- CAVA Group, Inc. recently entered into a Third Amendment to its March 2022 credit agreement, extending the credit facility’s maturity to March 20, 2031 and increasing revolving commitments from US$75,000,000 to US$150,000,000, with borrowings secured by first-priority liens on substantially all company and guarantor assets.

- This enhanced, asset-backed revolving capacity and longer-dated funding horizon materially strengthen CAVA’s liquidity toolkit, potentially supporting future restaurant expansion, technology investments, and operational initiatives within the constraints of its covenants.

- We’ll now examine how the extended 2031 maturity and doubled revolving commitments could reshape CAVA’s investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

CAVA Group Investment Narrative Recap

To own CAVA, you generally need to believe its Mediterranean fast casual concept can keep drawing traffic and support disciplined expansion toward its long term restaurant goals. The expanded credit facility to US$150,000,000 and extended 2031 maturity improve financial flexibility, which could help fund new units and technology, but it does not eliminate key near term risks such as potential menu fatigue, market saturation from rapid openings, or cost pressures that could weigh on margins.

Recent new market entries, such as CAVA’s first Ohio restaurant in Cincinnati, show the company is still leaning into its long term target of at least 1,000 locations by 2032. Against that backdrop, the larger revolving facility gives CAVA more room to support this footprint buildout and related investments, but it also sits alongside covenants and leverage considerations that could matter if same restaurant sales or unit economics come under pressure.

Yet behind the appealing growth story, investors should also be aware of how higher fixed costs and added leverage could amplify the impact of any slowdown in...

Read the full narrative on CAVA Group (it's free!)

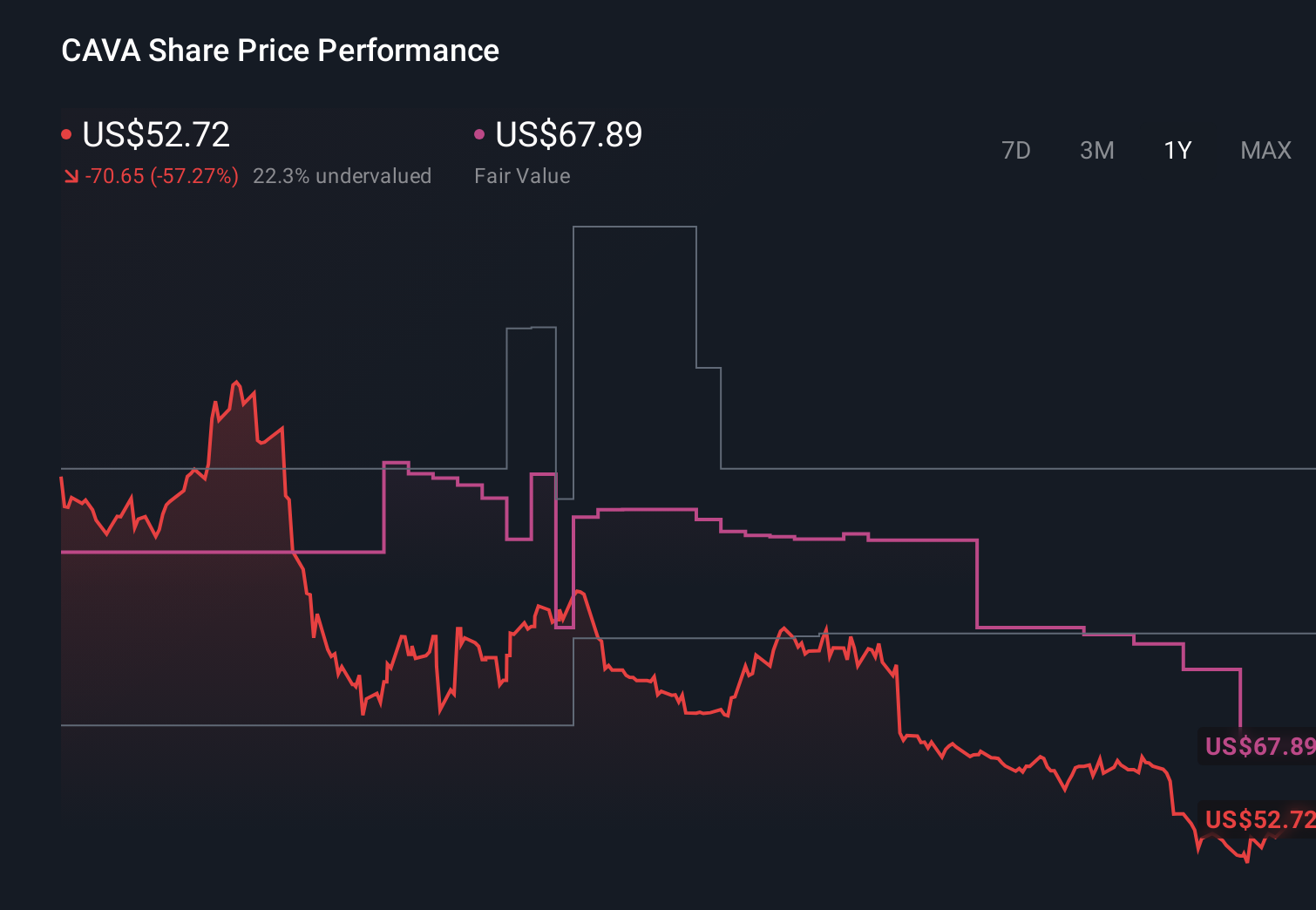

CAVA Group’s narrative projects $2.1 billion revenue and $119.1 million earnings by 2029. This requires 21.7% yearly revenue growth and a roughly $55 million earnings increase from $63.7 million today.

Uncover how CAVA Group's forecasts yield a $84.00 fair value, a 4% upside to its current price.

Exploring Other Perspectives

While consensus focuses on expansion and tech efficiency, the most bearish analysts were modeling revenue near US$1.8 billion and earnings around US$84.8 million, highlighting how views on margin pressure and expansion risk can differ sharply and may shift again as this larger, longer credit facility filters into updated scenarios.

Explore 9 other fair value estimates on CAVA Group - why the stock might be worth 45% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CAVA Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com