Why InterDigital stock is back on investor radar

InterDigital (IDCC) is in focus after securing a preliminary injunction in Brazil against Transsion over alleged 5G patent infringement, a decision that directly affects device shipments in an important smartphone market.

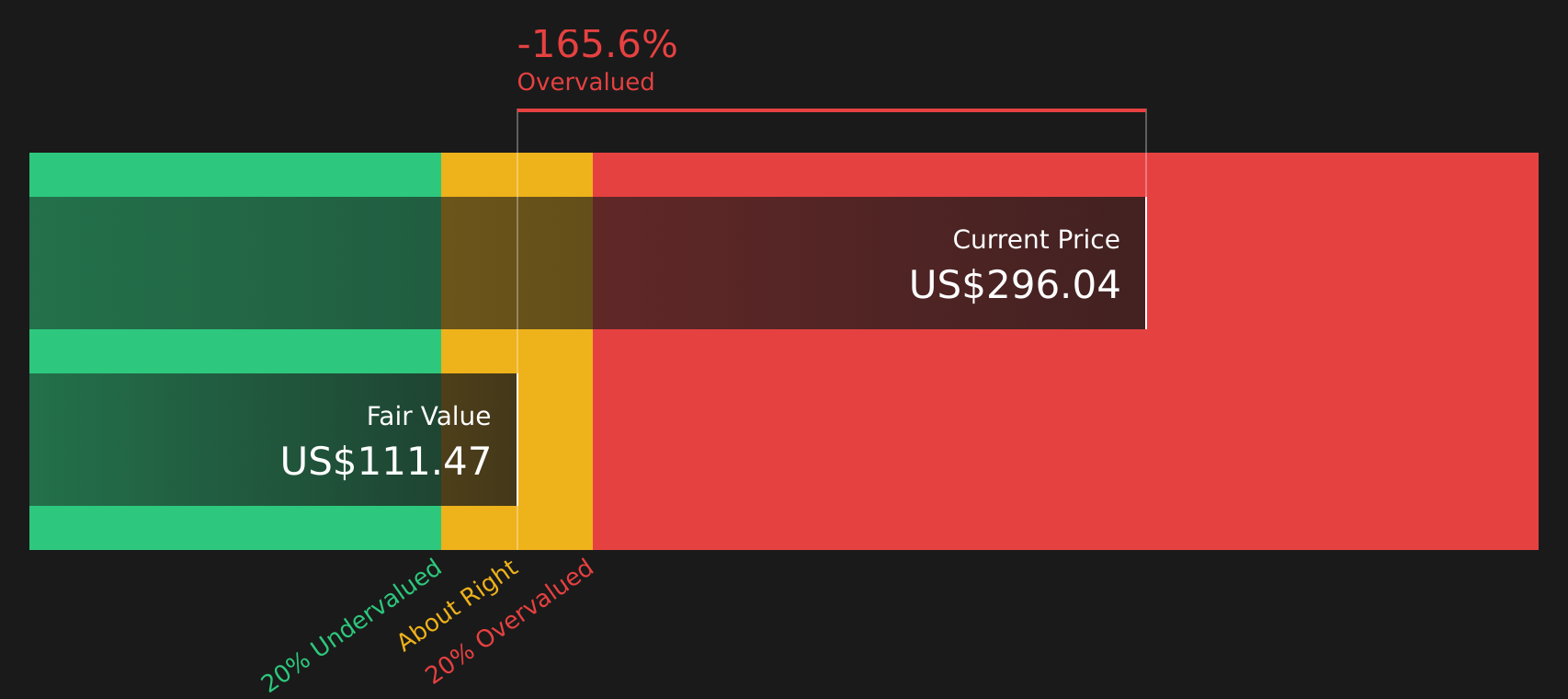

See our latest analysis for InterDigital.

The injunction news follows a weaker 30-day share price return of a 17.6% decline and a year-to-date share price return of a 7.4% decline, set against a 1-year total shareholder return of 48.9% that points to longer-term momentum still being intact.

If this legal outcome has you thinking about other growth stories tied to data traffic and computing demand, it could be a good moment to scan 36 AI infrastructure stocks

With InterDigital shares down 17.6% over 30 days but still showing a 1 year total return of 48.9%, and trading below the average analyst price target, should you view this as potential untapped value or conclude that the current price already reflects expectations for future growth?

Most Popular Narrative: 35% Undervalued

With InterDigital last closing at $302.00 against a narrative fair value of $462.67, the current share price sits well below what this widely followed model implies. This puts the spotlight on the assumptions behind that gap.

The analysts have a consensus price target of $266.5 for InterDigital based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $311.0, and the most bearish reporting a price target of just $220.0.

Want to see what justifies a fair value well above both the current price and the analyst consensus? The narrative focuses on margin strength, recurring licensing cash flows, and a long runway of projected earnings that together support a higher implied multiple.

Result: Fair Value of $462.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat fair value view still hinges on aggressive revenue and margin assumptions, as well as a lower discount rate that could prove optimistic if licensing cash flows face pressure.

Find out about the key risks to this InterDigital narrative.

Another Way to Look at Value

While the narrative fair value of $462.67 points to upside, a different approach tells a more cautious story. The Simply Wall St DCF model estimates InterDigital’s future cash flows at $165.97 per share, which is well below the current $302 price. Which story do you think better fits the risk you are willing to take?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment running both hot and cold, it helps to look at the full picture yourself. Act promptly, review the underlying numbers, and weigh up the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If InterDigital has caught your attention, do not stop there. Broaden your watchlist with other focused ideas that could suit your goals and risk comfort.

- Target potential value opportunities by scanning 58 high quality undervalued stocks, which already pair stronger fundamentals with pricing that may still leave room for upside.

- Secure more reliable income streams by checking out 12 dividend fortresses, where yields start at 5% and are backed by robust business profiles.

- Prioritise resilience first by reviewing 64 resilient stocks with low risk scores, which score well on financial strength and lower overall risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com