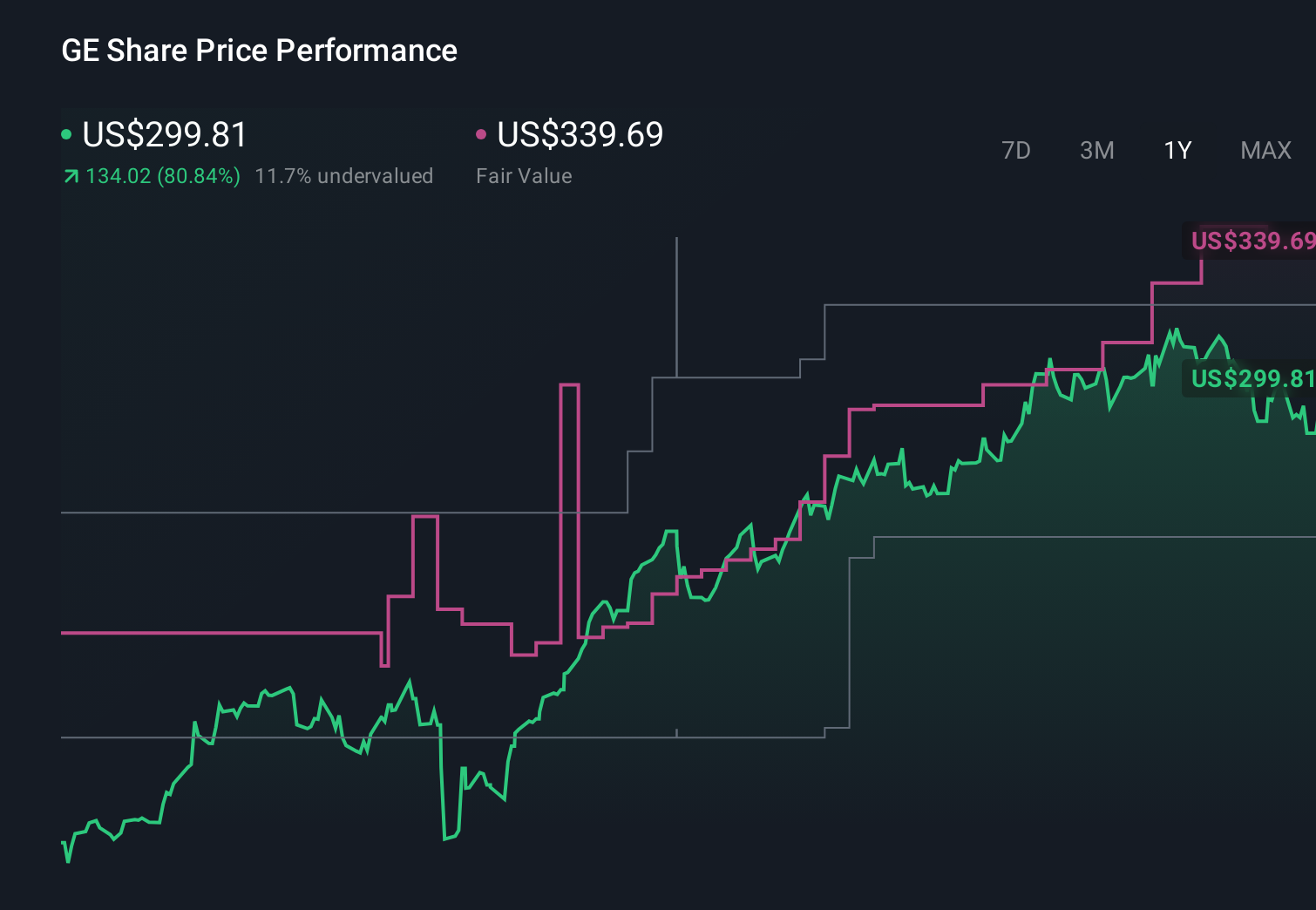

To own GE Aerospace today, you need to believe in its core engine and services franchise and its ability to manage both commercial and defense exposure. The most important near term catalyst remains execution on its US$190 billion backlog and 2026 EPS guidance, while a key risk is sentiment around defense programs and geopolitical shocks. The recent Israel focused shareholder proposal and the campaign against it may influence how some investors view GE’s reputation, but it does not materially change these core drivers.

The recent expansion of GE Aerospace’s partnership with Palantir is especially relevant here, since it ties directly into defense readiness and data driven fleet support at a time when geopolitical tensions are high and digital capabilities are increasingly central to the company’s value proposition. This kind of program sits at the intersection of GE’s biggest catalyst efficient backlog conversion and its biggest risk potential pushback on the scope and visibility of its defense work.

But alongside the optimism, investors should be aware of how rising geopolitical tensions and targeted threats against US defense contractors could affect GE’s margin resilience and...

Read the full narrative on General Electric (it's free!)

General Electric's narrative projects $50.8 billion revenue and $9.5 billion earnings by 2028. This requires 6.9% yearly revenue growth and a $1.9 billion earnings increase from $7.6 billion today.

Uncover how General Electric's forecasts yield a $357.24 fair value, a 27% upside to its current price.

Exploring Other Perspectives

While the base case focuses on backlog strength, the most pessimistic analysts were already assuming only 5.3% annual revenue growth and flat earnings around US$6.9 billion, reminding you that views on how far defense and climate related risks can bite into GE’s jet engine business can differ sharply and may shift again after this latest round of shareholder activism.

Explore 8 other fair value estimates on General Electric - why the stock might be worth just $270.93!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Electric research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com