Why Norfolk Southern’s Doraville partnership matters for shareholders

Norfolk Southern (NSC) has drawn fresh attention after partnering with Jaguar Transport Holdings to run its Doraville, Georgia, transload terminal, handle local switching, and fund targeted rail infrastructure upgrades to support additional freight volumes.

See our latest analysis for Norfolk Southern.

Against this backdrop, Norfolk Southern’s 1 year total shareholder return of 22.75% and 3 year total shareholder return of 51.26% contrast with a weaker 30 day share price return of a 9.60% decline, suggesting momentum has cooled recently even as longer term holders remain ahead.

If this kind of rail partnership has you thinking about where else growth and infrastructure themes might show up in your portfolio, it is worth scanning 27 power grid technology and infrastructure stocks

With NSC trading at $287.00 against an average analyst target of $313.11, alongside a recent 30-day share price decline and a value score of 2, is this rail giant still cheap or is future growth already fully reflected in the price?

Most Popular Narrative: 8.6% Undervalued

The most followed narrative currently pegs Norfolk Southern’s fair value at about $314.11, compared with the last close at $287.00. It frames today’s price against a long term rail infrastructure story built around efficiency gains, intermodal corridors and potential merger benefits.

The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could bolster future revenue growth.

Strategic plans to capitalize on industrial development activity, particularly in sectors like steel and food production, along with the potential for highway-to-rail conversions, are expected to provide new demand drivers for volume growth, supporting long-term revenue enhancement.

Want to see what kind of revenue path and profit profile are baked into that fair value? The narrative leans on steady expansion, firm margins and a richer earnings multiple. Curious which specific assumptions really move the gap between $287.00 and $314.11?

Result: Fair Value of $314.11 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on risks around storm restoration costs and on regulatory uncertainty tied to the proposed Union Pacific merger, either of which could challenge the current fair value story.

Find out about the key risks to this Norfolk Southern narrative.

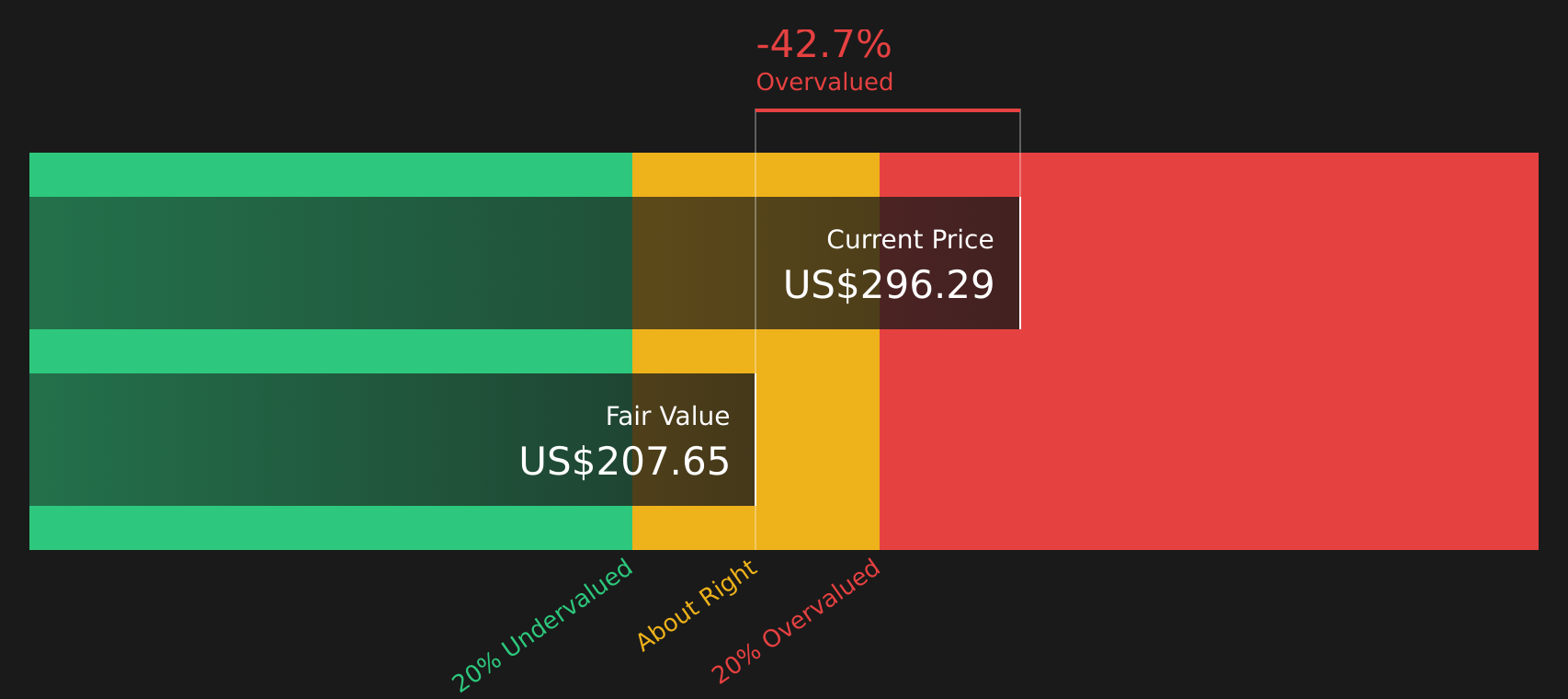

Another angle on valuation: what the cash flows say

While the popular narrative points to an 8.6% gap between the $287.00 share price and a $314.11 fair value, the Simply Wall St DCF model paints a different picture. On that view, NSC at $287.00 sits above an estimated future cash flow value of $207.94, which implies the shares look expensive rather than underpriced. Which story do you think better fits how you see NSC’s long term cash generation?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norfolk Southern for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 63 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern around Norfolk Southern leaves you undecided, take a closer look at the full picture and weigh the 4 key rewards and 1 important warning sign

Ready for more ideas beyond Norfolk Southern?

If you stop with just one company, you could miss opportunities that better fit your goals. Take a few minutes to scan focused stock ideas built from clear fundamentals.

- Target reliable income by checking out companies in the 12 dividend fortresses that may suit a long term, cash flow focused approach.

- Hunt for potential value opportunities by reviewing the 63 high quality undervalued stocks that pair quality fundamentals with discounted prices.

- Prioritize resilience by focusing on the 65 resilient stocks with low risk scores that score well on financial strength and risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com