- If you are wondering whether Kinsale Capital Group's current share price still reflects good value, the recent moves in the stock give you plenty to think about.

- The shares last closed at US$336.69, with a 2.6% gain over the past week, set against declines of 13.6% over 30 days, 14.2% year to date and 30.7% over the past year.

- These price moves have kept Kinsale on the radar for investors who track longer term return profiles, with the stock showing 12.2% over 3 years and 99.1% over 5 years. This mix of shorter term weakness and longer term returns often prompts a closer look at whether the current price lines up with underlying value.

- Kinsale currently has a valuation score of 3 out of 6. The sections that follow will compare different valuation methods to that score and then finish with a broader way to think about what the market might be pricing in.

Find out why Kinsale Capital Group's -30.7% return over the last year is lagging behind its peers.

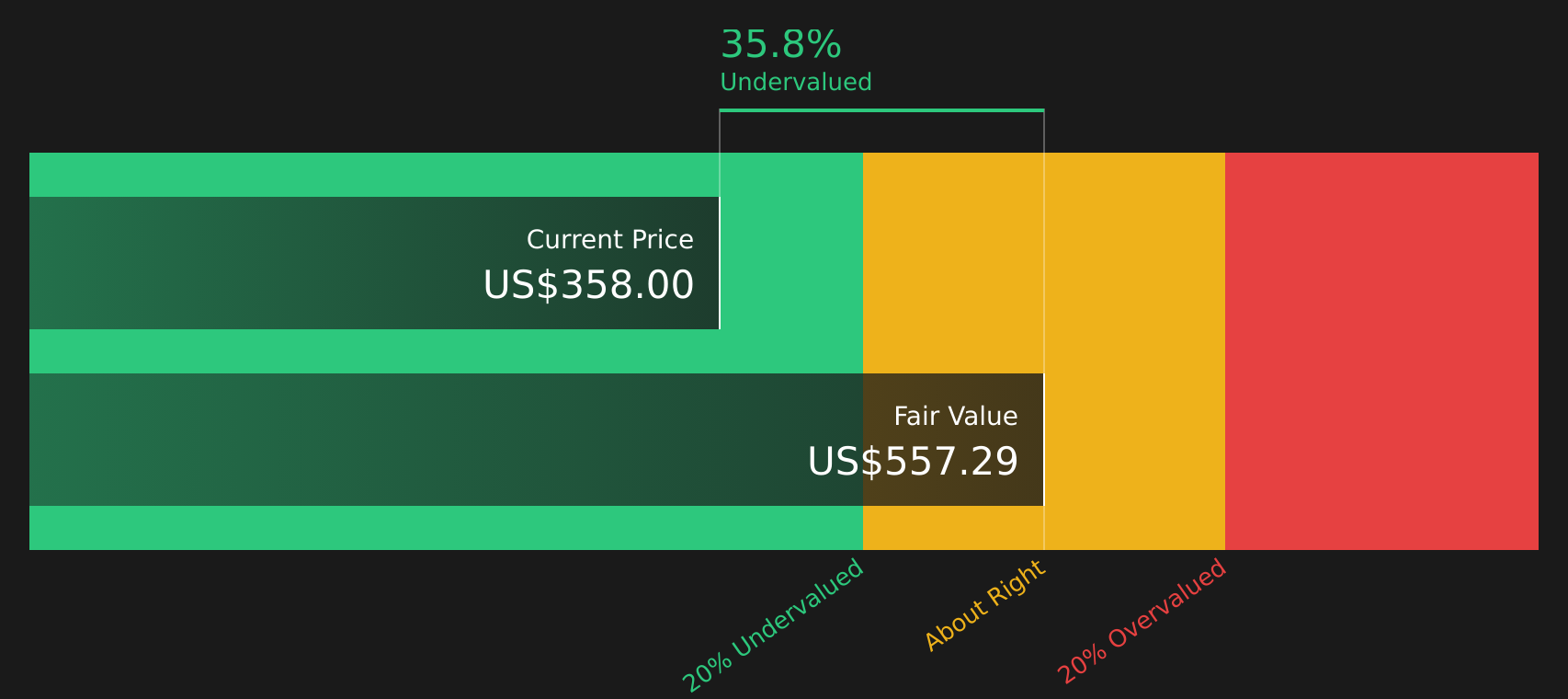

Approach 1: Kinsale Capital Group Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to generate above the return that shareholders require, and then adds the value of those excess profits to the current book value per share.

For Kinsale Capital Group, the starting Book Value is $84.66 per share, with a Stable Book Value estimate of $109.05 per share, based on weighted future book value estimates from 7 analysts. The model uses a Stable EPS of $23.49 per share, sourced from weighted future return on equity estimates from 8 analysts, and an Average Return on Equity of 21.54%.

The required return for shareholders, or Cost of Equity, is $7.61 per share. That leaves an Excess Return of $15.88 per share, which the model treats as value created above the required hurdle rate. Combining these inputs, the Excess Returns valuation points to an intrinsic value of about $554.20 per share.

Set against the recent share price of $336.69, this indicates the shares trade at about a 39.2% discount on this measure.

Result: UNDERVALUED

Our Excess Returns analysis suggests Kinsale Capital Group is undervalued by 39.2%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

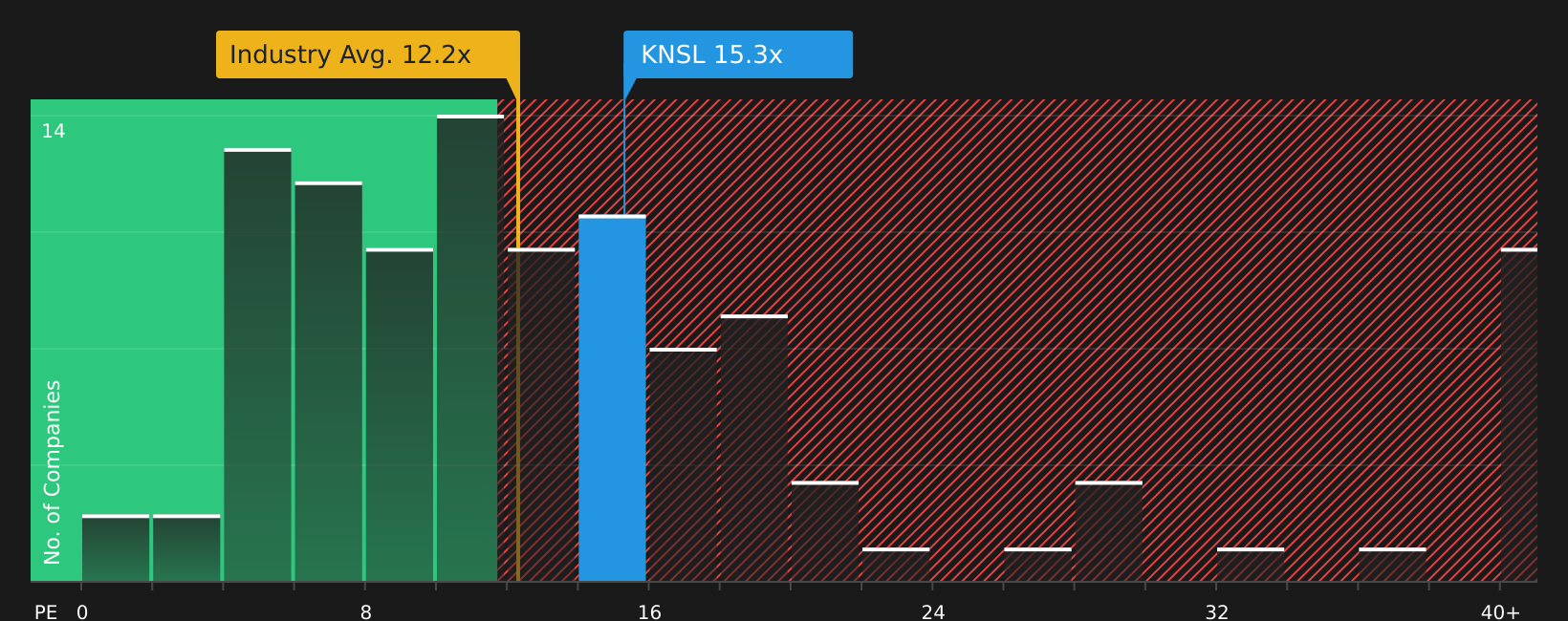

Approach 2: Kinsale Capital Group Price vs Earnings

For a profitable company, the P/E ratio is a straightforward way to relate what you pay for each share to the earnings that share currently generates. It helps you see how many dollars investors are paying for one dollar of earnings.

What counts as a "normal" or "fair" P/E often reflects expectations for future growth and the level of risk. Higher growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk usually point to a lower multiple.

Kinsale Capital Group currently trades on a P/E of 15.48x. This sits above the Insurance industry average P/E of 11.08x and also above the peer average of 7.97x. This suggests the market is willing to pay more for each dollar of Kinsale’s earnings compared with many industry peers.

Simply Wall St’s Fair Ratio for Kinsale is 11.75x. This is a proprietary estimate of what P/E might be reasonable given factors such as earnings growth, industry, profit margins, market cap and specific risks. Because it blends these company specific inputs, the Fair Ratio can give a more tailored view than simple peer or industry comparisons.

Comparing the current P/E of 15.48x with the Fair Ratio of 11.75x, the stock screens as trading above that fair level.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Kinsale Capital Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St’s Community page let you turn your view of Kinsale Capital Group into a clear story that ties assumptions about future revenue, earnings, margins and a fair value together, compares that fair value to the current price to help you judge whether the stock looks attractive or stretched, and then keeps that view updated as new information such as earnings or news arrives. For example, one investor might build a Narrative around the higher analyst target of US$450 with expectations for Kinsale’s growth, margins and a future P/E near 21.2x. Another might lean toward the lower US$312 target with more conservative assumptions. You can see these different stories, test which one feels closer to your own expectations, and decide what that means for your own timing and risk tolerance.

Do you think there's more to the story for Kinsale Capital Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com