Over the last 7 days, the United States market has experienced a 1.9% decline, yet it remains up by 15% over the past year with anticipated earnings growth of 15% annually in the coming years. In this dynamic environment, identifying promising small-cap stocks with insider buying can offer unique opportunities for investors seeking potential value amidst fluctuating market conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Enovis | NA | 0.6x | 49.71% | ★★★★★★ |

| PCB Bancorp | 8.5x | 2.8x | 29.02% | ★★★★★☆ |

| Financial Institutions | 8.3x | 2.6x | 46.07% | ★★★★★☆ |

| Franklin Financial Services | 10.6x | 2.6x | 2.82% | ★★★★☆☆ |

| 1st Source | 10.6x | 3.9x | 49.85% | ★★★★☆☆ |

| German American Bancorp | 13.7x | 4.5x | 47.47% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 41.69% | ★★★☆☆☆ |

| Union Bankshares | 9.7x | 2.0x | 24.02% | ★★★☆☆☆ |

| Aldeyra Therapeutics | NA | NA | 44.25% | ★★★☆☆☆ |

| Douglas Emmett | 103.9x | 1.5x | 44.83% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

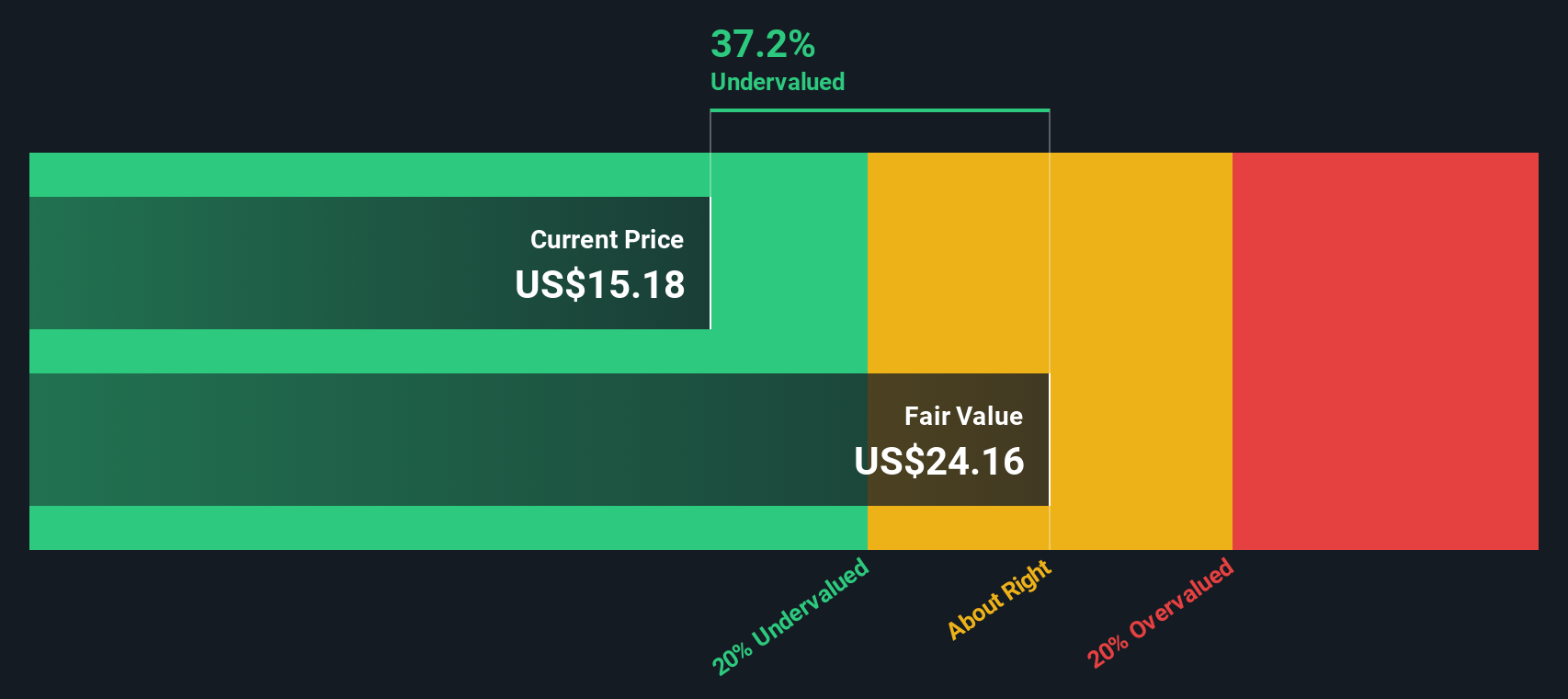

Monro (MNRO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Monro operates a chain of auto repair centers, with a market cap of approximately $1.5 billion.

Operations: The company generates revenue primarily through its auto repair centers, with a recent revenue figure of $1.18 billion. The cost of goods sold (COGS) was approximately $768.66 million, resulting in a gross profit margin of 34.77%. Operating expenses were reported at $387.64 million, impacting the net income which was noted as negative in the latest period at -$13.87 million, leading to a net income margin of -1.18%.

PE: -33.5x

Monro, a company with a focus on auto services, has shown insider confidence through Mario Gabelli's significant share purchase worth US$9.1 million. Despite facing higher risk due to external borrowing, Monro's earnings are projected to grow by 64% annually. Recent financials reveal mixed results: third-quarter sales dipped slightly to US$293 million, yet net income more than doubled from the previous year. Their consistent dividend policy underscores stability amidst these dynamics.

- Click to explore a detailed breakdown of our findings in Monro's valuation report.

Gain insights into Monro's past trends and performance with our Past report.

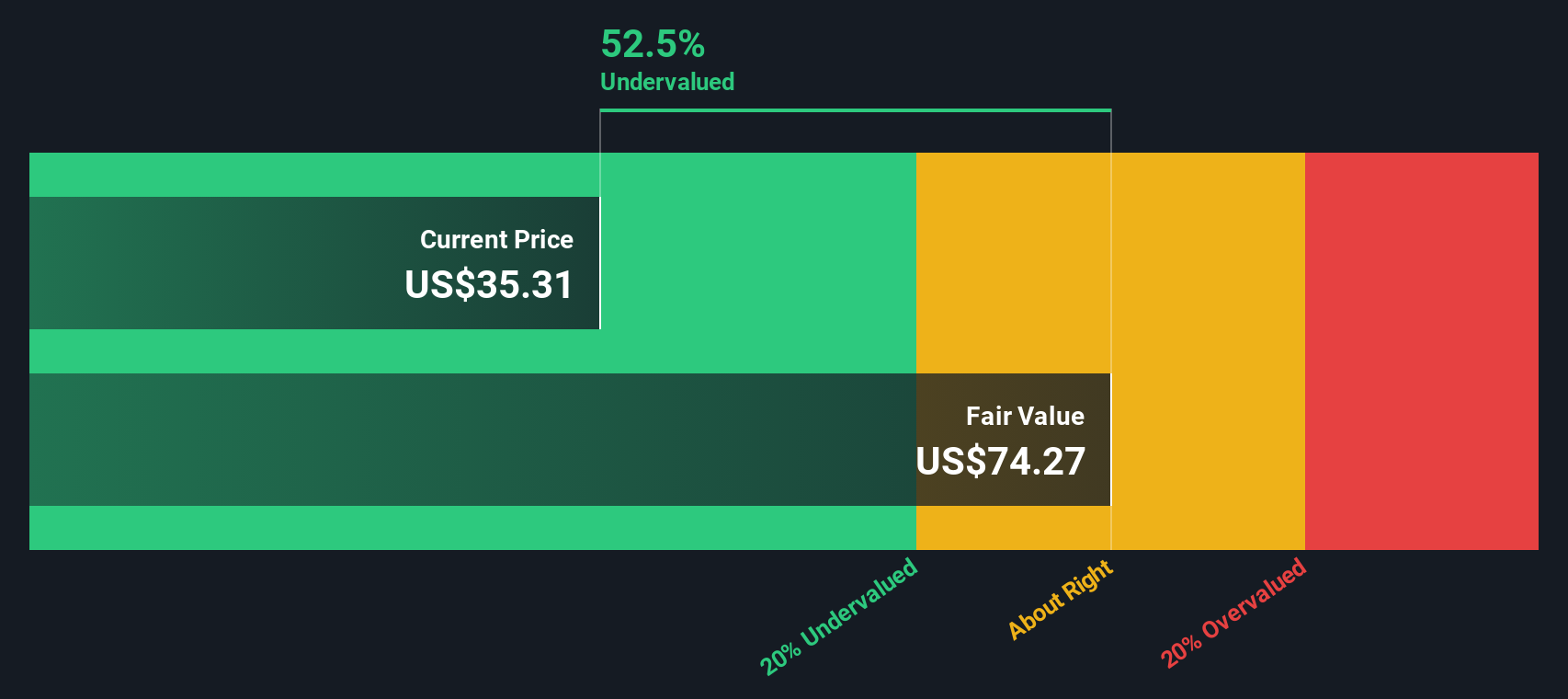

LTC Properties (LTC)

Simply Wall St Value Rating: ★★★★★☆

Overview: LTC Properties is a real estate investment trust focusing on senior housing and healthcare properties, with a market cap of approximately $1.49 billion.

Operations: LTC Properties generates revenue primarily from its Real Estate Investment Portfolio and Seniors Housing Operating Portfolio, with recent figures showing $190.27 million and $72.12 million respectively. The company's gross profit margin has shown fluctuations over time, peaking at 99.98% in Q1 2017 before declining to 72.28% by the end of 2025, indicating variations in cost management relative to revenue growth.

PE: 15.4x

LTC Properties, a healthcare-focused real estate investment trust, recently showcased at Deutsche Bank's Healthcare REIT Summit. Their Q4 2025 earnings revealed a significant rise in net income to US$102.2 million from US$18.08 million the previous year, with basic EPS climbing to US$2.13 from US$0.40. Despite projected earnings decline of 4.3% annually over the next three years, insider confidence is evident through recent share purchases by company leaders, signaling potential value recognition amidst challenging funding conditions reliant on external borrowing sources.

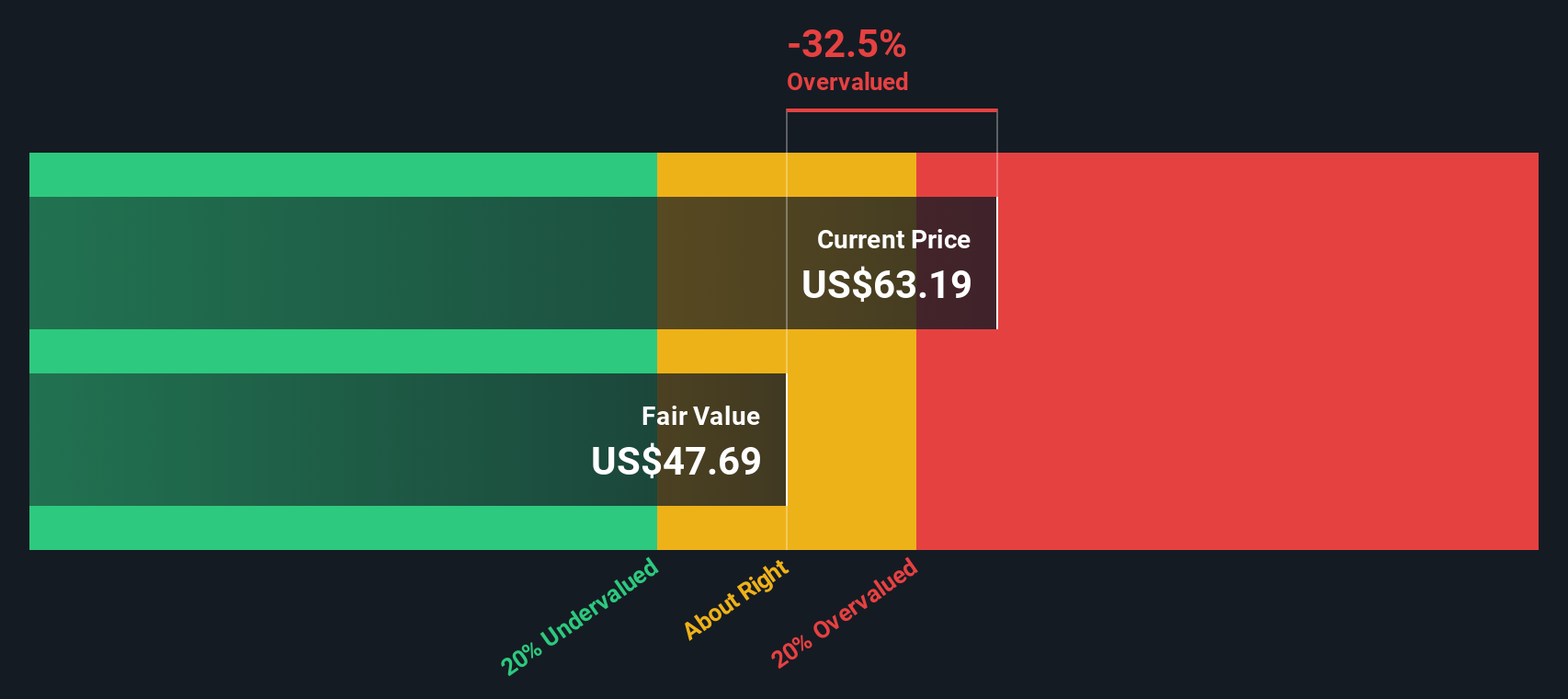

Tecnoglass (TGLS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Tecnoglass is a company that specializes in the manufacturing and distribution of architectural glass and windows, with a market capitalization of approximately $1.62 billion.

Operations: The company's revenue is primarily driven by its Architectural Glass and Windows segment, with a recent quarterly revenue of $983.61 million. The gross profit margin has shown variability, reaching 50.59% in early 2023 before adjusting to 42.84% by the end of the year. Operating expenses include significant allocations for sales and marketing as well as general and administrative costs, impacting overall profitability.

PE: 11.9x

Tecnoglass, a player in the construction materials sector, is capturing attention with its growth potential and strategic financial maneuvers. The company forecasts annual revenue growth of 11% for 2026, targeting between US$1.06 billion and US$1.13 billion. Recent earnings showed a slight dip in net income to US$159.57 million for 2025 but maintained stable earnings per share at US$3.42. Insider confidence is evident as they increased their equity buyback plan by US$100 million in February 2026, completing significant repurchases totaling over 7% of shares since November 2022 for approximately $156.59 million . Despite relying on external borrowing, Tecnoglass continues to pay dividends quarterly at $0.15 per share, reflecting its commitment to shareholder returns while navigating higher-risk funding sources.

- Click here and access our complete valuation analysis report to understand the dynamics of Tecnoglass.

Gain insights into Tecnoglass' historical performance by reviewing our past performance report.

Summing It All Up

- Click through to start exploring the rest of the 58 Undervalued US Small Caps With Insider Buying now.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com