- If you are wondering whether Intuitive Surgical's current share price still makes sense for your portfolio, it helps to break the story into what the stock has done recently and what the numbers say about value.

- The stock closed at US$452.78, with returns of 5.3% decline over 7 days, 10.1% decline over 30 days, 19.4% decline year to date and 8.6% decline over 1 year, set against longer term returns of 78.6% over 3 years and 77.3% over 5 years.

- Recent headlines around robotic surgery adoption, competitive activity in medical devices and evolving healthcare spending have kept investor attention on how much growth is already priced into Intuitive Surgical. These themes help frame whether the latest pullback is just noise or a shift in how the market is thinking about risk and return for the stock.

- Simply Wall St's valuation model currently gives Intuitive Surgical a score of 1/6. The rest of this article will unpack what that actually means across different valuation methods and then finish with a broader, more practical way to think about what "fair value" really is for this company.

Intuitive Surgical scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

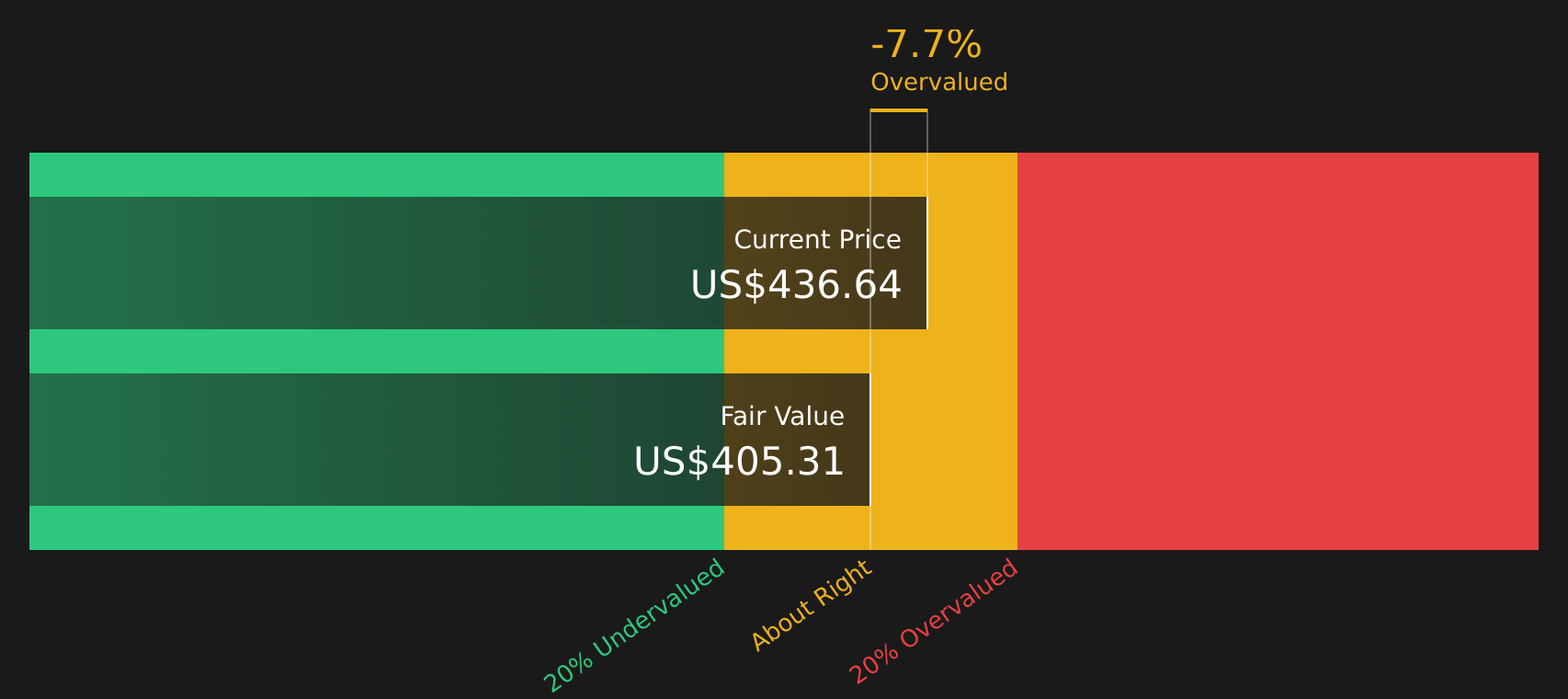

Approach 1: Intuitive Surgical Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow, or DCF, model estimates what a business might be worth by projecting its future cash flows and then discounting those back to today using a required rate of return. It is essentially asking what all those future dollars are worth in present day terms.

For Intuitive Surgical, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month Free Cash Flow is about $1.96b, and analysts and internal estimates project Free Cash Flow of $6.08b in 2030. For the years in between, Simply Wall St combines analyst estimates for up to 5 years with extrapolated figures beyond that to build a ten year cash flow path in dollars.

After discounting those projected cash flows back to today, the DCF model arrives at an estimated intrinsic value of about $378.73 per share. Compared with the recent share price of $452.78, this implies the stock is about 19.6% above that intrinsic value, so on this model Intuitive Surgical screens as overvalued rather than cheap.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Intuitive Surgical may be overvalued by 19.6%. Discover 62 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Intuitive Surgical Price vs Earnings

For profitable companies like Intuitive Surgical, the P/E ratio is a commonly used yardstick because it directly links what you pay per share to the earnings that each share generates. It is a quick way to see how much the market is willing to pay for current earnings.

What counts as a “normal” P/E depends a lot on how much growth investors expect and how much risk they see. Higher growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually means investors look for a lower multiple.

Intuitive Surgical currently trades on a P/E of about 56.3x, compared with a Medical Equipment industry average of about 27.2x and a peer average of roughly 30.5x. Simply Wall St’s Fair Ratio for Intuitive Surgical is 37.7x, which is a proprietary estimate of what the P/E might be given factors like earnings growth, industry, profit margins, market cap and risk profile.

This Fair Ratio can be more useful than a simple comparison with peers, because it tries to adjust for differences in growth, profitability, industry positioning and size. Set against the current P/E of 56.3x, the Fair Ratio of 37.7x suggests the shares are priced above that modelled range.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Intuitive Surgical Narrative

Earlier we mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story about Intuitive Surgical to specific assumptions for future revenue, earnings and margins. You can then convert that into a Fair Value to set against today’s price. Each Narrative lives on the Community page, updates automatically when fresh news or earnings arrive, and can reflect very different viewpoints. For example, one investor may see a Fair Value of about US$325 per share, another may see roughly US$750, and others may be clustered in between. This allows you to quickly see which story feels closest to your own and decide how the current price lines up with what you believe the stock is worth.

For Intuitive Surgical however we will make it really easy for you with previews of two leading Intuitive Surgical Narratives:

🐂 Intuitive Surgical Bull Case

Fair value in this narrative: US$532.46 per share

Implied valuation gap vs last close: about 15.0% below this fair value

Revenue growth assumption: 12%

- The author focuses on Intuitive Surgical as a long established leader in robotic assisted surgery, with the da Vinci platform at the center of its model.

- A large installed base and a high share of revenue from instruments, services and software are highlighted as key supports for recurring cash flow.

- The narrative treats the stock as roughly in line with fair value on the author’s assumptions. Return expectations are described as closely tied to long term cash flow growth rather than a substantial change in valuation.

🐻 Intuitive Surgical Bear Case

Fair value in this narrative: US$325.55 per share

Implied valuation gap vs last close: about 39.0% above this fair value

Revenue growth assumption: 12%

- This narrative still describes Intuitive Surgical as a clear leader in robotic surgery but questions whether the current price already reflects strong adoption across more procedures and regions.

- It highlights high capital costs for hospitals, regulatory and reimbursement changes and rising competition as key risks to both growth and margins.

- The author frames the stock as overvalued on their fair value estimate. Outcomes are described as sensitive to any shortfall against growth expectations or pressure on valuation multiples.

Once you have seen how different investors frame the same stock through these Narratives, the next step is to decide which set of assumptions feels closest to your own view and what that implies for position size, time horizon and risk tolerance in your portfolio.

Do you think there's more to the story for Intuitive Surgical? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com